Some funds have no coordination contribution and some other funds adjust the contribution to the working rate.

The current deduction of coordination is 25’725.-

Let’s assume the salary is 60k at 100%, and 30k at 50%. An employee works at 50% and his age is 35. The pension fund employer part is 5% and the employee 5% (a total of 10%).

Fund 1 (Not adjusting the deduction of coordination):

30’000-25’725=4275.-

The contribution each year in the pension fund will be 4’275*0.1=427

Fund 2 (adjusting the deduction of coordination):

30’000-25’725 * 0.5=17’137.-

The contribution each year in the pension fund will be 17’137*0.1=1’713

The law defines a legal minimum (and maximum). Pension funds can operate quite freely within these boundaries, as long as the general principles are adhered to.

Let’s keep in mind that this is only the minimum old-age savings contribution. The contribution could also be higher than 10% - in fact, it usually will be, since there‘s also be risk premiums and management/administration costs to cover.

While pension funds are pretty regulated, there are still several options to offer a better pension fund for employees. For example:

Starting to contribute sooner than 25 (there are several that start at 20)

Insure more than the mandatory amount (>61k)

Contribute a higher % than mandatory required

Decrease the „Koordinationsabzug“ of 25k or even abolish it completely (some pension funds have special regulations like „if you earn less than 86k, 20-30% of your salary will be your Koordinationsabzug“ which is great for part-time or low-income employees)

Completely cover all risk-insurance related parts and thus 100% of the contributions/deductions are going into wealth-building

Many more…

So lets compare 2 completely different pension funds and 2 different employees in their early 30s. Pension fund A does the legal minimum and pension fund B doesn‘t have a Koordinationsabzug, insures the total salary and contributions are 6% by employee and 9% by employer instead of 3.5/3.5% (legal minimum for 25-34 year olds). Jonas is earning 140k and works 100%. Sarah is earning 50k and works 60%. Total yearly contributions:

Jonas at pension fund A: 4.3k

Jonas at pension fund B: 21k

Sarah at pension fund A: 1.7k

Sarah at pension fund B: 7.5k

These aren‘t just imaginary pension funds. These are real-world examples I‘m encountering every week in my job.

The biggest problem with pension fund A isn‘t even low contributions, it‘s low insured salaries. Invalidity rent is 65% of your insured salary. So it makes a huge difference how much is insured. Especially for Jonas with his 140k salary where pension fund A would only pay 40k/year in case of invalidity compared to the 91k of pension fund B.

So chose your employer wisely. It‘s not only about the salary.

Wow I find it concerning and it reinforces the need for an obligatory pension contribution as we have here in CH.

Just a side note, the Federal Council estimated that 12% of the population was on the strict obligatory scheme LPP, and 20% highly depends on the minimal conversion factor, as their over-obligatory part is rather small :

Environ 12 % des assurés sont couverts par des plans de

prévoyance fondés uniquement sur le minimum légal, et environ 20 % des assurés

sont fortement concernés par le taux de conversion minimal, car seule une faible part

de leur avoir de vieillesse relève du régime surobligatoire.

What about the 1st pillar? Is there an easy way (i.e. without having to send letters etc.) to understand how much you have accumulated in benefits as of TODAY?

Well for one thing the students are going to be voters one day and it would be nice if they don’t just eat up any bullshit economic plan the politicians are peddling.

Researchers found a distinct Swissness factor in investment decisions when comparing Swiss-Germans to Germans, Swiss-French to French and Swiss-Italians to Italians.

Based on a large international survey we analyze how German- French- and Italian-speaking Swiss differ in their investment decision behavior and investment competence as compared to their closest neighbors abroad speaking the same language. Although language may be closer to the individual self than the country of residence, we find that there are greater similarities in the decision behavior of Swiss speaking different languages than between Swiss and their linguistically closest neighbors abroad. These similarities hold also for the emotional investment competence and to some extend also for the knowledge-based competence. We conclude that there is Swissness in the decision behavior as well as in the emotional investment competence. The latter is associated with regional differences in the relationship to investment advisors.

Well, I would expect the tax system and the available vehicles to play a greater role in investing decisions than language, and also for the educational system, wealth level and general society to also play a big role in “emotional decisions” and financial knowledge so I am not very surprised.

The first guy was a 70-year-old professional chef with a Social Security check of $1,400 a month. He had been working 12 hours a day for 6-7 days a week until age 63 when he went into the hospital with a heart issue and then never worked again. His financial plan prior to that event? To work until he died. Thus, no savings. He had been making $8,000 a month; that’s almost $100,000 a year. And now he’s living on less than $17,000.

Please, don’t complain about 2nd pillar. More efficient - yes, removing it - no.

If you’re not going to save for retirement, your TV is going to be your entertainment.

Sacrifice when you are young or sacrifice when you are old, but you will sacrifice.

Damn this is the nightmare many people don’t understand: working like a dog for 30-40 years and then struggling.

That, I don’t know why it’s so hard for people to understand, being old and infirm is bad enough, adding being poor on top and one might as well jump off a cliff. Have seen way too many people in my immediate surrounding getting hit by financial and health-related hardship after 70, ain’t never happening to me.

I saw recently this article. The main idea we know - who doesn’t take care about their financial situation, will have difficult time when old.

My attention was attracted by another thing: they quoted some studies where people’s financial knowledge was evaluated:

Selbsteinschätzung vs. tatsächliches Wissen

Die Resultate einer neuen Studie der Hochschule Luzern lassen aufhorchen.

…

Laut Studie bekunden über 70 Prozent der befragten Personen, dass die berufliche Altersvorsorge ein wichtiges Thema sei. Doch zwischen der Selbsteinschätzung und dem tatsächlichen Finanz- respektive Vorsorgewissen wurden erhebliche Lücken festgestellt.

Ein Drittel der Befragten schätzt sein Finanzwissen als hoch oder sehr hoch ein - vergleichbare Werte wurden beim Vorsorgewissen gemessen. Aber: Weniger als 20 Prozent der befragten Personen konnten alle Finanzfragen richtig beantworten. Die Beantwortung der Vorsorgefragen fiel noch schlechter aus.

Beachtlich war auch der Anteil jener Personen, die überzeugt waren, die richtige Antwort zu wissen. Je nach Frage betrug der Anteil der Falschantworten bis zu 50 Prozent. Probanden hätten im Fragebogen einfach die Frage «weiss nicht» ankreuzen können. Solche Personen sind sich der eigenen Wissenslücke gar nicht bewusst - mit der Folge, dass Fehlentscheide getroffen werden.

This let me think: as a personal finance autodidact, how do I know that I know right what I know?

I don’t want to go into the philosophy of knowledge, but would like to ask a practical question:

Is there a free online test about (personal) finance, ideally with Swiss specifics? I am sure I can find a USA-specific one with a click.

I don’t want to take an online course or pay for an advisor, but would really appreciate a possibility to evaluate my (presumably high) knowledge of personal finance in Switzerland.

But going deeper, how do I know that you know what you claim to know? I can also create a test about African art of 16th century. What are your credentials?

After posting my previous post, I found 3 online test about finances in German. 2 were for 50% thinly disguised advertisements. Another one seems honest, but one question, I am pretty sure, had an error, and some where in a style “what is the difference between EBIT and EBITDA”.

In the spirit of the study, me being overconfident could probably answer most of that correctly. The answer often starting with “depends on…”

The one where I’d struggle out of the blue is “Vorsorgegelder im Nachlass”, but I’d be able to read it up for cases like voluntary buy-ins (should be yes, voluntary buy-ins are paid out?).

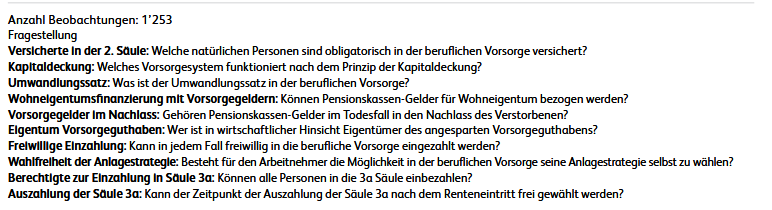

Looks like the questions in this specific study were specifically about pension savings and pillars. Seeing the question “Eigentum Vorsorgeguthaben”, I am remembering notes that a huge fraction of Swiss population does not realize that 2nd pillar belongs to them. So you see the level.

About this specific question, I think they mean to ask if pension savings are added to general inheritance. I will try to give the expected answer: they are not.

Second pillar is converted to a pension for the remaining partner and children.

Third pillar balances are paid exclusively to the spouse first. If there is none, there is a sequence of beneficiaries. One can also designate the beneficiary of 3a balance in case of death. Point is, it is not subjected to the obligatory separation of the general inheritance, i.e. min 25% to children etc.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.