Unfortunately doesn‘t seem that USD is getting stronger.

Probably not for quite a few months

What‘s going on today?

continued expectations of early fed cuts and low volume.

If I understand correctly from thid forum, hedging USD to mitigate the risk of USD decline is not really worth it. How do the more experienced users here handle this?

I think only going with Swiss stocks would be too risky. From my perspective, one just has to live with the USD decline.

1 Like

I start to ask myself this question. I see VT (USD) increasing its value but the CHF worth at a lower speed obviously. This makes me think if investing only in USD is the right thing to do. I know that VT is based on 65% USD, but nevertheless its value is USD.

Assume that today you have 1M USD in VT (or any other USD-based ETF). US inflations is not getting better and it’s likely that it will continue. I started to read the book “Principles for Dealing with the Changing World Order: Why Nations Succeed or Fail” and the following picture made me think a bit about the long-term strategy. Is all the theory based on when US was one of (or the) most powerful nation in terms of economics?

1 Like

It seems to me that your are mixing two effects:

-

The intrisic value of companies, which is affected by their ability to generate profits. This value can be expressed in a number of currency metrics, USD being one, CHF being another. Reading the value in USD or in CHF doesn’t change this intrisic value, therefor, VT gaining value when measured in USD and loosing value when measured in CHF is irrelevant to the Swiss investor. Only the CHF value matters, since that is how that money can be expected to be spent (by you or your heirs).

-

The prospects of varrying currencies when measured against each other. The USD is an inflationary currency while the CHF has been mostly flat as of late. A weaker currency helps exports but makes importing goods more expensive. On the other hand, inflation tends to be lower and salaries higher in countries with a strong currency.

That doesn’t mean the stock price of companies of a country may not have better or lesser prospects from each other (I consider the US to be overvalued because with their recent outperformance, people have dived into the S&P500 and the NASDAQ more than would probably be warranted by a proper valuation of the companies) but I would consider companies prospects independently from the behavior of the currency in which they are measured.

From December 2008 (near inception) to November 2023, 10 kCHF invested in VT would have turned into 36 kCHF in nominal terms and 34 kCHF in inflation adjusted (real) terms, for a real CAGR of 7.76%.

The lower apparent growth of the value of the fund measured in CHF has been compensated by lower inflation (5% total over the period in Switzerland vs 40% in the USA). The actual real CAGR are pretty close when measured both in USD and in CHF (7.19% in USD vs 7.76% in CHF).

This may not hold true in a world with bigger barriers to trade that may decouple domestic inflation from the international exchange rate of the domestic currency, so worries about the prospects of the US may, or may not, be warranted.

14 Likes

My whole year gains are basically gone due to this insane CHF apreciation compared to USD. Feels terrible.

Im thinking really hard about hedging right now. At least a bigger part of the portfolio.

1 Like

You’re aware it doesn’t change the end result, right? Hedging costs the delta of the risk free rate between CHF and USD (3.75% currently), and over long period of time it’s going to be the same as not hedging.

(it sounds like you’re trying to time the FX market, which if you’re confident about your play you can make a lot more money than whatever you might gain with a successful hedge)

1 Like

Yes, thousands of CHF gone by the day…

I now go for 25% of Swiss stocks ETF and 75% of All World stocks in USD.

1 Like

There is some evidence partially hedging might be worth it. Im trying to find the paper again. You smooth the currency fluctuations and can take advantage due to rebalancing.

Since some time the benefit seems to be worth it as well. CHF USD made almost 20% ! in the last 4 years and the recent run-up was insane.

There has also been a recent paper by Scott Cederburg, that proposed a high home bias (35%) to be superior longterm and in this Rational Remidner Podcast episode https://www.youtube.com/watch?v=y3UK1kc0ako he also said hedging may be worth it, but didnt study it. Big part of a home bias being superior in his findings seems to be currency.

Im aware that it’s a bit sepcial in CH, due to SMI being all multinationals etc. That’s why Im thinking about a higher proportion of swiss stocks + a hedged portion. Something like 10-20% SPMCHA + 10-20% ACWIS maybe. Rest unhedged.

But equity day to day fluctuation typically trumps FX changes by a lot (that’s in the vanguard paper re hedging).

Edit: in any case just make you don’t have recency bias, it’s the worst enemy of the long term investor, you FOMO and decide to change your allocation, but that’s after the overperformance and you instead get the reversion to the mean ![]()

4 Likes

6 Likes

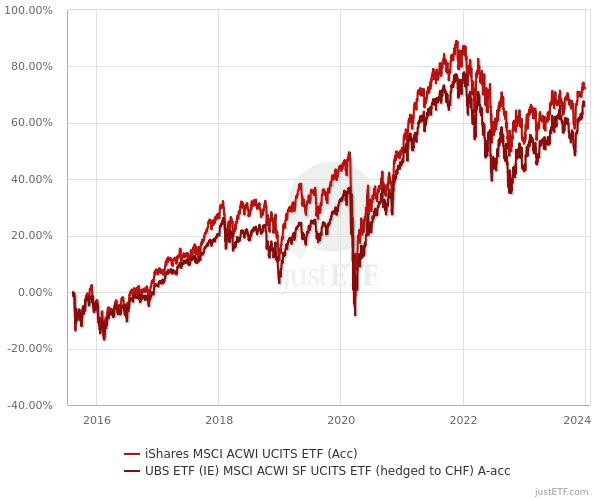

Please help me read this chart: is the unhedged one in CHF as well, so did it perform about 5% better after four years when calculating in CHF?

According to justeft, the return chart for both is in CHF (I’d expect much bigger differences if wrong currencies were compared anyway).

I wouldn’t consider a 5% difference over 4 years as significant for an investment in stocks: I’m expecting a high level of variability in outcomes in which such a 5% difference would easily fit. So I would base my decisions regarding my investments in them on fundamentals rather than short term past performance.

What I take out of these charts is that the hedged and unhedged funds both had a behavior primarily affected by stocks and that both behaved mainly similarily. I’d use bonds denominated or hedged in CHF if I wanted to reduce my exposure to currency fluctuations (short term if I wanted to also avoid interest rate risk) and I’d keep a long term investing horizon for my stocks, not caring much about what happens in-between, including the recent short term drop of the USD vs the CHF (the longer term effects being handled by the interest rate parity theory).

Edit: to be clear, when I write “short term drop”, I don’t imply that I expect it to revert and be canceled out in the short term, rather that it happened rapidly and recently, without making a prognostic whatsoever on what the currencies pair will do in the short term future.

4 Likes

USD/CHF stayed mostly flat during the 10 years bull market after the financial crisis and hedging it over this perioid had a performance drag of around 30%.

You have to look at the big picture. The FX market is brutally efficient and it will average out over many years and decades of ones investing career. Hedging USD/CHF makes only sense if you strongly believe that the devaluation will be higher than the market expects.

7 Likes

This is the part where Scott Cederburg is suggesting partial hedging might be a good idea and pushes down the optimal (per their study) domestic portion, for their findings of an optimal 100% stock portfolio.

1 Like

Btw still not sure how that reconciles with the paper clearly saying it’s not worth it:

Maybe that’s because the public of those videos is US investors who tend to not have any international exposure, in which case hedged international is better than no exposure?