You don’t see a problem with you net worth dropping by 500k in a single day, even though nothing bad happened? I think in accounting you always try to smooth things out. For example you depreciate an asset. If you own a car for 10 years and sell it for 10% of the value, you don’t record a 90% loss on the day of the sale, instead each year you record a slight depreciation of the car.

The same should apply to pension. I’m sure there are some real-life cases where people with the right experience can tell how its done, and I simply don’t accept your way of doing this. How would it work anyway, I record a -500’000 booking on my 2nd pillar account and where do I book the +500’000? On “expenses”? Makes no sense.

It is not complicated, just include an account, like a savings account with your lifespan in months x monthly pension. when you receive monthly income it would be transfer from that account to your cash holdings. Like depreciating the asset. And if you live longer- than it would be weird yes, you will have asset reclassification (like re assessing your car or house value). But I assume you would not mind positive surprises after 85 (if you are still tracking)

This is not a problem at all.

Either you take the lump sum (in which case you know the value of your second pillar).

Or you choose the annuity, and this annuity’s value is computed in exactly the same way as other assets: by taking the present value of future cash flows.

If you retire and go for the annuity, its value is computed by V = P/r (this is a special case because as long as you are alive the annuity never ends), where P is the annual payment and r the discounting rate. For the discounting rate i would personnally take my opportunity cost. Another way would be to use the SWR + possibly inflation.

So if you say that you have a 2nd pillar of 500k and you choose the annuity generating 6% of these 500k (i.e 30’000 k per year), then:

if you use a 4% SWR, then V = 30’000/5% = 750’000CHF

if you use your opportunity cost (you could invest the money on the stock market at 7%), then V = 30’000/7% = 428’571 CHF

Cool stuff, that’s what I was looking for! But of course I will not live forever, so it would make sense to calculate my life expectancy and get the value for that number of annuities (?)

If you are doing the calculus, it seriously does not change anything because as soon as you are dead you won’t have the money anyway.

Same thing for your partner, if you die then she will receive the annuity instead of you until her death.

However, it is different for your children. A lump sum is transmissible, an annuity is not.

Anyway, regarding lump-sum vs annuity, the point i want to make is the following:

At retirement age you will have to choose between lump sum and annuity

to do the comparison you need to discount the cash flows of the annuity to present value

the value of the annuity depends a lot of your opportunity cost. The higher the opportunity cost, the lower the value of the annuity and vice versa

Let’s say you were to retire tomorrow. With current conditions, you would choose the annuity of 6% if you think you would not be able to do any better with the 500k. You would choose the lump sum if you think you can invest it at a better rate (as we have seen, a 7% opportunity cost decrease the value of a 500k 6% annuity to 428k).

with the current trend in bond rates, it is possible that the annuity rate will become lower and lower, in which case the lump sum becomes more and more interesting.

Only when leaving the CH/EEA/EFTA for good. Mandatory pension benefits will be retained in Switzerland as long as you live in Europe.

While that might satisfy your personal tolerance to risk, the same is true for any investment where the funds are locked.

By the same logic, you could exclude real estate as well. It could devalue literally overnight, so you don’t know how much bread you’re going to get for it.

As the others said, it doesn‘t drop. It’s the present value of future cashflows.

And wouldn’t the annuity payment „smooth things out“ over the longer term, rather than taking one lump sum payment?

…as opposed to the current trend in medical technology and progress, which might lengthen your expected life span

Also, one shouldn’t forget the effect of different taxation and/or tax rates for lump-sum vs. annuity payments.

Well, that’s what I thought, but the guys above didn’t say anything about leaving CH. Of course I wouldn’t like to have to leave CH in order to pay out 2nd pillar. So how is it?

You didn’t say anything about present value, you didn’t say how to actually book it.

Don’t you get it? The day you go for the annuity, the balance on your 2nd pillar account goes to 0. The annuities will be however paid out in the future, like salary, and you normally don’t book future salaries. So yes, in time the annuities will bridge that gap, but unless you introduce a new asset, where you calculate the present value of future annuities, your net worth chart will have a huge drop at one point.

Your salary is a trade of your time for money. Your haven’t yet traded your future time yet so you shouldn’t prematurely book the money for it.

Cash flow from annuity is a sure thing on the other hand (ignoring bankruptcy risks), it’s a contract, like a bond. That’s why it’s an asset you should book now. When you’re buying bonds/stocks do you also mourn the fact that your brokerage account’s cash balance goes to zero as a loss? Pension annuity is like a bond you can buy at your broker, except there’s more strings attached and it’s not as readily sellable on the market - but for the right price your pension fund generally would be willing to trade it for cash.

You have EU passport? Then coming back should be as easy as getting a new job offer. It’s only problematic for non-EU.

Seem like I’ve triggered an interesting discussion here.

I do include blocked employer shares, as they will become vested over the next couple of years. I do not include 3a as those assets are blocked for many years still. I also do not include the pension fund. I know my numbers, though, they’re just not on my "net worth sheet”.

I tend to agree with @Bojack regarding accounting and tracking of pension funds.

Before the age of 60, when you leave your employer, the money can be parked in a (personal) Freizuegigkeitsaccount. It is blocked there until 60, except for the 3 cases: freshly becoming self-employed, leaving the European social security area or for buying a house you personally live in .The property can also be in the European social security area (due to non discrimination clause in the treaties).

The money may be left in your Freizuegigkeitsaccount up to age 70 (even if you are not working).

》》It would take massive changes to effectively abolish the possibility of taking your money out of PK.

Not even that - He/she just needs to have the financial means to sustain himself.

As long as someone does, he’s free to immigrate and settle in Switzerland (as an EU citizen).

Though a quick and pre-planned return is kind of “cheating the system”, as you have to leave Switzerland indefinitely, in order to cash out your pension benefits (not saying that it doesn’t happen).

…which you should better rename to “liquid net worth” or something similar then!

I think pension benefits and pillar 3a should definitely be included in “net worth” - though there’s nothing wrong with preferring a more liquidity-based definition of one’s net worth for accounting and comparison purposes.

…or, for completeness’ sake…

a) if become eligible to a full disability pension

b) once you die

c) upon divorce, for (usually part-) transfer to your ex-spouse due to a divorce decree

That’s a long read for what you yourself accurately summarize to: Future cash flows have a present net value. And while I use quite different assumptions, this is more or less what I do too.

There are at least three possibilities to get money out of the 2nd pillar (ignoring the fourth case: Getting divorced):

Buying self-inhabited real estate

Becoming self-employed (as an individual company, not as a corporation)

Emigrate out of Switzerland. Leaving CH towards EU/EFTA will allow you to free up the extra-mandatory portion or your assets, leaving EU/EFTA will allow you to get all he money. In those cases, tax implications might be severe (first two cases come with specially low CH taxes, which is comparatively bearable).

Wait what? So you pay pillar 3a every year, basically assuming that your money is lost immediately after payment? How does that make sense?

Good point. My main argument is anyway the point that even if your are subject to local social security, you still get your extra-mandatory share. For high earners, and many here seem to be part of that bunch, this is the large majority of the funds.

Indeed if you have no say in the asset allocation of your 2nd pillar (and consequently also little to no risk with it), there is little to take into consideration regarding asset allocation in total.

However with 1e solutions for the 2nd pillar this changes dramatically. I can freely choose the super-mandatory portion, and for example am 75% in stocks with that part (at my own risk of course).

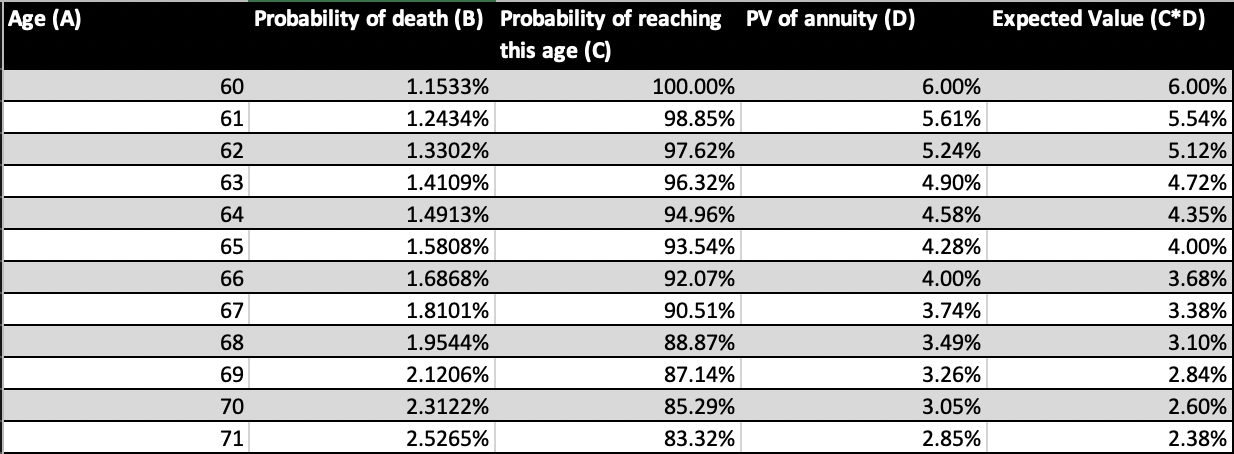

Alright. So if anyone is interested, I found the probability of dying each year. Then I used your formula to calculate present value (this website has a nice explanation). I plugged it into an excel sheet. (probabilities are for males)

So if you sum up all the expected values for each year (last column), you will get a total as a proportion of the lump sum.

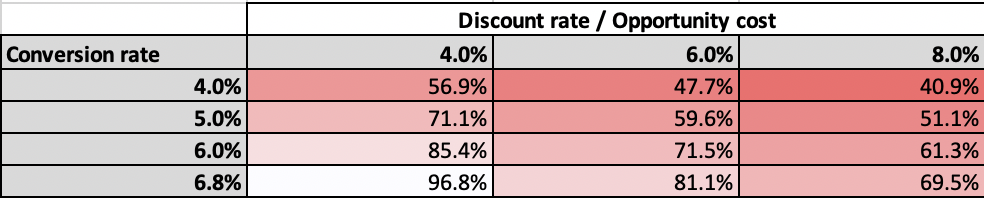

I made a comparison for a different combination of conversion rates (Umwandlungssatz, i.e. what the pension fund will pay you annually) and discount rates (your own return on capital if you invested privately).

Going for the annuity seems like a bad idea in each scenario. But do you actually know if the annuity amount is frozen forever from the moment you’re 60, or is it adjusted for inflation?

According to the calculation, the Present Value of the annuity (column D) would be roughly half after only 10 years: that seems very wrong - as, to be honest, do your assumed discount rates between 4 and 8 per cent.

The point of the pension payments is that the income is pretty much guaranteed (at least nominally). At interest rates of 4.0%, let alone 8%, however, your investment is everything but guaranteed.

Discounting a (reasonably) guaranteed cashflow like the annuity pension payouts with a discount rate that mirrors volatile (e.g. stock market) if not downright high-risk (at 8%) investments seems like comparing apples to oranges.

Whatever you choose as a discount rate, the central bank rate (as a risk-free rate, currently below 1%), the BVG minimum rate (1%, though somewhat arbitrarily) or the inflation rate (again, below 1%) would seem more appropriate to me. Though I’d probably try to choose something like a longer-term average inflation rate.

This discussion of how to “bookkeep” pensionskasse at 60 & beyond money surprises me.

As Mustachians & FIRE-people we will all be getting our stash “out” early on early-retirement, transferring it to a Freizügigkeitskonto* (only option if staying in CH/EU), then at 60 finally taking control of the lump sum and investing that & living of the dividends and some of the stash itself. Won’t “we”?

*before you retire & later when in the Freizügigkeitskonto (<60) the stash is either bond-like (if cash account) or potentially at Viac or VZ could be part of your equity portfolio.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.