When I look at the big picture it gives me peace.

I might be the worst market timer on the internet, but I guess I’m still doing fine.

When I look at the big picture it gives me peace.

I might be the worst market timer on the internet, but I guess I’m still doing fine.

Any updates? Who uses ValuePension for 2nd or 3rd Pillar? Is an app coming? How is the reporting? Any downsides?

I’m using it for my 2nd pillar since 2 months. No app, but I don’t really need it. There are no further contributions, so it will stay like that for 40 years till I withdraw it at age of 69 or 70. I’m still loving the fact that you can set your own rebalancing bands. It’s currently at 100%, so there won’t be any rebalancing in the future.

Still waiting for the 3rd pillar solution.

Politics won’t change change anything. Has politics ever given the little man more freedom and scope to make financial decisions - unless that happened to benefit big corporate interests as well?

Pension fund contributions are mandatory - as such, the funds keep flowing into pension funds, among them the largest insurance companies (AXA, Zürich, etc.). And you can’t even choose choose pension you’ll contract to, since the employer will do it for you (lingering question: do you believe that your employer contracts with the pension fund that is most beneficial to you?)

Pointless for me. I don’t even have to bother looking into it, since only the top 10% or so of earners (among employees) are eligible. 127k/year an upwards. I’ll never reach these income strata from employment income (legally) in this life.

(Well, maybe if the figure doesn’t get adjusted and we see a hyperinflation)

I asked them once again to include Japan and Canada in their fund selection. Otherwise it’s still uncomplete! They have CH, Europe ex CH, Pacific ex Japan, USA, Emerging Markets. But those 2 are missing!

It’s not a big deal as you can take 3% SMI, 10% EM and 86% MSCI World ex CH to replicate VT. But I’m slightly deviating from VT and thus in need of those regions to be satisfied.

Just got the answer.

In short: Canada and Japan aren’t correctly listed in CHF. There is a CHF-tranche, but they have issues with the data-feed (no CHF price available from CS). So they can’t automate the trading. They are trying to simulate the CHF price using the FX rates from CS.

They don’t want to use the JPY or CAD dominated funds, like VIAC is doing. They don’t want to screw the customer over the FX spread costs of 0.75%. VIAC is doing this on purpose with the other funds, eventhough the CHF-dominated fund would be available.

Japan and Canada are making up 9.6% of the global market right now. That’s in the range of the market cap of all emerging markets combined. So we should definitely include it in our portfolio.

I guess VP didn’t include it yet because of the costs. It’s not as important as TER, but they are handling 2nd pillar money and if I recall correctly the avg. VP customer has 300k. 300k * 10% * 0.75% = 225 CHF.

But I guess VP will find a solution in the near future to use the CHF-nominated fund.

www.finpension.ch

3a is live. 0.39% TER. I just opened up an account and will test it now.

@finpension Any plan to reduce the TER of Valuepension to allign it with Finpension 3a ?

@wapiti No, there are currently no plans to lower it for valuepension.

Great thread. I am about to move my 2nd pillar and am still deciding between VP vs VIAC. A comment on market timing. Wouldn’t it be better to break your amount into say four 25% amounts and instruct VP to invest these amounts on the 1st of each month for the next 4 months (or even better once every 2 or 3 months). That would reduce the risk of market timing. I asked VP whether they could do this and they said yes and would only need the specific instructions. The downside of course is you still pay the .49% fee on the total balance whether in cash or not, and there is also a potential negative interest rate on your cash balance. If you followed this approach VIAC would presumedly then have lower fees at least initially given you will receive a positive interest rate on the cash balance and reduced TER since this is only charged on the amount invested.

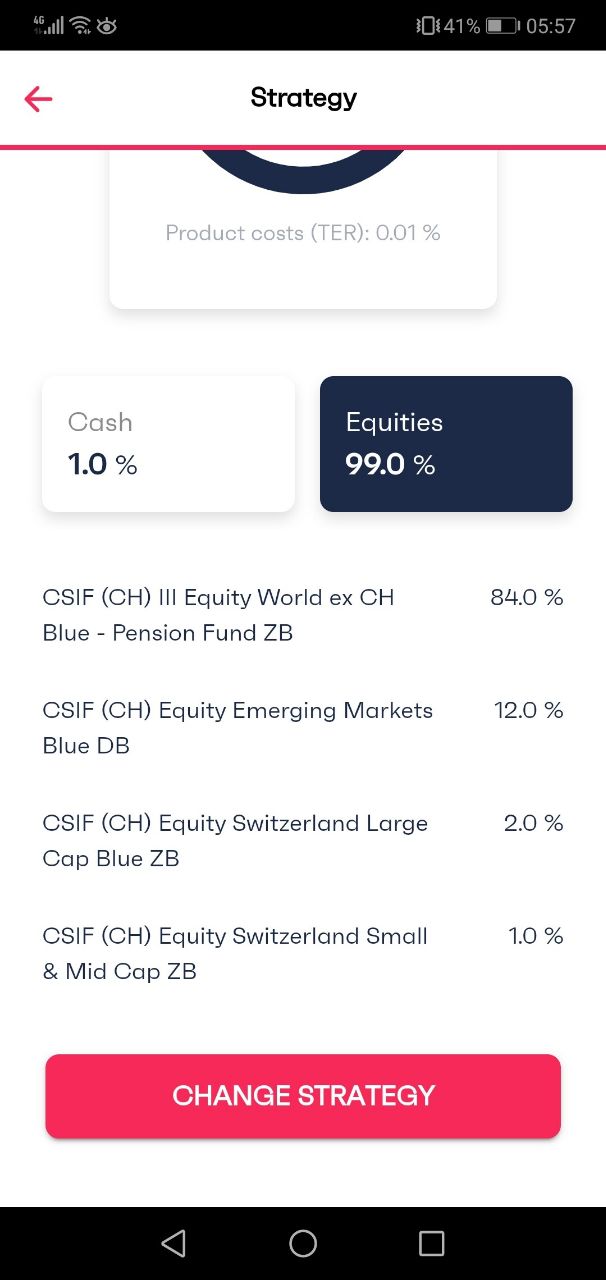

Just opened the account for this year’s 3a contributions and I love it so far. All very clean and smooth. Amount was settled within one business day so be aware of that small delay. Below my humble guess on a starting allocation. Should become active tomorrow morning via monthly reallocation mechanisms.

Very nice! Too bad we can’t rebuild VT like that in Viac.

How did this play out, eventually? You kept the money at ValuePension and transferred nothing to your new employer?

Was @TeaCup’s answer deleted or am I just too stupid to find it. What did s/he say?

What’s the latest news on the investment account vs. pure cash account?

Welcome @zips!

“News” in what respect of investment vs cash for pillar 2 & 3?

Gains, risks, costs, what is available,…?

I am transitioning job and need to decide where to put my 2nd pillar vested benefits. My latest Pension Fund will not keep it much longer, as my employment terminates.

When did you leave your previous job?