It is strange that they cap the calculation to <$1m pension. Although that sounds a lot, when you consider inflation over multi-decade timeframes plus compounding of investments, having 7 figure retirement pots should not be uncommon.

1 Like

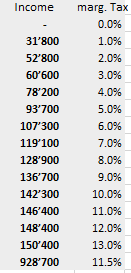

No idea. It was shared on forum but it matches the proposed rule.

I think because kind of took 3a number in consideration…

yes, this can be quite high for some folks… specially for 2nd pillar.

Yes (to statement) and no (fare much worse). You’d only pay half, some 5k instead of 10k.

1 Like

It’s due to the progression.

Even with “only” 500k you are high up in the progression, even though you get taxed only on 1/5 of the rate.

With the fictional translation to income, you benefit from the first 636k being tax free if there’s no other income considered. Only then the progression starts to climb, either with much higher capital or with other income.

As said, I’m using the married table, but the idea is the same for singles.

Anyway, it’s purely speculation for now.

1 Like

They explicitly mention they’d have to take care of the “timing” optimizations so they’re aware of it. I suspect that’s the kind of things that makes the proposal doomed, because it’s just too complex to implement (how would they figure out when people “optimize” their income, what if you take a sabbatical, are you optimizing? do you take the average over the past 5y? etc.)

4 Likes

Agreed

Inclusion of income at time of withdrawal makes no sense anyways. With current proposal, person with capital withdrawal of 1.25 million & annual income of 100K would have higher extra burden versus person with 2 million withdrawn & 25K income. And who is to say that just because someone has higher income for that year, it would continue for many years.

Rules should be independent of income of the person withdrawing capital. This would also keep the principle of capital taxation & income taxation separate. And this would avoid people being creative

I think what might make more sense is to simply increase the federal taxes for capital withdrawals if that is really really necessary. And if for some reason people with high balance need to be penalised more then this can easily be done via higher federal tax for higher amounts

Not that I want tax increases but the principles should be kept intact to avoid other problems

8 Likes

I for one am fascinated by the first row view into the sausage-making just by the Mustachians in this thread.

Imaging the blood in the parliamentary butchery and guts spilled in the Bundeshaus when this sausage is finally made at the federal level … ![]()

![]()

![]()

5 Likes

I think something simple like that would be most acceptable and easy to implement. Maybe even 10 years.

Tax law never let sense get in the way.

In truth, I think the current system works fine. If they really want to increase the tax take, then maybe instead of using 20% of the withdrawn amount as the base, they could use a higher number e.g. 30%. Then you just change a single number instead of re-writing the whole rulebook.

2 Likes

Political actors have started to move. I just recieved a call to sign a petition against this proposition through FDP/PLR channels. Everybody can sign online.

German: https://www.nein-zur-vorsorgesteuer.ch/

French: https://www.impot-prevoyance-non.ch/

9 Likes

So has it already been decided by the parliament or why are they collecting signatures (for referendum)?

I assume to show that there is significant opposition and if the proposed measures are implemented it would be met by a referendum. Just a warning to those who want to implement it that they should rethink the proposals and is not as easy as imagined.

8 Likes

That proposed change is going to be dead on arrival. FDP now tries to kill it even on it’s way to parliament for political points.

4 Likes

Which is a good thing imo. Shows initiative and that stuff like this will be extinguished in its tracks, to not try again.

8 Likes

Employees who have made large voluntary contributions will have massive incentive to resign and withdraw 2P/3P before the new tax becomes effective. One outcome will be resignations to become self employed or leave the country - not good for national productivity.

If there is no longer a meaningful tax saving by investing in 2P it creates a disincentive to work.

There will also be a one-off distortion in the property market

4 Likes

I doubt the number of people that this would apply to would have any meaningful impact on the country as a whole.

6 Likes

I don’t have data but I would assume a majority of high earners make voluntary contributions to 2 and 3 Pillar on the basis of tax savings

These high earners with big pots will surely correlate to the most important and senior employees in the economy (managers, bankers, IT … ) and in society (Doctors,…)

IIRC the amount of tax they hoped to raise with this measure was not large and could conceivably be off-set by the above impacts

1 Like

I’m not convinced about how much people really contribute to their pension. I think most people, even high earners, tend to live paycheck to paycheck.

Even if they have large pots, few would be willing or able to forgo their future earning potential to save a bit of tax.

Where it could have an impact is at the margins if people are anyway close to retirement and can pull that forward a few years to benefit.

But remember also that super high earners are probably the ones that just working one more year would more than cover the extra tax.

I agree and I would not underestimate the potential consequences. In the UK a couple of years ago there was a problem with consultant doctors being incentivized to take early retirement due to a change and pension contributions no longer being tax efficient.

Like the consultants above who effectively faced working for free on an after tax basis, or worse ![]()

3 Likes