Well, but this decision can have huge consequences for the ability to retire early.

you keep it all in cash and watch it slowly lose value due to inflation

you do invest in real estate but then are bounded to a location and still have to work a long time to pay off the mortgage

you invest in the stock market, and it either grows 4x in the next 10 years and you can retire, or maybe it stagnates and goes nowhere and you end up regretting that you didn’t buy a flat

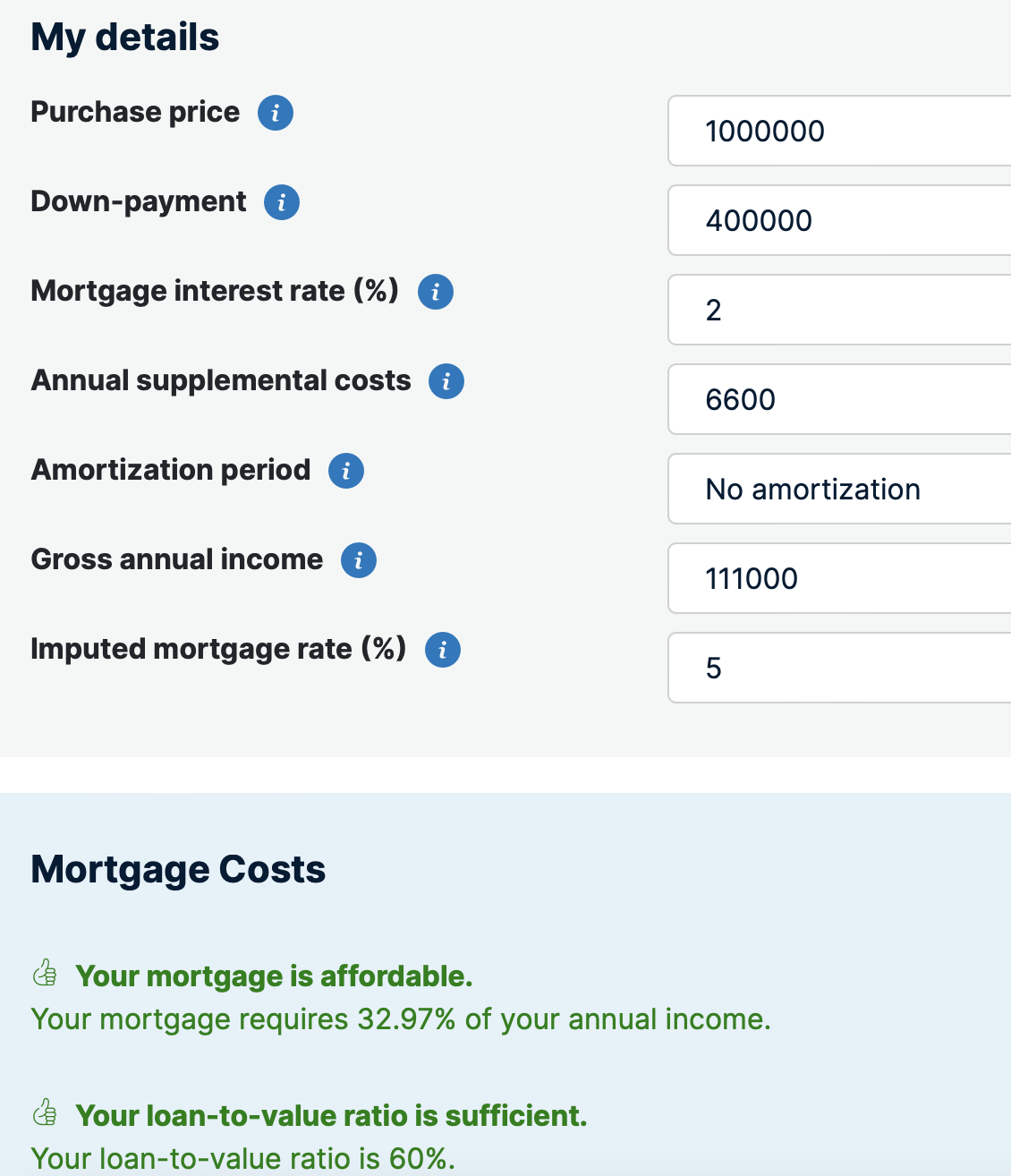

Well, find me a decent flat in Zurich for that money, that you will want to keep for decades. Or even for 1m, including 400k mortgage.

@Bojack. Money can be a source of issues between partners. I recall reading on the “Millionaire next door” that financial independence is correlated with the couple’s similar attitude to spending.

I would extend to investment up to a point.

What happens if she invests the whole amount and market stays down -20% for another 5+ years, this will strain the relationship.

I am educating my wife about investment, she is not much interested but partially receptive. What I do is to use a much lower risk profile for her investments and keep a larger part in cash.

Going back to your points:

I see 600k into a property and 400k or more into mortgage as a very safe way. You don’t sell real estate very often and she may get rents. Therefore she may not even feel price fluctuation

if she has little attitude towards risk, so be it.

alternatively you can have her investing 100k into stocks, 500k as cash deposit and 500k as mortgage. Still low LTV and she can vibe the stock market at lower exposure level

Is that hers or yours goal ? From previous posts of yours, I recall that RE was your goal. Her goal might be “only” a decent, comfy life.

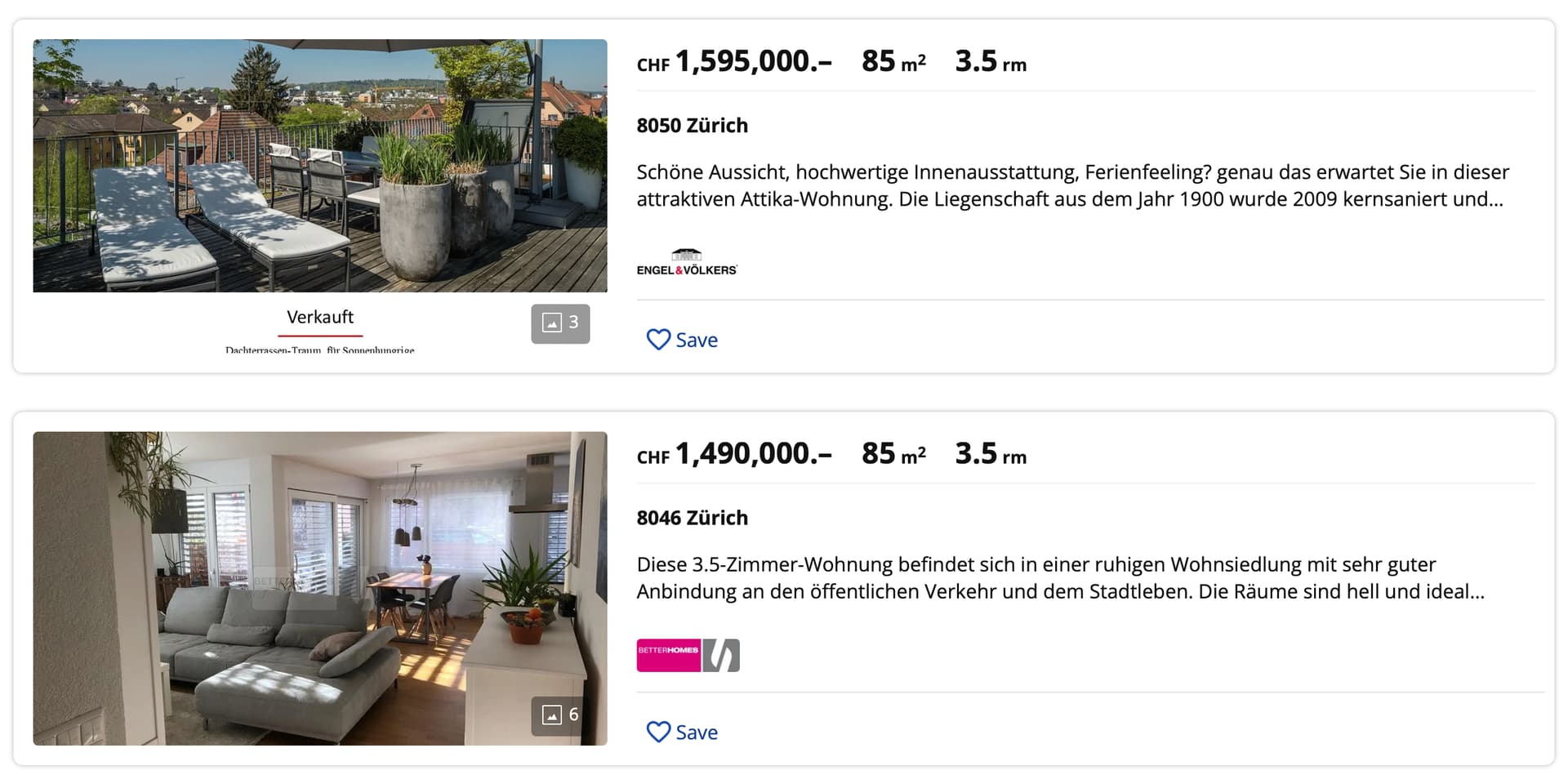

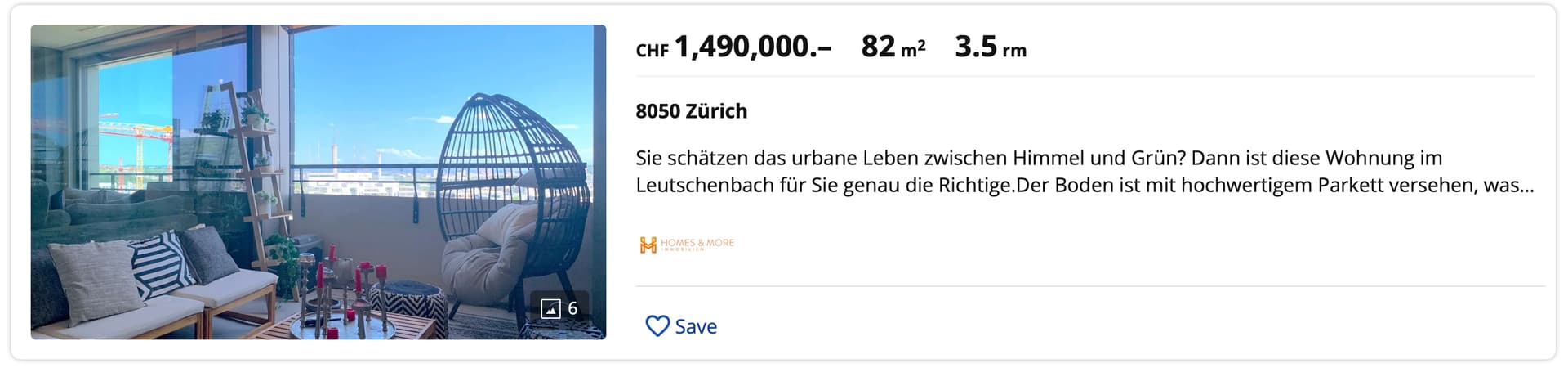

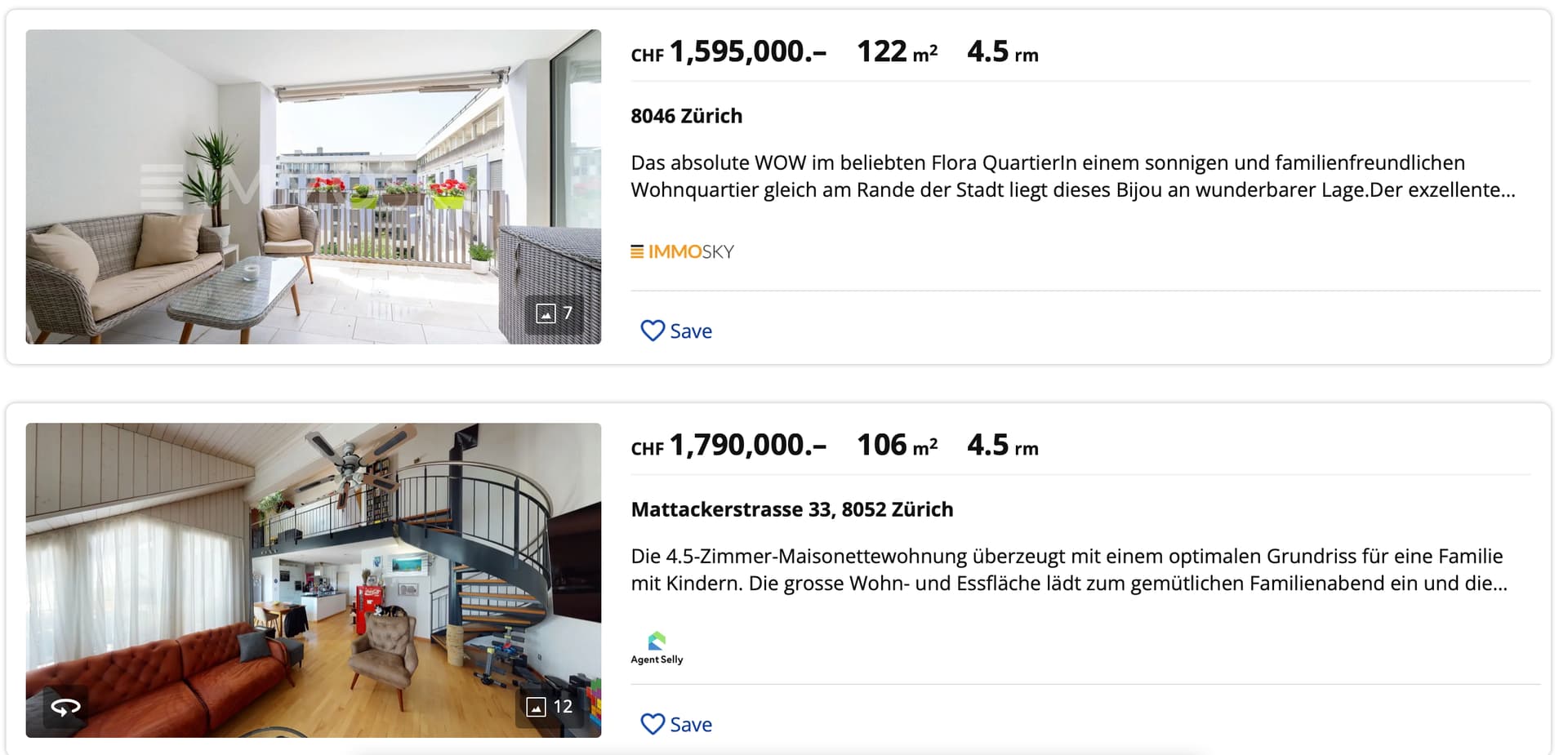

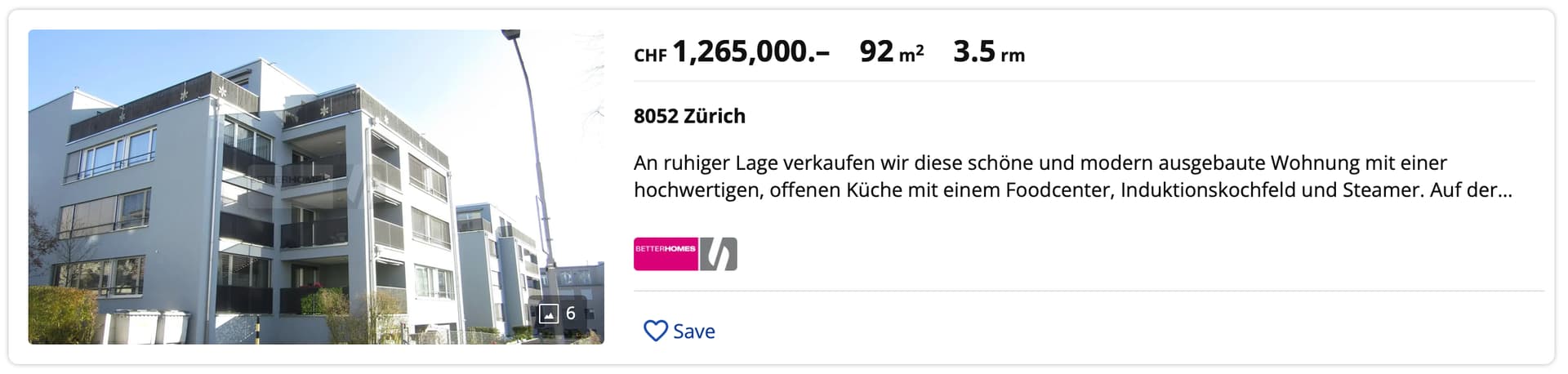

As I said, perspective. I guess I would be happy with much less than you would be (I am actively looking into the tiny house possibility in Switzerland). I see 3.5 rooms/101 m2 from 1.2 MCHF just by typing into immoscout, and assuming you don’t have/want kids, that should be enough (+ a more thorough research might get better options).

Furthermore, as you keep separate finances, it would be fair you add in rent from your side, which allows for a bigger flat, since she increases her income (not sure if this is practically possible).

Also, having 600k as dry powder for an incredible RE opportunity which might come along the way is not too bad for a starting point. It sure gives you some flexibility which you would not have otherwise.

Finally, her money, her choice as long as you do not have combined finances. And you cannot impose life choices IMHO.

Side note : it is a deeply personal topic, I am just some dude on the internet. Not saying how you should do stuff, just looking into different perspectives. I have a similar issue, since my family in law is asking why we do not buy real estate (and parts of my family as well). I only get some weird looks when I explain opportunity costs, that their nominal gain on property price is mainly inflation, too much risk by putting everything in one object, that the rent to own ratio is out of control in CH etc.

She would like to gradually reduce her workload. Maybe start with 80%, then reduce further. I mean, most people don’t get up all pumped up to go to work .

Neither do I, but yeah, if we move to her flat, I should be paying rent. Many people don’t do that, though. Because it’s somehow tactless to “make money” off of your close ones.

I ran the numbers and I guess she could even get a 600k loan with her current income.

I will have to re-check, but I find it that whenever you dig into these postings, then either the place looks bad, or the location is not too sexy. To me, buying real estate comes with the stress of getting yourself anchored to a location. Because if you decide to move, it will cost you a lot of effort and money to sell and buy a new place. And using it as rental property means you need to pay back the 2nd pillar etc.

I think, as long as she works, she will live in Zürich. So buying a flat here makes sense. But if she invested in the stock market, and saw some big gains, she could retire early and we could move to Ticino, or wherever, and we could afford a considerably higher standard of living at the same cost.

How much is long enough is another question, but I guess if you rent out and buy somewhere else, it should not be a problem (basically just transferring the wealth into a new property.

Looking at gross income you state above, she would still have a very comfortable for a single person. With the starting capital she has now, she could achieve the first goal right now.

Well, I think you should push her to educate herself about investment and provide corresponding materials. Argue that doing something without understanding is not good and if she has money, it is better to learn how to use it effectively. Or if she doesn’t trust your knowledge, convince her to talk with an asset manager, Vermögenszentrum looks reasonably priced.

For now I would also suggest her to fill the 2nd pillar as much as possible. She gets tax deductions, it is growing slowly but doesn’t decrease, and in 3 years you can use this money to buy a property if you find one.

You can also try to convince her that she can have an immediate income from dividends that is automatically adjusts to inflation and market conditions while doing nothing and selling none of the assets. Taxwise not very effective, we know, but with 600k invested in for example

You sort of answered the question. 6% of 10-year periods have been negative for US stock market returns. There is no sure way to know whether the following 10 years will become part of the 94% positive or 6% negative. Given the current situation, I’d say anything less than 10 years is pretty risky, but for an 8-year term I personally would still consider investing some of my assets (20% or 30%) in stocks. But I’m an eternal optimist.

I would trust VZ. It’s a serious institution.

They are relatively conservative, which makes sense since they focus on soon-to-be retired clients. They don’t sell their own funds, and give back 100% on any commission they receive.

You basically pay for neutral, professional advice

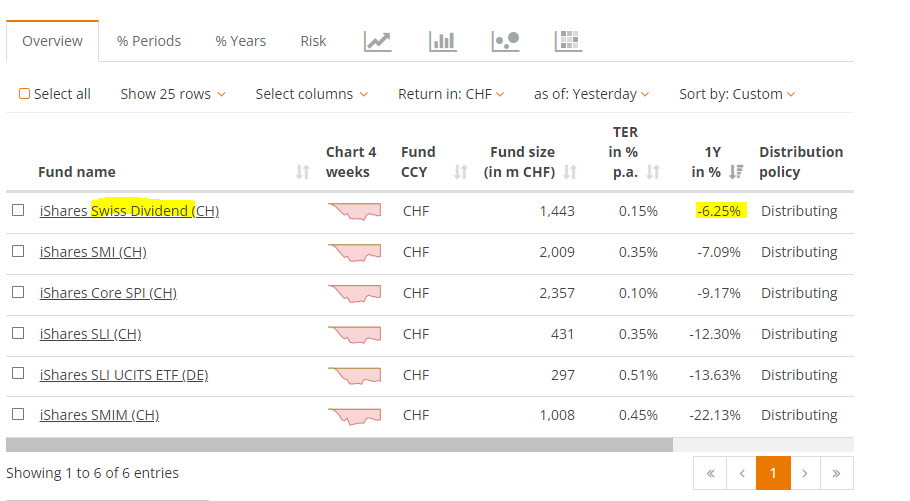

What does your screenshot prove? That in a recession, blue chip high dividend yielding stock drops more slowly and later? Well, yes. But we’re interested in a longer time horizon than 1 year, and we don’t want to only invest in the asset which loses the least at the start of a bear market. We want an asset that performs best over 20 years.

They don’t sell their own funds but they still sell their own wealth management solutions. They simultaneously mention that it’s important to invest with low fees and then try to sell their own wealth management with >1% fee. I no longer consider them neutral.

My screenshot proves nothing, but you might still be wrong.

Just like low TER, high dividend is like a guaranteed income, from profitable companies, as opposed to gambles on cash-burning “disruptive innovators” with poor performance prospects like Zoom or DocuSign, that are way too heavy in today’s indexes, hence in today’s portfolios.

A reasonable tilt towards low volatility and high dividend can help: -5% instead of -20% YTD is a large difference, that could lead to a large difference also in 20 year’s time.

A typical example: P/E ratios of the likes of Tesla are worrying. Tesla is treated almost as a blue chip now, is usually in the Top5 of S&P500 and has a market cap above Berkshire Hathaway despite a P/E ratio around one hundred.

thanks everyone, this turned into a bigger discussion, which is great.

Question: what about dividends? A good part of investing this money into VT is getting dividends. Any input on VT vs something else that pays better dividends especially if you invest a big amount of money?

The same answer to both: when a company is already generating huge cashflows and doesn’t know how to grow further and reinvest this money, it will return money to shareholders. If you aim for high dividends, you’re then aiming at companies at a particular stage. Historical data shows that you achieve higher overall return if you DON’T focus only on high dividend earners.

I’d say going for high dividend stocks is a form of timing the market, as these stocks outperform in certain scenarios, like at the start of a recession.

Before it turns into our usual argument, may I remind you that high dividend ETF was brought up by me in a discussion how to motivate your girlfriend to invest. So it is rather investing in some type of stocks vs. not investing at all.

Current indexes contain disproportionate amounts of crap.

A tilt towards profitable companies helps mitigate that.

It’s fine to burn some cash when you have actual growth perspectives. It’s not when you want to sell pretty standard products like videoconferencing or electronic signatures.

Tesla’s P/E of 100 cannot be reasonable, on any standard.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.