Subject Matter Expert

1 Like

I feel it’s mostly FI allowing me to take this stance.

And perhaps the a bit regrettable acceptance that a “get things done” attitude benefits most (1) my superior(s), (2) the company I work for, and, perhaps, (3) me. In that order.

Your_Full_Name’s Law of Merit at a Big Company. And maybe even at some smaller companies.

From a personal POV I historically definitely veered into the “get things done” camp. This was especially so at the beginning of my time at the GOOG. It’s just the way I’m wired.

For many years I didn’t want to believe that Google had slowly turned from a meritocracy (you benefit from you things getting done) into following the Law of Merit at a Big Company. Lots of personal time and well-being wasted.

I’m not doing this anymore despite my personality because I can afford it.

I can’t really speak to the angle of losing career aspirations (aside from being able to not have them because of FI).

2 Likes

Quick update if anyone beside @rolandinho is interested:

TL;DR: Still FI, working part-time, currently evaluating further continued employment by my current employer, considering going full private.

For those reading along but haven’t followed the thread: I am FI, currently working part time at an asset management company, partially for learning how the professionals do this, partially for initially being uncertain about whether my investments will cover our expenses.

What’s changed since my previous update (March '21)? Using the same categories as last time …

- Family: I am able to commit more time as needed to look after things. I am glad I am able to commit the time, as my son is coming of age, which comes with its own challenges that I didn’t expect to be so difficult for me to handle. Not so much my son’s fault, more the way I am capable of dealing with it. Definitely glad I have the time.

I believe at my old job at Hoolie I would have either not picked up on these things at all because of too much committment to Hoolie or - more likely, as I did cut back on mental committment in the trailing year or two - would have picked up on it, but would not have recognized it in time as an issue I need to dedicate personal time to to help address.

On a more positive note we as a family in 2022 spent precious time together on awesome vacations, including a two week trip to Africa. - Perspective: probably even more hard-line on this one. Developed only very little tolerance for negative work-space interactions, expressing myself accordingly, and my environment is even adapting to my expectations.

I am still asking myself regularly whether I still want to experience the remaining marginal corporate drama that occasionally occurs. Will probably answer this question this year. - Risk tolerance: I am a little afraid of my beating the S&P 500 by over 20% in 2022 with my stockpicking portfolio will make me overconfident. Recency bias, pure luck, whatever. Anyhow, I would like to move more funds from more conservative allocations (globally diversified equity and bond ETFs) into my stock picking portfolio. Will have to see how this plays out. It’s a nice challenge to have to deal with.

- Perspective II++: managing your own money is so much easier than having to manage OPM (Other People’s Money). My Portfolio Manager colleagues at my current gig all ended up negative for 2022, some even trailing their benchmark (usually some index). Not being bound by such constraints as an individual investor I feel I can easily navigate current market inefficiencies and generate alpha. Famous last words …

Additional thoughs:

- pursuing a dividend (growth) strategy has definitely given me ease of mind: income though (growing) dividends financing lifestyle trickles in and is growing, and I don’t have to think about selling stock, especially when markets are depressed.

This concludes today’s updates. If you have follow-up questions, please fire away.

25 Likes

You make me want to pick up stock picking again too. I’ve watched some FastGraphs videos and it seems that tool really makes it rather easy to find those dividend grower stocks.

3 Likes

I have not recognized its @Your_Full_Name in this topic as well. Therefore not only thanks to the valuable insights into the stockpicking topic but also this one.

Very inspiring to read your journey, specially also around the impact on the family. Thanks to WFH I spend a lot of time with my boys (4 & 7) however currently they are happy with me just playing with them but I usually it’s small kids small problems, big kids well you know.

Looking forward for more interesting insights

2 Likes

I am far from FI(RE), but this part the discussion with @monkk has my full attention…I’m at a similar crossroads : I’m also an SME and until recently, I was able to see very good correlation on my progression the past 10years based on results of my work ethic to increase my expertise. Now, I think the the situation you both describe is happening to me too. Its probably normal since I’ve reached a level of seniority that would make progressing more a very big new investment, when a divorce is my biggest risk to my FI currently…should that happen I think my position on looking for a promotion would probably change ![]()

So assuming I stay in the status quo, its reassuring to see your posts* if i should become a guy who keeps his head down while focusing on not becoming complacent in my expertise. Not sure I am wired this way though… as my wife’s salary has more potential to grow proportionally at this stage its worth trying while I really shift focus to quality>quantity on our expenses.

*Thanks for the honesty and transparency on the journey as well as the results which I will be looking at attentively to learn from your experiences @Your_Full_Name

7 Likes

Is it worth it or how do you justify it? You are getting dividends taxes as ordinary income after all?

Also, would you mind giving more details/names of dividend stocks you hold? I need to park some margin cash and was looking in preferred shares, but these are mainly financials in US.

2 Likes

There’s an entire thread on me picking stocks and a live view of the holdings I have in my stockpicking part of my portfolio* if you are interested in more details.

The TL;DR to your questions: it always depends on your personal circumstances (duh).

In my case I feel it’s worth it and it’s justified by generating passive income in the high 4 figures and closing in on 5 figures per month. If I didn’t touch my stockpicking portfolio anymore, I’d expect on average an at least 5% higher total dividend income every year (currently the rate is above 8%). As already mentioned, I find it very appealing not having to sell any equity to generate steady income (e.g. now’ish would not be my preferred time to have to sell).

Yep, full income tax payed on this (in Switzerland).

I wouldn’t park cash in this strategy unless your holding horizon is at least 3-5 years and you are willing to spend some time picking the companies.

* Use the list at best as an inspiriation, not as a buying guide. A bunch of the companies in that list are now overvalued and I wouldn’t buy them at current valuations (e.g. Coca Cola, KO) or because they haven’t increased or even cut the dividend (e.g. Compass Minerals, CME).

2 Likes

Do you / Did you own a company? Or how did you get to 3.6 M AUM?

Even if one has a really high paying job, this seems quite unreachable for most ![]()

He worked for Hoolie for a long time → FI(RE), pulling the trigger likely in 2020: ~50, male, married, one kid

which paid extremly high salaries

1 Like

Worst is for people who want early retirement: you have the low accumulation rate, but don’t get the nice conversion rate as when you retire, you have to pull out the amounts into a VB account and just get a lump sum.

2 Likes

Compounding 5k per month for 25 years can get you there. So if you start in your 20s, you could conceivably do it before turning 50. I only wish I knew at 20 what I knew now - I ‘drifted’ for a big portion of my life. At least I was growing my career and had some kind of forced savings through buying a house. But I never invested into pension (except minimum forced amounts) or stocks until recently.

1 Like

You’ve to be realistic here.

Only few people can save 5k chf a month in their 20’s ![]()

The compouding theory is interesting but faces reality

2 Likes

I would argue that it’s highly unlikely to be able to compound 5k per month in your early 20s ![]()

It’s interesting how our minds are not able to grasp the exponential effects of compounding.

E.g. most people would prefer getting CHF 10k a day for 31 days over CHF 0.01 doubled every day for 31 days.

The first one leaves you with CHF 310 k.

The second one with more than CHF 10.5 Mio.

Would be great, buy a bunch of bitcoin, wait a bit, sell, done ![]()

who said anything about early 20s ![]()

though even if you can’t reach 5k in your 20s, you can catch up in your 30s.

1 Like

Not grasping compounding is one thing. There’s another class of people who argue that taking the 10k a day is better because you might die in the 2nd week… YOLO!

2 Likes

He/ she is in their ~50s and stock market returns have been incredible.

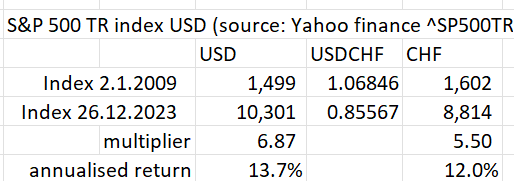

S&P500 Total Return from 1 January 2009 to end of 2023 is approx 14% p.a.

$1 invested in Jan 2009 is now worth 7 USD assuming reinvested dividends and before taxes

1 CHF invested in Jan 2009 is now worth 5.50 CHF

1 Like

I can confidently vouch for the person being a he.

I would attribute my net worth to “dumb luck” rather than skill or overall stock market return: had I known about investing I would have gotten rid of the Hoolie shares (for diversification reasons) the moment they vested (or the first day the blackout window* ended or would have later opted for the automated selling when that was introduced for Hoolies in Switzerland.

For the longest time, however, I looked at those Hoolie shares as “something extra maybe some day” tucked away. I wouldn’t even really look at them for years and only sell some to cover taxes.

Once I started to become interested in investing and later FI I realized that I had probably 95% of my net worth (outside pillar 2 and 3a) in those Hoolie shares and that I should perhaps diversify.

So the “dumb luck” of concentrating in and holding onto most of my Hoolie shares from 2005 to close to 2020 made sure I fully benefitted from Hoolie’s meteoric rise over that period (easily outperforming the S&P 500).

By the way, had I stayed “dumb” lucky" all the way through to today by not, ahem, … diworsifying away from Hoolie shares, I’d probably have joined the eight figures club. ¯\_(ツ)_/¯

Fun fact: I initially took a pay cut going from about 140k to 120k in order to work for Hoolie in 2005 …

It’s only after maybe 2010 when salaries started ballooning (out of proportion, IMO [but I won’t complain ![]() ]).

]).

* Typically a month before and after Hoolie quarterly earnings.

1 Like

Sorry for my ignorance, but what company is Hoolie? I‘m too dumb to find any (stock-) information.

No need to apologize, and I actually misspelt it: Hooli (which I haven’t watched). Stands for big Silicon Valley tech company, in my case a company mainly known for its search engine.