Crazy

Monero is one of the coins that I feel is truly useful besides Bitcoin

Crazy

Monero is one of the coins that I feel is truly useful besides Bitcoin

Tokenization indeed. Creating a token on a bank’s private blockchain and available only in bank’s app, and selling it as something incredible.

…for gold that’s stored in their own vaults.

People who think that BTC might replace or take a fair share of Gold in WM portfolios also see it as an asymmetric bet to take. If it get there, yes its value per unit is expected to be way more stable as it would hopefully play its role as an edge against inflation and kind of a safe haven in case of political uncertainties. But its value would be a few multiples from what it is now.

I’m not sure if it has been mentioned but imho the biggest selling point of BTC relies simply in its unique story.

It’s the first successful experience of a decentralized cryptocurrency. It has no CEO. We don’t know who’s behind its creation (= no human point of failure). Satoshi released the whitepaper in a transparent way few months before he decided to finally plug in its bitcoin core open-source software. Which means that anybody curious enough and with sufficient knowledge could have join the party from the get-go or even tried to front run his ideas. No coin has been premined. And the cherry on the cake – in 2010 Satoshi which is the one who benefited the most from participating in the mining process from the very beginning disappeared completely.

Also, one of the most important points is that since nobody cared about it in its early days, it had the opportunity to flew under the radar when the whole thing was at its most vulnerable state from external attacks since the security provided by the Proof of Work consensus has the particularity of getting stronger and stronger as the network grows. And it’s been long since we’ve passed the point of no return on this matter.

This combination of factors is just not replicable by any other coin.

Having 96min (or 48 on 2x) worth watching Saylor…

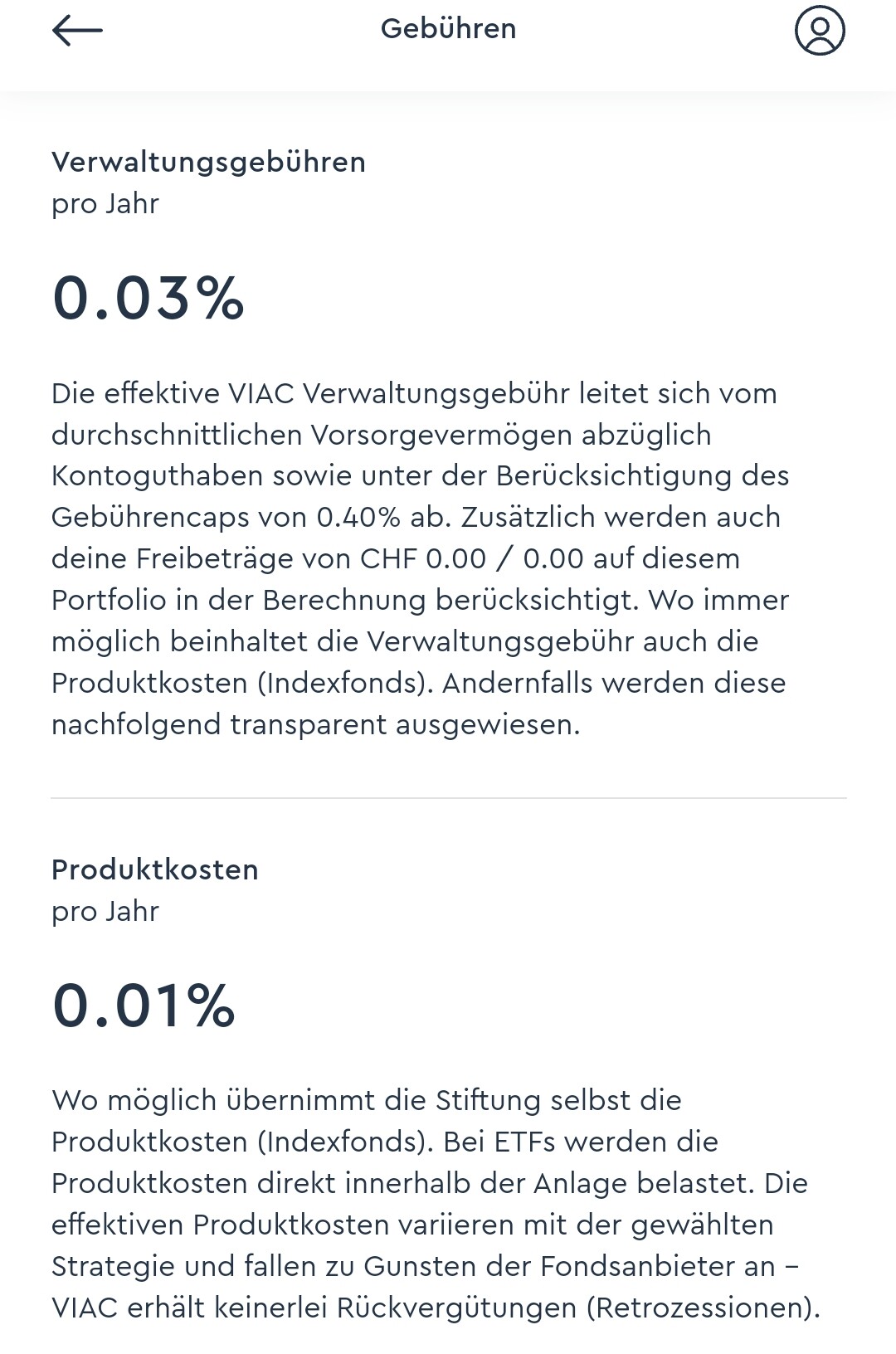

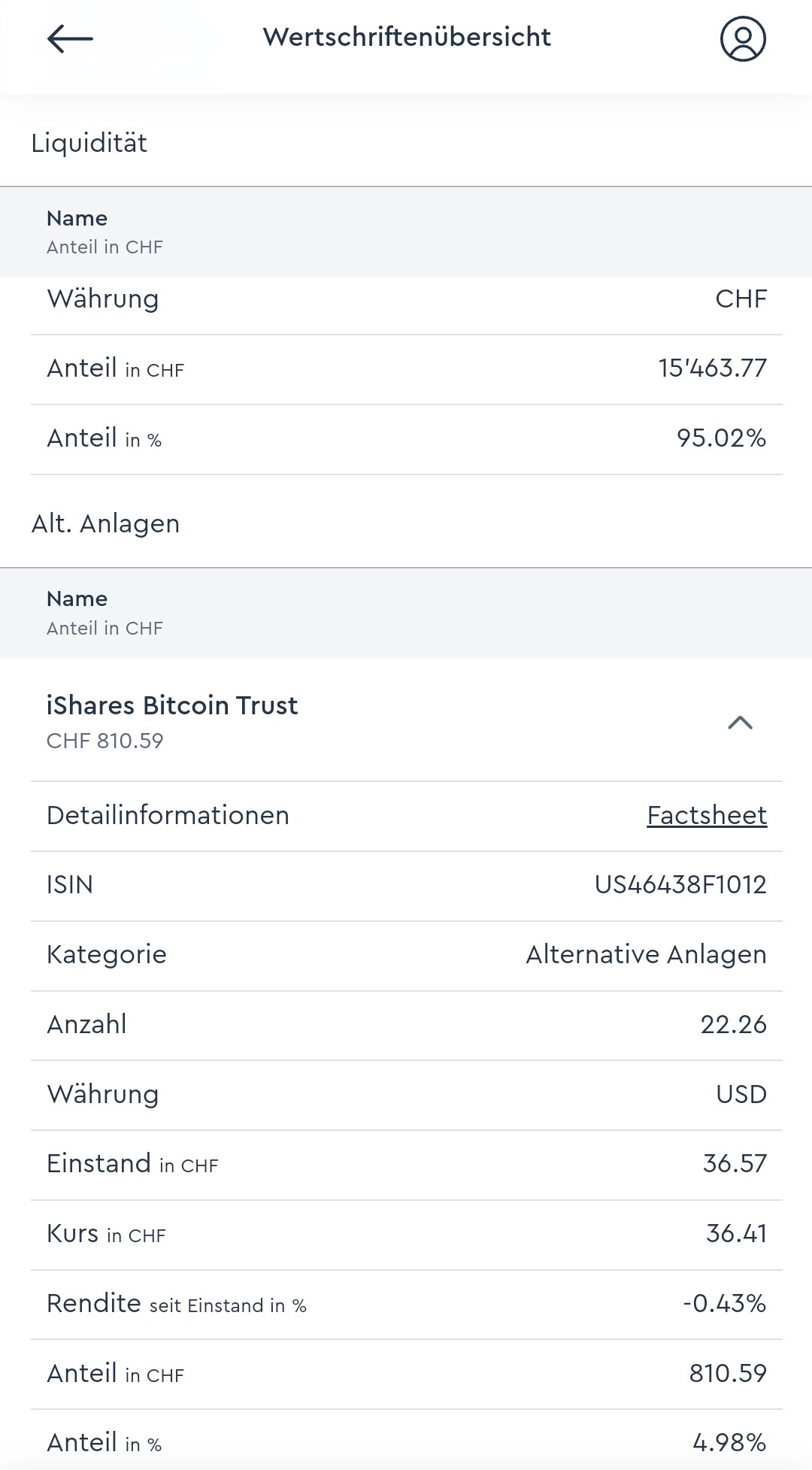

nice… it’s cheap. Having 95% CHF and 5% IBIT. 0.04% fees.

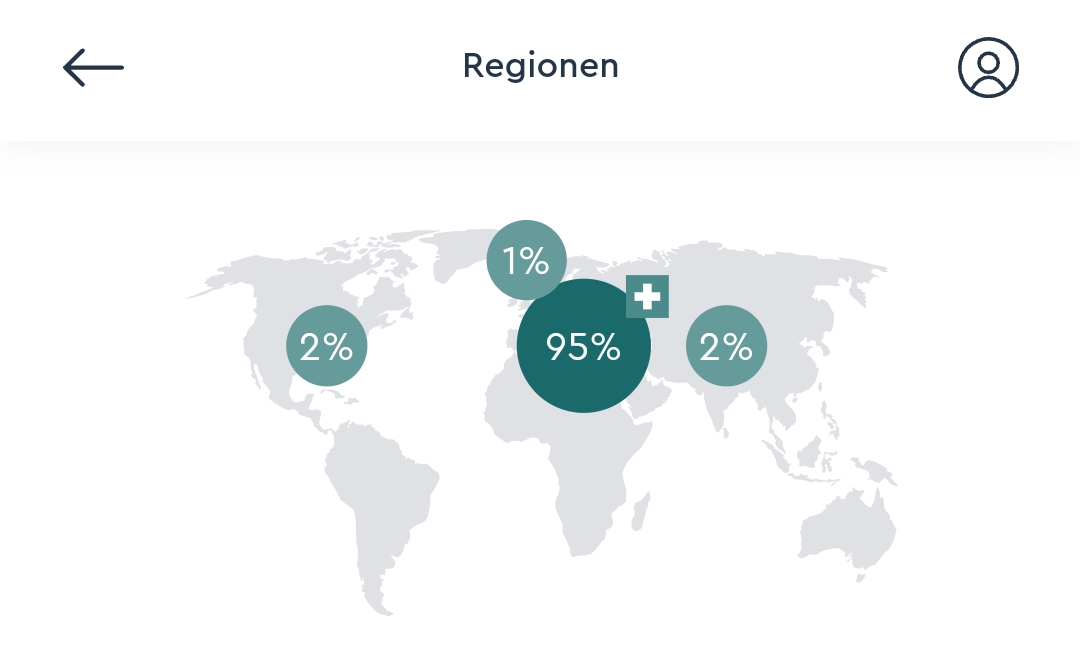

Still an open question: why is IBIT split into Northamerica 2%, Asia 2% and Europe 1%?

3A withdrawal tax is irrelevant for your asset allocation.

Here’s why: When you invest 1k that in 30 years become 10M… the government then (at 10% Tax) RECEIVES 1M. But YOUR COST is still 10% NOW, of your 1k aka 100 NOW.

You just invested your Cost of 100 that you realize now, you invested it for 30 years, and these cost over that time became to the million in cash that the Government eventually reveives. But your cost of investing into 3A is still already realized now and 10% of your invest aka 100.

This is the case as long as withdrawal percentages are static - which is the case if you have a certain 3A wealth. Tax progresson has a minor effect but it is offset by the wealth tax gain.

Thats a very interesting idea ![]() would you mind to once in a while report how that Portfolio develops? Would have thought that this should roughly give you relatively smooth 4-5% p.a.?

would you mind to once in a while report how that Portfolio develops? Would have thought that this should roughly give you relatively smooth 4-5% p.a.?

Will hold this one against it, this is essentially 40% Shares, 30% Bonds, 20% Real Estate and 10% Cash (including a 2% Gold and 1% BTC).

Return could actually be quite comparable as I expect it to yield about 4-5% p.a. But to be honest, your 5% BTC may come with lower Volatility. Will be interesting to see.

Screen shot on Asset Allocation comes once trading completed aka Tomorrow/after Easter.

As said, I like the idea of 5% BTC and then monetizing on volatility and re-balancing benefits.

Really curious how this gonna play out.

I don’t get what you want to tell me.

I never said the 3a withdrawal tax rate is relevant for one’s asset allocation.

I only said that it makes more sense to hold BTC outside of 3a instead of inside 3a, and I don’t see any reason why someone who wants to hold BTC does it in 3a instead of in his taxable account.

There is one: If one is only invested in BTC and doesn’t own stock ETFs/index funds outside of 3rd pillar. This person wants to maximize the BTC allocation.

So then, why not just buy more BTC outside of 3a? Why does he need to invest it in 3a?

Because by investing in 3a you get the tax benefit? So you are investing at a 15% or so discount.

I mean it’s the same thing with stocks or basically any other investing on 3a.

The other benefit of 3A is the absence of annual tax on wealth.

If the marginal tax on the wealth is of the order of 0.5 to 1% (it is close to this upper limit in my canton), after 10-25 years the cumulated savings is almost equivalent to the single tax on withdrawal ; of course the calculation is somewhat more complex, because the savings is on the value increasing with time, while the final tax is on the final amount.

So, I think that it makes sense to put in 3A an investment that has a probability to grow wildly.

Ok, let’s do some simplified calculations:

Assumptions

Case 1: Invest in 3a

In 30 years you have 10 Mio. in BTC, you pay 2.65 Mio in withdrawal tax, you saved 60k in income taxes over 30 years:

10’000’000 - 2’650’000 + 60’000 = 7’410’000

Case 2: Invest outside 3a

In 30 years you have 10 Mio. In BTC, you paid 1.71 Mio. in wealth taxes over 30 years:

10’000’000 - 1’710’000 = 8’290’000

Investing outside 3a will yield 880’000 more in 30 years. And this is assuming that you paid wealth tax on 10 Mio. for the whole 30 years.

Anything flawed in my simplified calculations?

Yes. In both cases you invest 7k every year which is flawed. Either you invest 7k in 3a and less outside of it, or 7k outside of it and 7k in 3a + something outside of it. The something depends on whatever marginal tax rate you used for your investment.

In essence, when you invest in 3a you invest 7k at a net cost of 5-6k. Or alternatively you can invest 8-9k at a net cost of 7k.

This has been discussed multiple times in this forum tbf. If one invests both in 3a and outside of it in both bitcoin and something that returns dividends then it’s better to try and maximize the amount of crypto outside of 3a if possible but this is all dependent on the portfolio one chooses. If one is 100% bitcoin for example then ofc the 3a still makes sense, even if for other more normal “strategies” it is suboptimal

You’re right, but I also left out another important factor that speaks against investing BTC in 3a, the management fees and the product fees for IBIT, which seems to be 0.04% at VIAC as posted by Stojano.

I’ll see if I find some time to make a more sophisticated spreadsheet.

Additional fees (over the “all-in” base fee) for IBIT at VIAC or Finpension are 0.25%. Stojano’s numbers are the fees incurred for the total VIAC portfolio, which includes 95% CHF at no fees.