But there is a bigger than 50% chance that the fund will underperform the SPI in the future.

That there is an incentive to outperform the index doesn’t make it easier for the fund manager to outperform the market.

Banks keep good performing funds and close bad performing funds. But funds that outperformed in the past are not more likely to outperform in the future. There is plenty of research to show that.

By the way did anyone look at how it outperformed? From what I can see it’s currently short financials (no UBS/CS holdings) compared to SPI and indeed financials have underperformed in the past 10y.

Then the question is how did they justify that choice and if it’s just luck.

I rally like this perspective. the 1% basic fee is less than basically any product from a big bank in CH (CS, UBS, …), so I do believe it is a true incevntive for them.

Do you know about any other fund doing something like this?

I rally like this perspective. the 1% basic fee is less than basically any product from a big bank in CH (CS, UBS, …), so I do believe it is a true incevntive for them.

Do you know about any other fund doing something like this?

Good question. I personally have no clue.

I guess that they doi not justify, but provide just final good results and people are happy with them.

To be short is somehow part of the game (130 long, 30 short), so this doesn’t bother me too much.

Honestly I do not think they will tell you how they pick which ones to long and which ones to short. At the end this is where is the value of the fund manager

Honestly there is bunch of documents with all the details. I did not read them yet, but definitely on the to do list for the coming days.

Most funds do provide some pseudo justification / newsletter. By the way by short I do not mean shorting the stock, I mean being short compared to the index (iirc UBS is like 3%+ of SPI, but they don’t hold it, I just skimmed their top holding compared to SPI).

For what is my understanding of this fund, they are not copying the SPI in term of % of capital allocation, but they are rather investing in all companies present in the SPI, but with variable allocation (with the 130/30 strategy in mind) having the goal of maximizing returns. Please correct me if I am wrong.

Yes. ETFs are eating their market, so if they want to be still alive they need to get closer.

I did not know that there was a result-proprortional fee in other funds. Perhaps my ignorance, but I have never saw it in any of the fund provided by all swiss bank (I checked CS, UBS, Migros, Cler, Valiant, Cantonal Banks from many cantons, Reiuffeisen). Pelase correct me if I am worong

Yes that’s correct, so to explain the outperformance it’s interesting to see how the allocation differs from SPI (since that’s both the investable universe and the benchmark). And when looking at it it seems the biggest financial is that they don’t invest in financials as much. The rest of the allocation is the usual suspects for CH (Nestle, Roche, etc.)

It’s more common for hedge funds. Hedge funds are rarely marketed to retail investors from what I can tell. (I guess technically that CS fund is a hedge fund since they have leverage + short)

Create 100 funds. Market the one with the best tracking record the most. Attract new money. Underperform the market with this fund. Close the fund after a couple of years. Repeat.

Hello Cortana,

I would definitely agree with you…if numbers would say the same!!!

Here what they did is the following:

-patent application in the early 2000

-created the fund in 2004

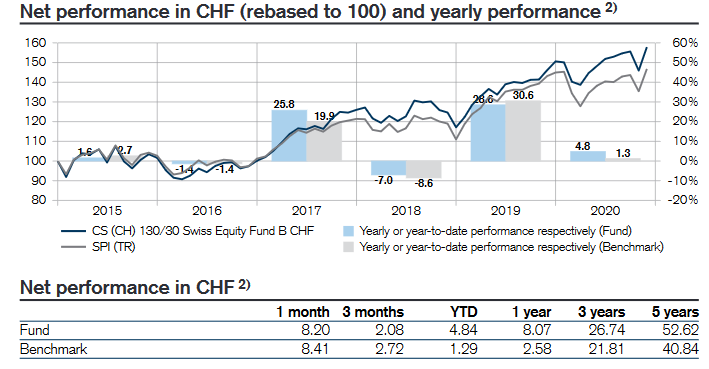

-basically perform as good as the SPI in net terms (this means that overally the were performing around 1% of the SPI) from 2004 till 2012

-beat the SPI from 2012 till 2020 around 2-2.5% per year (average return of SPI was around 5%, the fund provided something above 7% in net term, so something ranging from 8% to 9% in overall term).

According to what you said, it should be complitely the opposite, so performing well in the very beginning and underperform afterwards to eat people’s money.

It is maybe not that common path for an actively managed fund…but number are number! We cannot discuss them, we can just try to interpret what we see…

It can be definitely true. I’m just trying to analyse critically (pro and cos) the various option on the market. Any additional comment is definitely very welcome

You have a very good point here. There is deinitely a lot to learn on looking at their movements.

In the past years the CH financial sector did not do very well (banck secret lost…) so it makes esne in my opinion that they did not invest there.

On the other hand, CS is maitaining so many index about the Swiss economy (they speak everyday in all new about one million index on one miullion different topics either from CS or UBS), so I guess they can predict it fairly well. Agree guys?

I do not know how to define it. It is true that you have 160% (max, normally is lower) exposition to market. But it is also true that it is not only leveraging an index, like could be the TQQQ. What it is doing is to me closer to an hedge fund. I’m not an expert at all…

Any one that could help with the classification?

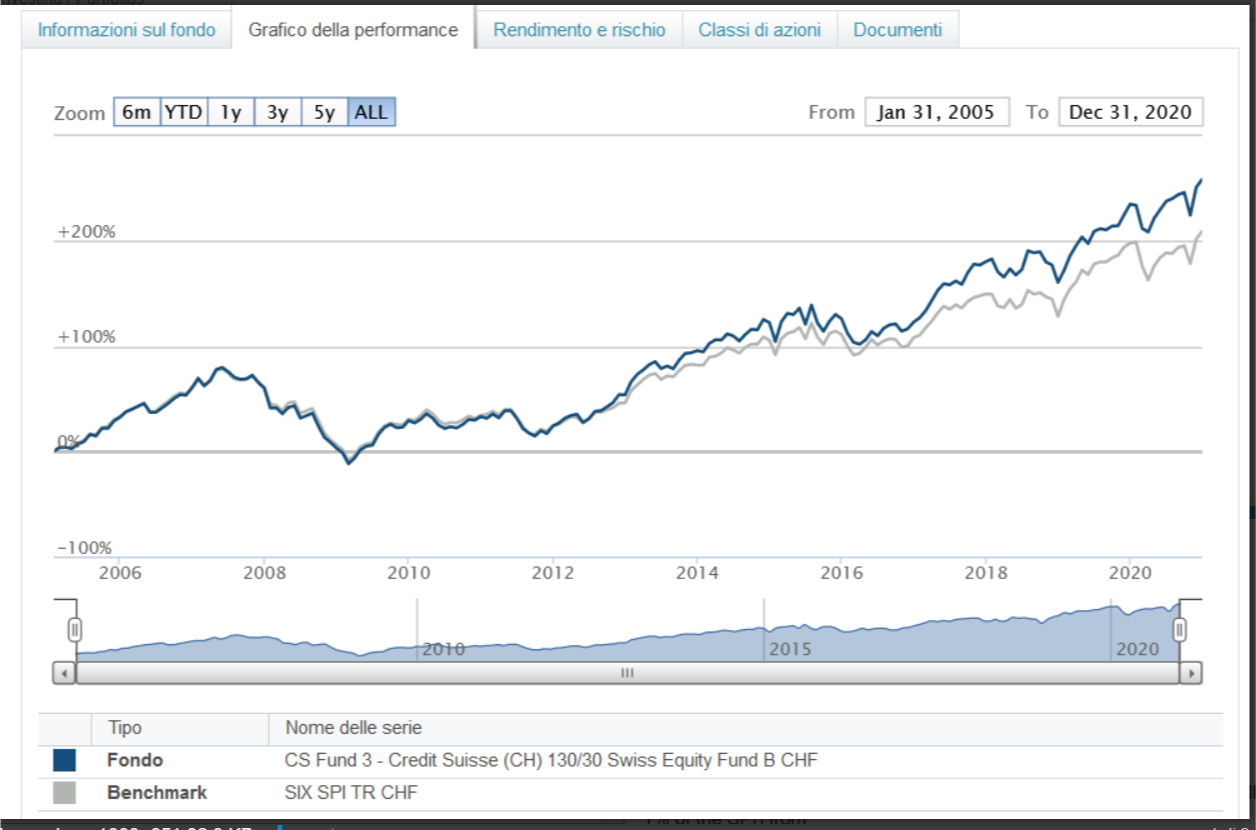

Oh no, don’t be misguided, that chart you are copying is most probably not net of fees.

Is there anywhere info which states the opposite?

Performance of the fund itself might be better than SPI, but you should be interested in the performance of you as the fund investor in there.

Plus it still doesn’t disprove the survivorship bias that Cortana was talking about.

This is the one which managed to not underperform the market (before fees) over the selected period of time.

And of course they would be putting it up front.

You are right by the above printed graph. I could not find if it was related to the net or gross performances.

But, I went in the fact sheet and took that one, in which is clearly mentioned that is net performance. Unfortunately it is povided only for the latest 6 years.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.