Why are you questioning this? Are you not willing to pay your fair share? /s

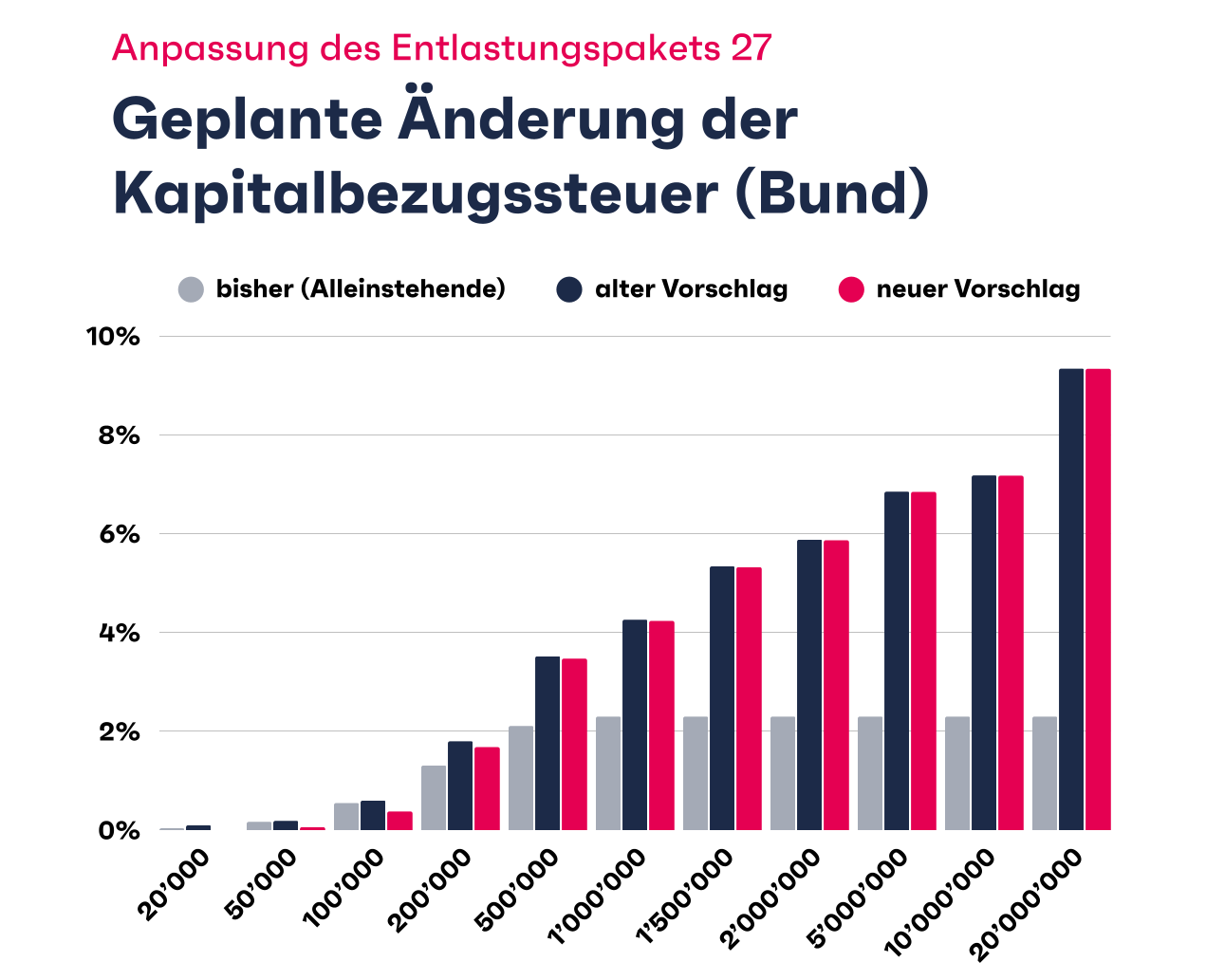

From Finpension (on LinkedIn):

3 Likes

Don’t tell anyone, but when you visualize it like that: Currently taxing 20m the same as 500k, and when you can save up to 13% during buy-in or compared to getting a pension, 2% is kind of ridiculously low ![]()

3 Likes

Especially since if you have 2M you probably contributed at top marginal tax rate.

Edit: that said top marginal tax rate for Bund is 13%, so not a big win if you have a 20M pillar 2 ![]()

Weighing up against that is the fact that you make your funds inaccessible for a long time and have them trapped in low yielding investments.

It’s unattractive unless you get them out into a VB with Finpension or VIAC.

It’s been debated to hell, not everyone wants to be in 100% stock ![]() lower volatility and yield can be good too.

lower volatility and yield can be good too.

Yes, having your low vol/bond portfolio in the Pillar 2 would make sense.

Maybe I’ll change my mind if I’d get closer to 20m then to 500k, but 20m-pension-fund-heavy me could probably stomach having some assets locked-up and low-yielding. ![]()

Ok enough from my side, the whole thing is still in debate. ![]()

4 Likes

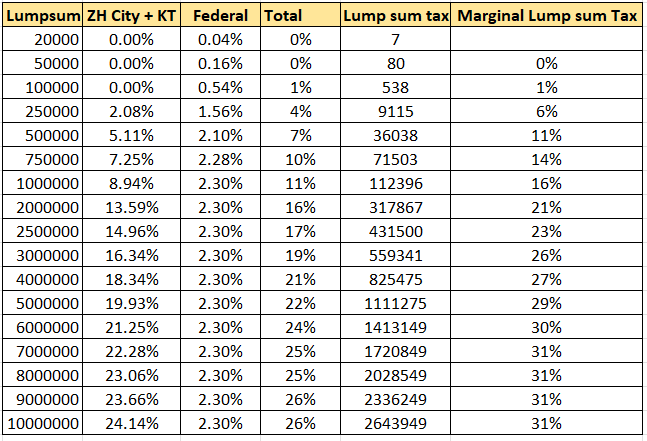

Here is the table I calculated for Marginal Tax rate. I used the data from ESTV and assumed Single, no children, ZH City , no church.

The marginal tax rate is assuming NO Change in Federal Taxes. If the Federal taxes increase, the marginal tax rate will also increase.

So if your pension pot grows to between 2M and 5M , the marginal tax would be between 21% and 29%.

The tax is mentioned as Total % in 4th column.

The marginal tax rate (last column) implies what’s the lumpsum tax you will pay for that last tranch.

For example -; let’s say your projected 2nd pillar is 750,000 and then you make 250K voluntary contribution and now the projection is 1M CHF. The additional 250K will have 16% marginal tax.

On average it’s still 11% for full 1M.

I think when someone is making voluntary payments, they should look at marginal lump sum tax rate and not the average

Seems to me the authorities are considering 250k-500k, 500k-1mn, 1mn-2mn as the key milestones to increase the tax rate. Seems very reasonable and pragmatic.

Yes because most people will be in lower brackets and hence vote can pass easily. It’s easy to vote against the minority ![]()

2 Likes

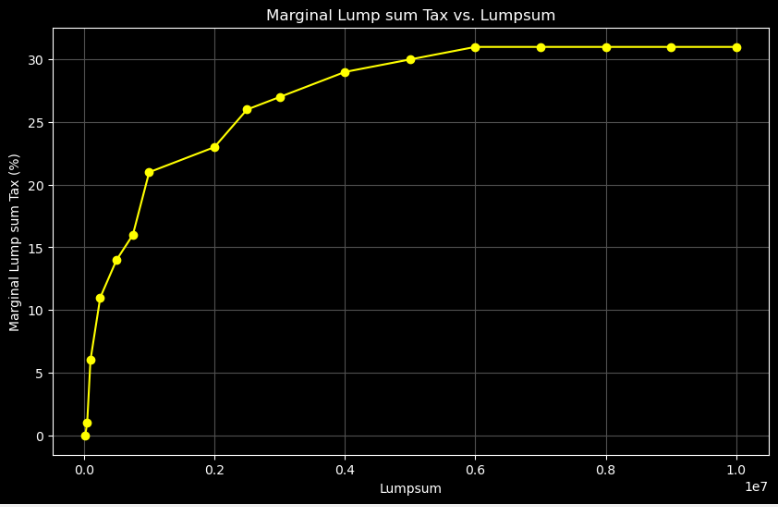

You have a linear ramp from 2.5M to 6M after which it pretty much tops out.

Between 0 and 1M is a very fast ramp up.

Yes it’s crystal clear from the number, that’s what I saw but a picture is 1000 words!

And it makes sense because I guess that’s where most people will fall in (up to 1mn).

I like these charts as the tax you pay is represented geometrically as the area under the line.

So if you look up to 1M, you have a triangle. And from 1M to 2M you have a rectangle of about this same height.

So combining the 2, you’d expect the tax at 2M to be about 3x the tax at 1M, which from the table is approximately correct.

1 Like

Now you are showing off your math skills ![]()

2 Likes

Ah yes the old quip “all taxes are flat if you earn enough” ![]()

Note that many cantons have a very different progression compared to Zürich (Zürich is one of those with steeper progression)

3 Likes

So, ideally, one is withdrawing every CHF 99’999 from 3a (e.g. reducing Saron mortgage with it, then increasing the mortgage by 100k, then amortizing again with second CHF 99’999 batch and playing this game every 5 years)?