I was looking at Bond ETFs and if Hedged ones are better or not… But that’s not my question here.

I just don’t understand how the hedging works, or at least it doesn’t work how I imagined it to.

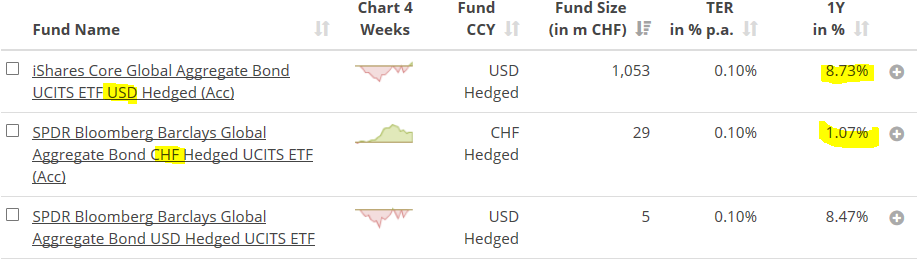

For example look at this 2-3 ETFs. They are all tracking the same underlying thing, but wo are hedged in USD and one in CHF.

Why is there such a big difference in performance? Epsecially considering that USD and CHF have almost been 1:1 in the last year? Does that mean the hedging to CHF itself caused 7% more internal fees? Could someone please enlighten me? Thank you.

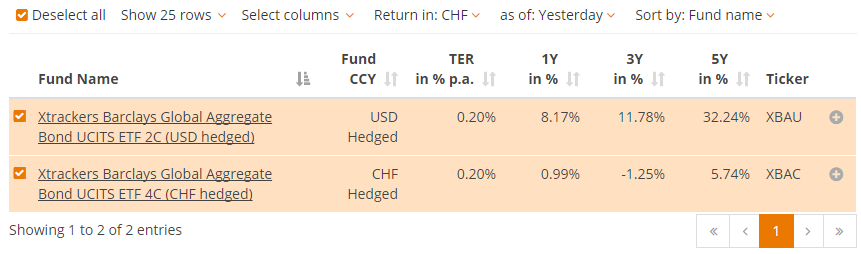

You got me, no idea why the USD one made 32% in 5 years, and CHF less than 6%. Maybe CHF hedging is just so much more expensive. Or maybe since probably half of the stuff is in USD, then they don’t need to hedge it, so it’s cheaper.

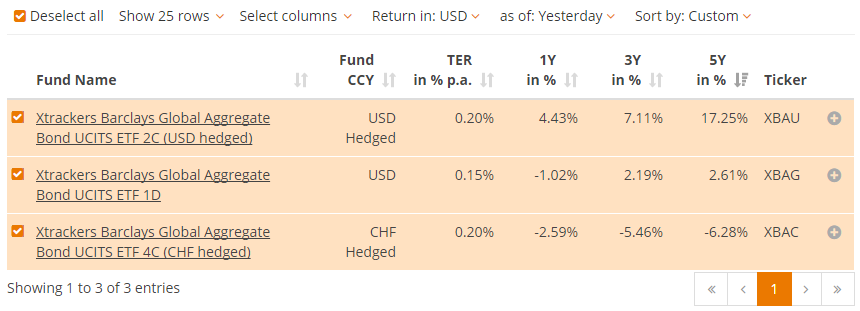

Here the unhedged one, and all returns in USD. The hedged USD one did a much better job than unhedged. I guess if you hedge and your currency gets stronger, you win. If the hedged currency gets weaker then you lose.

AFAIK, hedging cost is the delta between the interests rates of both currencies (so like 3% for CHF/USD). That’s the main reason why bonds don’t make much sense in CHF (CHF denominated or CHF hedged), for amounts where negative interests rates are not charged, holding cash will be cheaper (or you’ll have to go into risky bond territory to get a positive expected return).

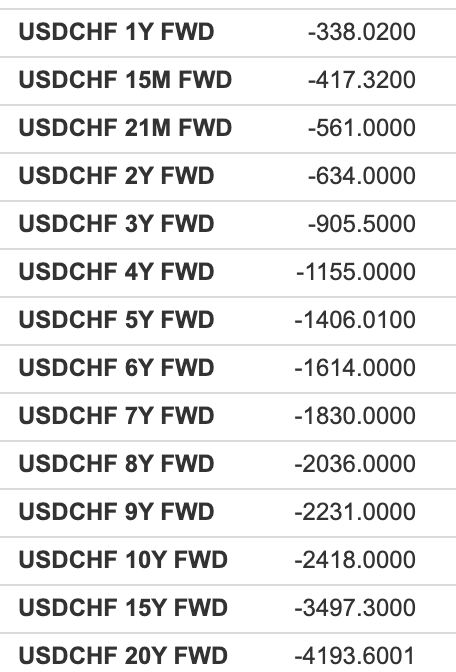

From what I understand of how forward rate works, don’t you need to plug interest rates for CHF and USD in the formula (and compound them over the period)?

Hedged stock market indexes are usually constructed to use with monthly forwards and roll the forwards every month

USDCHF 1M FWD bid -29.6900 ask -29.3400

This is in basis points and for a single month, so times 12 and at mid point means approximately 3.54% p.a. cost to hedge USD for CHF currently using hedged ETFs

They are not really predicting anything this far into the future of course, this is essentially options and the bulk of the cost you’re seeing here is option’s time value

No you don’t, because here it’s already kinda done. Here you already have the forward points, which is what the market is offering. There is a BID and an ASK.

This is how I understand forward points, if I’m wrong, someone correct me:

If you will have some future returns in CHF and you want to convert them to USD at the current spot rate, the forward points tell you how much CHF you have to pay today to be able to do it.

So you pay 338 CHF today and in 12 months you will be able to exchange 10’000 CHF to 10’000 USD (because today the rate is 1.00).

But if there is BID and ASK, then these are market prices, yes? So someone is willing to give you these rates. So, naturally, they have to be predicting what the exchange rate might be in the future, in order not to lose on that trade?

Big banks can sell you forwards, yes. Unlikely they take much risk for themselves in doing this, that’s not what banks do. There’s bond market where on one hand there are currently people willing to lock up swiss franks for 30 years at 0.2% interest and on other hand people willing to lock up dollars for 30 years for 2.9% interest, probably with some constructions these two kinds of people can meet and the banks will package it up for you as a forward contract, while taking up minimum risk for themselves in the process

I use 10’000 CHF to buy some USD bonds ETF hedged to CHF

The ETF provider converts these 10’000 CHF to USD at current fx rate

ETF buys USD bonds with these USD

They also make a forward contract for 1 month, so that when they sell the USD bonds in 1 month, they can exchange USD back to CHF at the current fx rate.

If they don’t sell the bonds in 1 month, they just make another forward contract.

Not bonds, currency forward contracts from some big banks. Securities from the original index + currency forwards is what you’re investing in with hedged ETFs.

The bank they bought forward from will do the rest of footwork to ensure buyers and sellers meet. At the end of the month when contract’s up they will settle the difference in cash: either they pay the bank or the bank pays them, and sign a new contract for next month.

But that’s what I wrote in point 3 & 4. They buy the original unhedged bonds from the index + they make the currency forward contract…

By reading and partipating to this forum, you confirm you have read and agree with the disclaimer presented on http://www.mustachianpost.com/

En lisant et participant à ce forum, tu confirmes avoir lu et être d'accord avec l'avis de dégagement de responsabilité présenté sur http://www.mustachianpost.com/fr/

Durch das Lesen und die Teilnahme an diesem Forum bestätigst du, dass du den auf http://www.mustachianpost.com/de/ dargestellten Haftungsausschluss gelesen hast und damit einverstanden bist.