I have to be honest that I looked into some of the real estate funds couple of years back and I was disheartened by the fact that their trading price was much higher than their reported NAV. I was looking into it as I look at Stock Funds where trading price and NAV are very close. So I thought Swiss people are overpaying for these funds just to have real estate exposure.

Now that I read your comments, it seems like that comparison of Fund price vs NAV price is not a right thing to do. And I was completely wrong in my assumptions.

So just to be sure if I get it. The difference in Fund price vs NAV is similar to the difference of buying an apartment in Zurich and reporting same apartment in the tax return. They might not match because tax value is always lower. Right?

Fund recommendations

You also recommended people should have 10-15% exposure to such funds. Do you know which ones are the cheapest option vs UBS? Or UBS is already the best when compared like to like?

Last question

TER of these funds should be compared to cost of managing a buy to let property? Or the cost of managing the property is inside the fund and TER is only about managing the fund itself….

To explain, when someone owns a property, they spend money on hiring an agency to manage it. There are also costs of maintenance etc. Are such costs part of TER?

By the way. You original question was focussed on UBS direct fund vs Buy to let (with mortgage)

But in principle , UBS fund is also buying to let (with mortgage) as this thread confirms. They just do it a bit better due to scale.

However UBS also have an article saying that buy to let is not very attractive in current interest environment. So I am wondering if individual buy to let is not attractive then why collective buy to let (via UBS) would be attractive ?

In principle, both are buy-to-let. I totally agree. Therefore if buy-to-let, as a broad term, is not attractive, then both are not attractive.

But for me, buy-to-let, as a broad term, is attractive. What I am comparing is on a more on detailed level, under the same broad term, buy-to-let. One choice costs more time than the other. Once choice has less leverage than the other. One choice is more liquid than the other. One choice has more return than the other, or not?

not to hijack your interests, but if buy-to-let is not attractive, why don’t you consider 5-6% (CHF) financing in crowd-financing rather than the 2.2% yield + Fund risk?

I’m also trying to allocate my next chunk of money somewhere.

As the SNB is lowering rates, the RE market should get another boom (lot of FOMO on the last 2 years + slowly cheaper financing options + constant influx of people) - how would I capture this if I’m not willing to drop multiple 100k’s in one basket otherwise?

My only option for small-ticket purchasing seems Crowdhouse, but I’m not quite confident with the company anymore.

Crowdfinancing seems attractive at around 6% yield (also no tax impact if I’m not mistaken), but it’s not owning anything long-term, the deals expire in 18-24 months.

This UBS thing doesn’t look bad after all, as it’s so easy - did anyone make a graph yet with “swiss property index vs UBS Direct fund”? Could be a nice hedge as we also rent our place.

Hmm, I guess you didn’t read the sentence directly after that sentence you quoted?

Anyway, I have never seriously considered crowd financing yet. I don’t know how to compare two buildings as an investment object. It is just out of my affordable range. And therefore, I don’t know how to make a decision on crowdhousing that I want to go for this project.

I think crowdfinancing (assuming lending option) is more comparable to high yield bonds. The main return comes from ability to take risk of credit default. The returns are not about the real estate market. I see it more like betting on real estate company rather than real estate market

UBS direct is more comparable to buy-to-let.

Regarding comparison with real estate market, one to one comparison is difficult due to leverage involved.

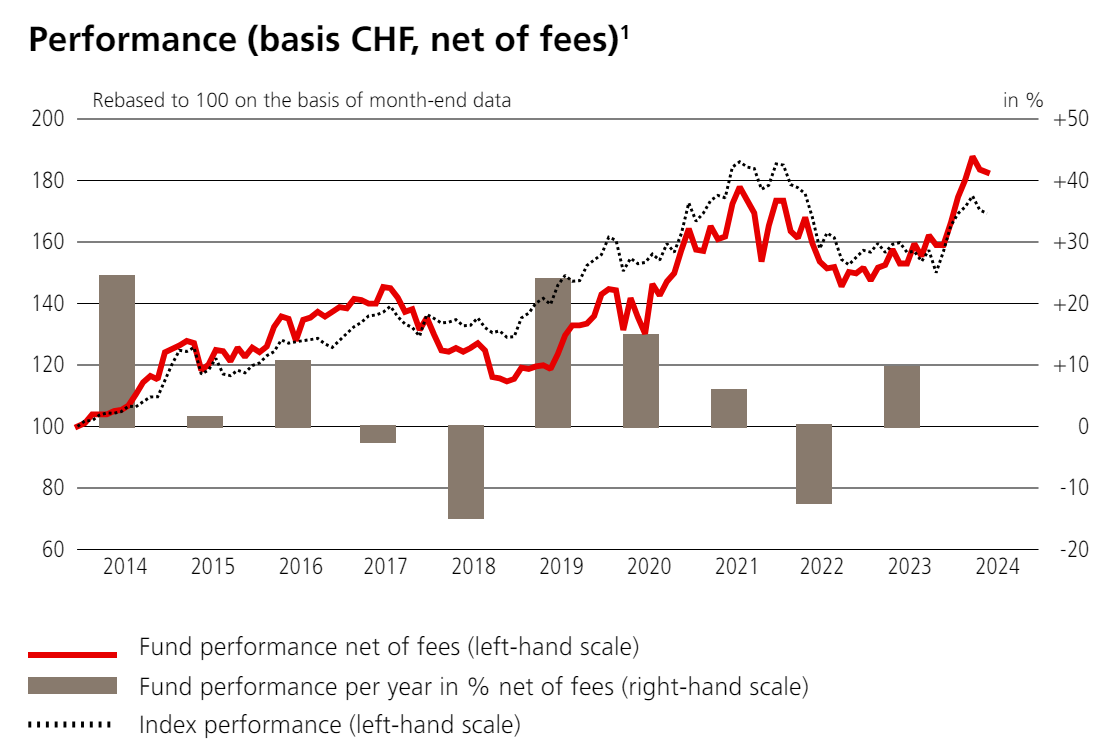

If you refer to factsheet, you will see overall returns of this UBS fund are about 57% in last 5 years.

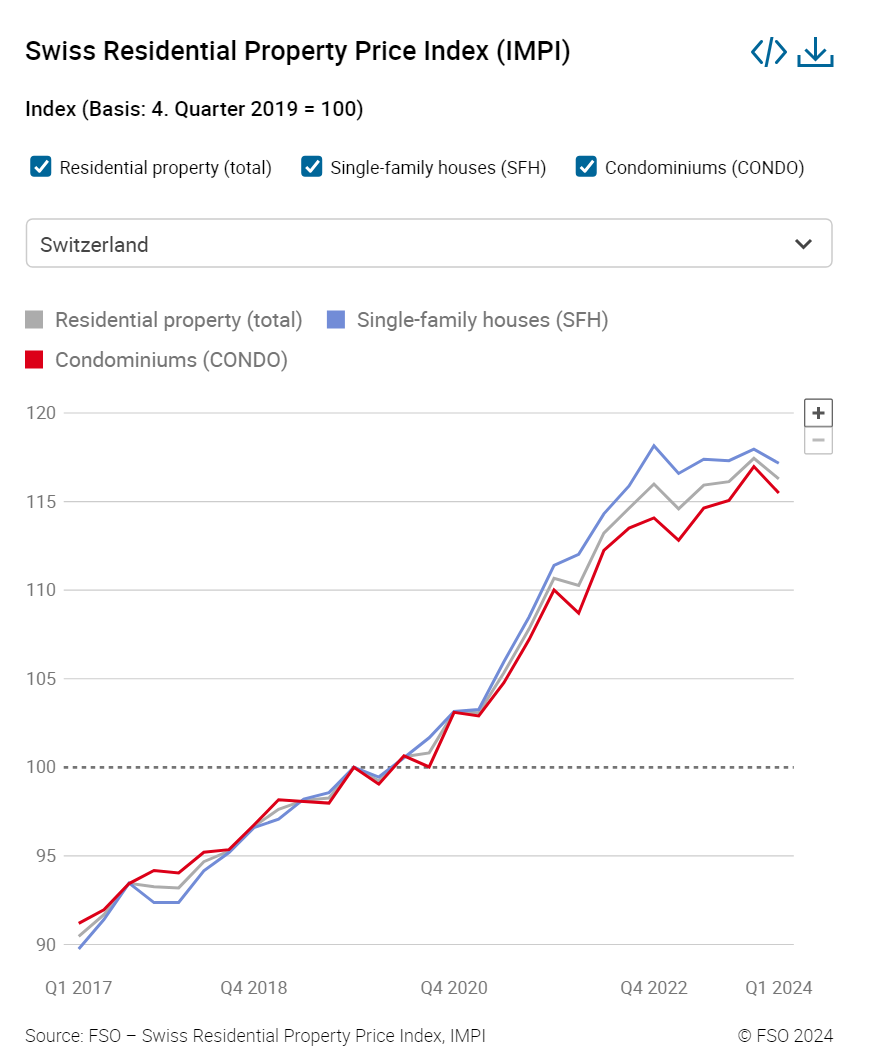

The real estate index of Canton of Zurich is up 25% and city of Zurich is up 30% in 5 years. But this is the price index. So you need to add rental yield on top.Price trend

the dotted line “index” on the latter looks very different. The real property price index almost never had a down leg in the last 7 years.

If you compare the 2 charts, the Fund started off with 3 years of zero wins, while the RE market went 13% up… ? I’m just a tad skeptical on how to get closer to the 1st chart without direct ownership.

I think the benchmark index in UBS factsheet is not the property index. It’s the index of real estate funds.

So as usual in bad market conditions, the notional value of real estate drops, this means people holding the funds start selling in panic mode. This doesn’t actually mean that funds started selling their assets (underlying units).

Most likely the drop in Real estate fund prices reflect the drop in premium over NAV. And the Swiss property index is showing the actual transactional prices which never dropped meaningfully.

I think the real estate funds will follow Swiss property price trend in longer term (maybe 10 year horizons) but not in short term (quarterly or yearly numbers). But again, please remember there is a leverage here , so the impact on upside and downside is multiplied.

For UBS fund specific- you also need to keep in mind it’s only investing in German speaking areas.

Also the SNB data is overall real estate (incl. SFH), the fund will own mostly apartments, and often will be limited to specific region (e.g. urban area in german speaking switzerland).

What happened between 2017 and 2018/19? Nothing on the market that would’ve generated a panic. The SP500 was going up nicely until the 2nd half of 2018 - maybe everyone was FOMOing into stocks instead? You need to buy when it’s cheap (at least under its own index).

It could be a chance now to be contrarian - drop the stock market and pile into RE before blood flows on Wall St. I guess a lot of people already started that at the end of 2023, hence the bump up in the fund’s price.

I don’t know about 2017-2019 but I remember when SNB pushed rates up in 2H of 2022, the SIC (which is Swisscanto fund) went down quite sharply (approx 25%). Most likely people assumed that increase in interest rates would lead to price fall. But it didn’t really happen so price went up again.

Interesting discussion. I gather from your comments that returns and volatility would not make this a particularly appealing instrument in a ‘normal’ portfolio, but what about as a tool to compensate for a short position on RE (as oslasho was mentioning above)? I rent and not looking to buy anytime soon, would it make sense for me to own something like this at a 10-20% of total portfolio (comparable to an ideal primary RE allocation)?

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.