I thought they were buying back their own shares…

They are, but I don’t think they’re doing enough. With this kind of discount, I believe buybacks would be more beneficial than opening new positions.

They were actively issuing shares when trading at a premium to keep it from exceeding 3% IIRC, but they don’t seem as concerned about addressing the current discount.

They said they created SSON as a the trust to avoid being forced to sell at unfavorable terms or due to liquidity issues. Since they’re opening new positions they clearly have cash available, that’s what I meant with my first post.

If anyone has good reasons for opening new positions at market value instead of buying existing positions at a huge discount (or even the new positions but just fewer shares), I’m genuinely interested to hear them.

There’s probably a good reason for their approach, but I’m not sure if it’s in the best interest of shareholders.

If they think the investments will make more money than the buybacks.

That might be a good reason to buy the new positions, but it’s a bad reason to keep the old ones. They could at least partially sell the existing positions at market value and use that cash to buy back their own stock at a discount.

The only explanation I can think of is that they hope by buying back shares slowly, without reducing the discount, they can increase the total number of shares bought back. But I was hoping someone might have a better reason, as I still think the discount is massive. Especially considering how they managed the premium and how long this discount has persisted.

Buying shares is both tricky, the discount irrelevant and share buy-backs are probably not ideal fr a tax point of view.

The Problem with a discount is that you only see the trading volumes that lead to the discount (aka how many shares were sold so thatvtge discount resulted). But unless they ask their shareholders, there is no way of knowing how much volume supports the discount. Meaning: they have no means of knowing how many shares they need to buy back in order to make the discount disappear. Worst case, they start the buy back and them realise that they can’t materially reduce the discount - and they lost trust in this process and probably attravt another wave of sales aka the discount widens.

Their mantra is that they care less about valuation but more about quality. That means that they don‘t care much about whether they can do a buy-back at a discount - as the discount simply doestn matter much.

In contrary, I wouldnt know tax laws in the Canal Islands but it could very well be that share buybacks were not that efficient. Be it tax, trading cost cost to destroy shares and later re-create them in case of a later NAV Premium… a shares buy-back was not efficient for them.

This particularely as the current discount actually simply was irrelevant. There is no negative impact.

Thanks for your input. I’m not sure if I understood you correctly and why you think the discount is irrelevant.

As far as I know buybacks are tax efficient and the fact that they actually hold 41 million of the total 171 million shares in treasury shows that they are not concerned with buybacks in general.

They can just look at their NAV per share and the order book to see how many shares they have to buy in a given moment to eliminate the discount. I don’t think they should do that to optimize shareholder return, but as long as their holdings are liquid enough they could eliminate the discount completely if they wanted to. And as their assets are small and mid cap stocks and not machines or something, they should be fairly liquid in comparison to their own shares.

So they could sell parts of the holdings or use inflows to buy every share that trades below the NAV per share price. And that’s what they are actually doing, I just think they should do it even more and with a different price threshold.

1 Like

Is anyone (still) buying any SSON?

Seems to be forever trading at ~10-12% “discount” from its NAV; and I hoped it would “catch up” at some point…

But I’m considering dropping out since it’s anyway a tiny portion of my overall portfolio.

Same issue like you, I got tired of it’s performance and sold it last year to buy RPI.L (also in GBP) instead for my fun portfolio. No regrets so far.

Not “(still) buying”, but (also) a bag-holder ![]()

Will hold on a while longer.

Strangely at IB this position as a “NT” symbol next to it since a few days, when hovering onto the symbol, I get “Restricted: must request complex or leveraged ET product permissions for trading. To close existing position, use the Close button”. Strange, since I originally bought it on IB, and it’s neither complex nor leveraged IMO.

1 Like

I just closed the position and it will go to Papa Smith (and maybe Buffett) on Monday (cash still settling it seems).

P.S. Same thing with the NT - couldn’t “Sell”, but could “Close”. ![]()

I’m taking this opportunity to note that this thread started in 2019. When we say that stocks are investments for the long term, we talk longer periods than that. Sometimes it’s a single stock or an ETF that underperforms, sometimes it’s the whole stock market that does poorer than savings accounts for longer periods of time.

If the goal is to not sell when stocks are down, it’s important that we believe strongly in our thesis so that it carries us even when the actual results are disappointing.

No beef, of course, with spending our play money however we want. It’s just that most of us have had precious few opportunities to really test our resilience in a down market and I’m taking every opportunity I can to remind myself that.

8 Likes

Hello, you’re right. But people have also the right to asset that they have been doing a mistake and closes change their positions. It can also happen If the investissement doesn’t reach the expectations.

I am personally an Happy holder of the base fundsmith fund. Still not convinced by SSON

3 Likes

Another year, another shareholder meeting:

3 Likes

Looks like SSON is winding down and the fund is closing. I received this message overnight

*“Please note that SMITHSON INVESTMENT TRUST announced reconstruction and voluntary winding-up of the company.

IBKR is unable to offer rollover option into a fund as this is done outside of Clearing-Systems, therefore your position will be applied to cash out option. There is no action required from your side.

To allow necessary settlement, your position will be blocked on 2026-02-03 after trading hours.”*

1 Like

I heard they were rolling over to an unlisted OEIC

Perhaps but IBKR cannot support it, if you hold via IBKR it will be cashed out

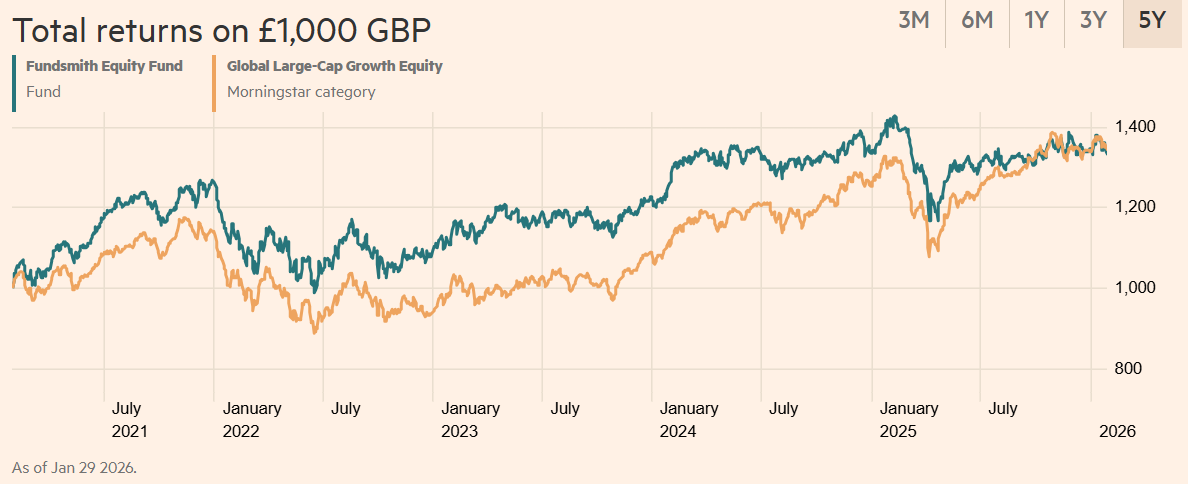

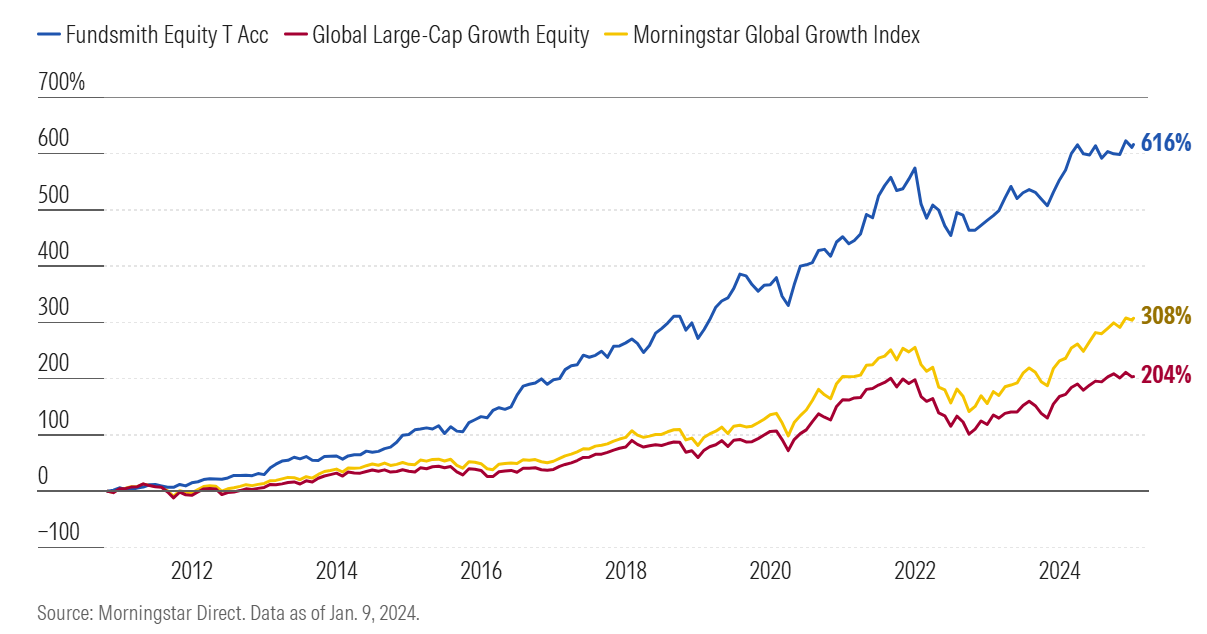

I never went into any Smith fund - was worrying Terry will phone up and say “Alright mate, didn’t get it quoite roight, did we?” - now I see it’s basically neck and neck with global large cap growth over 5 years, but absolutely blown it out the water since inception.

5 years

Since inception (missing 2025 as the source is from Jan 2025).

No liquidity, or appetite to go into GBP, but the long-term still seems good?

Very much on point

3 Likes

They announced it 2.5 months ago… If I were you I would follow my investments more closely. I personnaly sold all my SSON shares after the announcement, as the discount almost dissapeard instantly on that very day

1 Like

I fortunately did wind it down way before they did.

Fundsmith is still in my books.

Thanks. Where did they announce it? I never received any comms from SSON. Having said that you are right. My position anyway is very small. Less than 1% of my total investments