As the legendary Peter Lynch once said, “Far more money has been lost by investors preparing for corrections, or trying to anticipate corrections, than has been lost in corrections themselves.”

But do whatever gives you peace of mind.

I don’t see growth stock crash and burn, there are a lot of great companies, growing really fast, providing a lot of value. They probably will stall at some point in the next few years, and if there is a burst, I think it will quickly rebound back up. Just my opinion.

To me it’s a big mystery why we see no real inflation. I mean, it’s logical that real estate prices are sky high (low interest rates), it’s understandable that BTC and stocks are sky high (“stimulus” programs, printing money(1) ). But you would think that it’s just the nominal value that’s inflated. There is much more money than a few years ago. Why are consumer goods still at relatively the same prices?

So maybe you will see the bubble pop, or maybe finally inflation starts catching up. Stock prices will stay as they are, but consumer goods go up. Cash is trash, so people have been buying whatever else they can, that they don’t have to store at home. How else can you protect yourself against inflation? Take a fixed mortgage loan? Buy (farm) land?

(1) You could even argue that the recent Gamestop squeeze was caused in part by stimulus programs. Millions of people got some free money and they took it directly to Robinhood.

My bet is there aren’t many places for money to go while most of the world is under some kind of shut down, so inflation can’t reach the real economy as of yet. It may start rising when the people who have been saving, and were not used to, start to have more ways to spend it down again (these travels and holidays we’re postponing and are eager to start again).

Yeah, previous recessions were also unexpected. Inflation rise is usually also sudden and not expected. In fact, such comments en masse are sign of market euphoria that pushes valuations to unsustainable levels.

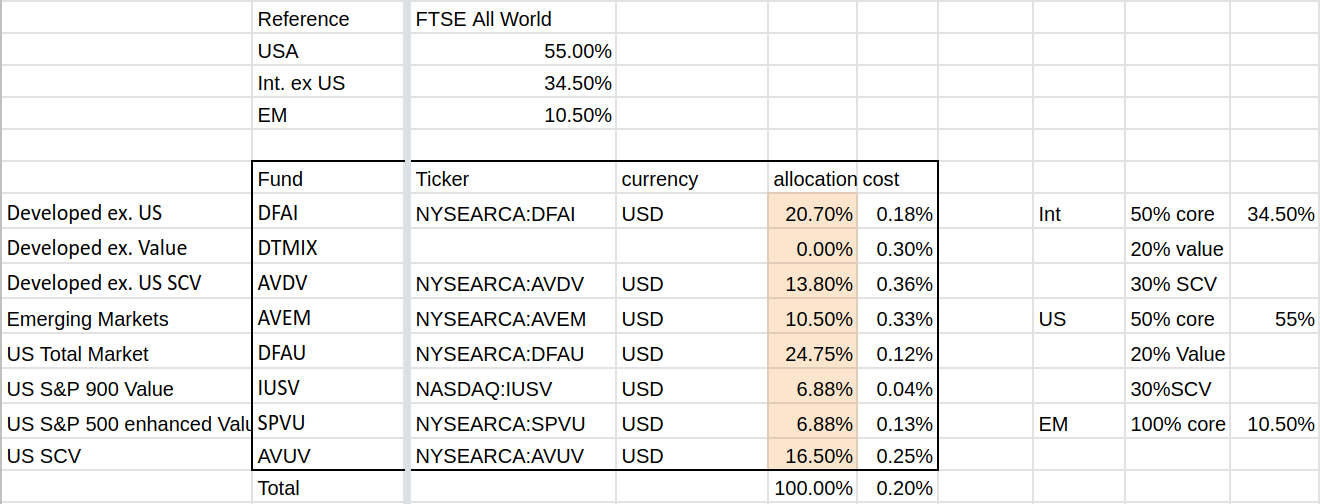

Here is my allocation. Dimensional will convert DTMIX to an etf this year, when that happens I will adjust the allocation a bit.

It is quite a strong tilt towards factors, but this doesn’t include my 3a funds. With that around 35% of my equities are in fund that specifically target factors.

This is a good point. All this liquidity providing by central banks fuelling stock market valuations is becoming the new normal since 2008 crash and euro-zone debt crisis. It might not burst for years. I remember I already was discussing this with friends at work and here at this forum 4 years ago and back than people were already saying it’s an almost 10 years bull market, valuations are super high, this stuff is unsustainable.

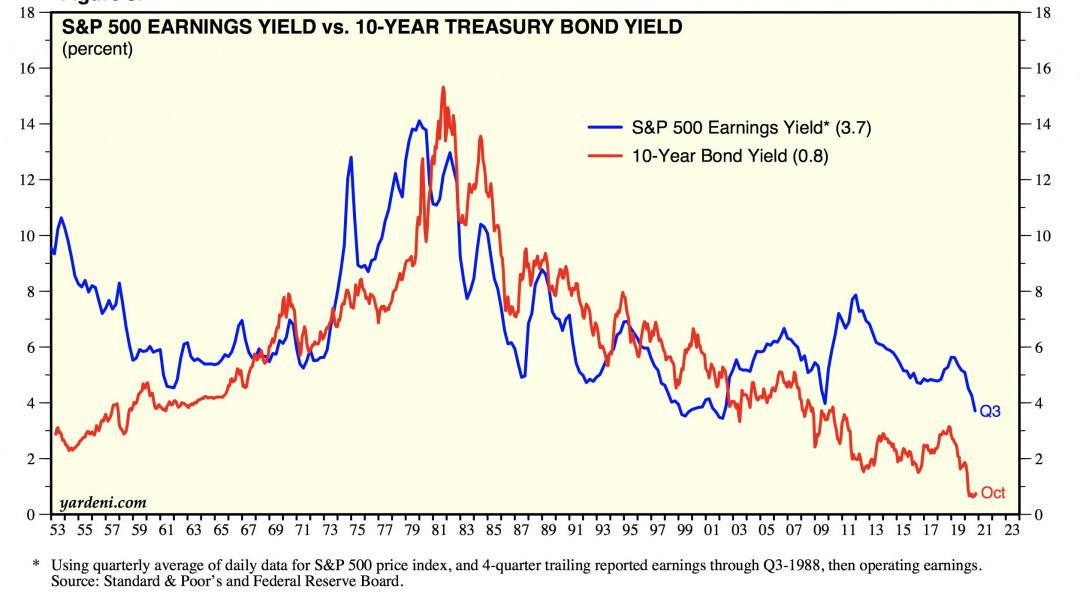

Cut the fearmongering :-). Markets follow the risk free rate of return. With US 10y treasury at ~1%, the S&P will match it at P/E=100 (1/100 = 1%). This is completely different from the 1995-2001 bubble when risky assets (stocks) yielded lower than safe assets (bonds). In reality we will probably not reach an aggregate P/E=100 on S&P500 level but there is plenty of room for valuation expansion.

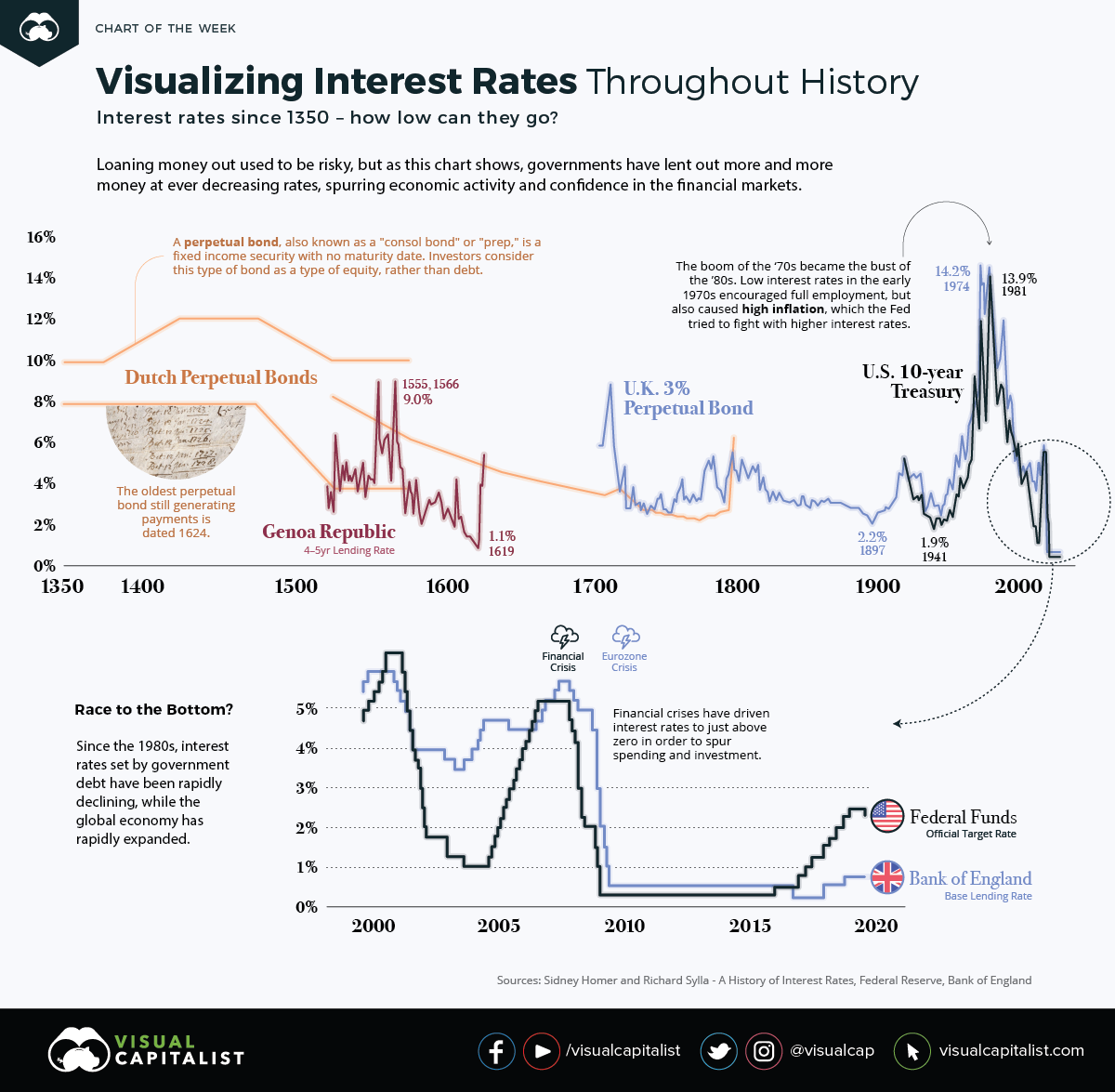

Everyone advocating an imminent return of high interest rates should probably look at Switzerland. We have the experience. It’s nearly impossible to escape ZIRP./NIRP and low rates are here to stay.

We may see 1.5%-2% on 10y bonds in some years from now, buf this still corresponds to P/E=50.

Really good point there. Low/negative return on fixed interest assets (cash, bonds, time deposits) pushes people to invest in things that still offer positive return. I guess in Switzerland there is no “risk free rate of return” anymore, maybe a “risk free rate of loss”. You want to “invest” capital without risk - not possible.

So the people whose money is locked into “low risk” assets (pension funds) are simply losing money. If you look at pension funds, on one hand the demographics are bad (more old retired people, fewer young working people) and then pension fund returns suck, because they need to invest in bonds. I wonder how high will pensions in 2050 be…

What would you say to a claim that zero interest rates rob people with conservative asset allocation off their savings?

Regarding the return of interest rates to the average, that would be a real black swan event. I can imagine the policy makers would be forced to do it during hyperinflation.

I’m not going to try and predict what will happen in some years from now. The situation we have now is barely an evidence to why the markets keep on going up and will probably continue for as long as risky assets yield more in time adjusted basis than safe assets.

In other words, time to worry is once 1/(P/E) < long term treasury yield

Interesting link, but also useful to read the comments.

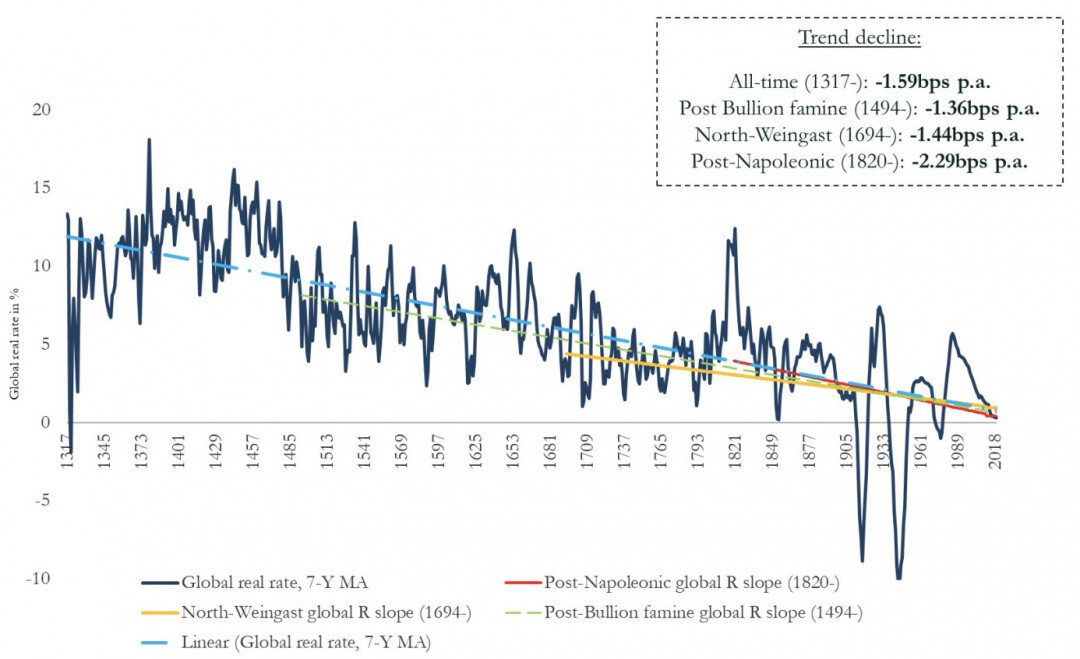

OK, I guess it makes sense that the interest rate is not an average, but that it has been dropping. The average lifespan, age, stability of law and enforcement contribute to lower lending rate. The safer it is to lend money, the lower the rate. And of course the World is much more organised than a few hundred years ago.

Still, the interest rate has had big volatility around the trend line, and a diversion from the trend may exist for decades. So I may correct my statement and say: the interest rate might not converge to the average, but to the trend line, or may make an upswing.

So, in order to reduce the risk the interest rate has on my portfolio, would it make sense for me to buy a flat with a 10y+ fixed rate mortgage? Or is it better to keep all the money in VT?

The ECB has purchased corporate bonds in the value of 255 billion EUR. This lowers the cost of debt for private companies. They save money on interest.

By reading and partipating to this forum, you confirm you have read and agree with the disclaimer presented on http://www.mustachianpost.com/

En lisant et participant à ce forum, tu confirmes avoir lu et être d'accord avec l'avis de dégagement de responsabilité présenté sur http://www.mustachianpost.com/fr/

Durch das Lesen und die Teilnahme an diesem Forum bestätigst du, dass du den auf http://www.mustachianpost.com/de/ dargestellten Haftungsausschluss gelesen hast und damit einverstanden bist.