I’m sorry to be very blunt but @portugalfire 's exception concerned dealing with a brokerage firm from your country of citizenship, so to use IBKR from a swiss place of residency while using that specific exception, one would need to be a citizen of the UK. I guess there are ways to become a UK citizen for those who aren’t already but I’m not sure the benefits are worth the trouble.

Depending on other citizenships, people may find ways to register to IBKR through their local entity if there is one, or have another choice of brokers available.

I would personally consider having to use UBS as a broker as part of the terms of my contract and put that in balance of my total compensation. Having restrictions linked to work contracts happens all the time: some need to live at less than 30 min than their working place, some have to have and use their own car, some have to do night and weekend shifts, etc. The way most people deal with it is to get compensated for it (and chances are the compensations offered by UBS aim to be competitive, so should take account of investing restrictions as a whole), rather than trying not to be subjected to those restrictions that are considered necessary for them to perform their job adequately.

I’m sorry to add that I find asking on an internet board rather than colleagues, our manager and/or compliance very naive and that doesn’t really reassure me as to the state of our banking industry…

I would like to add that using UBS services (which might be included into the compensation already and having advantage on prices of those services) is actually just a mini-optimisation on the scale a FIRE-seeking person is operating.

The most important part is actually to save 40%+ from our income and invest them into low-cost solutions, and the broker is not the most relevant part.

And otherwise, noone is forcing you to remain working at a certain employer, so stop being complainypants about it (to cite the namegiver of the movement).

I am not complaining, just seeking advice on possible optimization of the situation I am in. The comment on changing the employer was answered in my original post. Thanks!

Per advice from compliance, the exception can be given if someone already has an existing portfolio with the broker at their country of citizenship, at the time when they transferred to the company. It’s not for newly created brokerage accounts.

For your rather specific questions, I would say they have already been answered pretty well. Do not overthink or overoptimise too much, especially if you want to go with standard ETFs which have high liquidity. They are all more or less equivalent, since otherwise the instutional investors (which make the bulk of the AUM) would just run away from the inefficient ones.

@aire

Had the chance to talk with a UBS colleague about this. He did the following:

Open up a separate portfolio in his banking relationship with:

Custody account (0.175% p.a)

CHF account (included)

EUR account (included)

USD account (60.- p.a.)

Set up the FX option with margin. You need at least 20k coletaral for that (cash is counted 100%, ETFs 70%). As coletaral only the 3 accounts and the custody account in the new portfolio, all other accounts won’t be affected. That way you are able to exchange CHF to USD/EUR with a 0.17% margin. If you just do an account transfer from your CHF account to your USD/EUR account or just buy USD/EUR funds directly with your CHF account the margin will be 0.85%.

You shouldn‘t buy ETFs for less than 4300 CHF. From that amount it will cost you 0.863% no matter how much you buy. Anything less will be more expensive. For example buying 10 VTI for 1.8k CHF will cost 33 CHF (1.83%).

If your savings rate is 2-3k/month, I would buy the ETFs every 2 months. Do the FX change and enter the trade. Keep in mind to always chose the correct account to not get charged in the wrong currency.

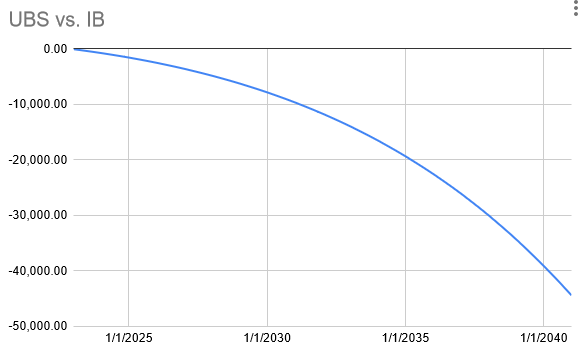

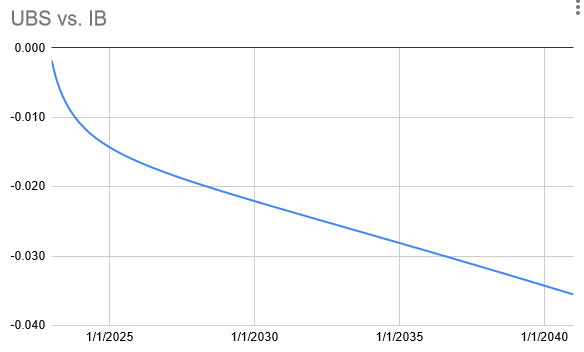

I calculated an example for comparing it to IBKR. Assuming 30k initial and 3k/month with an expexted return of 6.5%/year (6.325% for UBS because of custody fees) and accounting for the additional buying costs of ~1% (including FX) with UBS, after 15 years you would end up with:

just for curiosity, what are those conditions you have to invest in with UBS?

Like, what is the account fee, and how big are trading fees?

As a reference for IB: account fees: CHF 0 (above ~100k assets), trading fees: CHF 0.40 for a typical ETF purchase, and CHF 2-3 for a typical FX conversion

It’s not much of a difference if (once) you’re a millionaire.

When I was young, even 1000 Francs felt a lot of money. I’d actually used to live on less than that for a whole month. Today, my portfolio easily gains or loses that from day to day. You just adjust your own perspective.

So if you are a millionaire, throwing 25-30k in the bin isn‘t a big thing? No sane person would do that. But that‘s exactly what chosing UBS over IBKR makes you do.

That’s what I wanted to add to my previous post until you beat me to it.

You’re comparing it to an act of spending or expending, rather than viewing it as a fraction of your overall wealth or portfolio.

Now, if you spend 29‘000, that would certainly be no small expenditure in my book either. Nor even one thousand, frankly. If you do spend such amounts regularly, let alone recurringly, you‘ll blow through that million quite quickly.

But if you’re a millionaire, does just having another 29‘000 - on top of that one million - meaningfully increase your potential or options for consumption? I don’t think it does.

Also that’s over 15y, and there’s likely a tradeoff (e.g. having to invest with UBS, probably means you have a high comp job, maybe not doing so would reduce your salary by more than 2k per year)

Even ignoring any investment returns, 29’000 is only 161 CHF/month. And once you factor in compounding returns, that figure will move closer to a 100.

I hope - but also somewhat confidently assume - that working for UBS instead of AverageRandomBank™ will (over)compensate you for such opportunity costs by paying a bit more in salary every month.

Could you kindly explain the process you used to arrive at this optimal investing strategy, as well as the specific fee values you considered?

The figures I arrived at differ slightly:

A minimum fee of 40 CHF equates to a minimum transaction value of 40/0.006 → 6666.67.

For other exchanges with a minimum fee of 60 CHF, the minimum transaction value would be 60/0.0095 → 6315.79.

Given your track record and analysis shared in your post history, I am inclined to place more trust in your numbers than my own calculations. If you wouldn’t mind, could you kindly point out where I might have made a mistake?

As a UBS employee you get 50% off from the official prices. Stempelabgabe etc. still applies though, that’s why the minimum fee for abroad exchanges (for buying US ETFs for example) is around CHF 33.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.