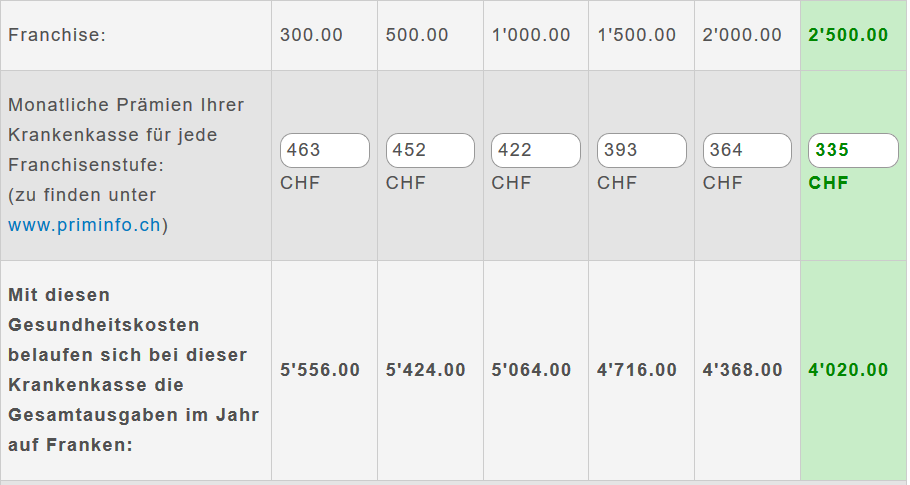

Lol, I give you a chart from Assura which clearly proves that 1000, 1500 and 2000 are useless and you just say that “people like to have a choice”…

Yes, look at the right end of the curves, it flats out. For example, by medical bills of 10’000, you will pay 500 deductible + 12 * 400 premiums + 700 coinsurance = 6000.

In fact, since these lines are so evenly distributed, I added a few more lines to reach deductible of 5000, and I got 150 monthly premium, so it was a sweet shot @ma0

I’m not sure free market would work. People already go to the doctor for every small thing… Let’s imagine a 5 chf per hour doctor that tells them they have nothing. Do they accept it? Nope they will never trust such a cheap doctor. In health stuff people wants all the most expensive options because pricer =better.

What I find interesting is that Comparis states it clearly:

franchise: 2500 if you expect your expenses to be under 2000 CHF/year

franchise: 300 if you expect your expenses to be over 2000 CHF/year

I go with the cheapest option unless I have “a doctor year” for which I go with the lowest franchise (and Assurance de base) and have all needed (planned) consultations scheduled starting from beginning of January (and yes, scheduling has to be done much in advance to get the first appointment, the following appointments and the treatment done in a single calendar year

2018 was my “doctor year”, and I learned a lot about which medication (as an example: dafalgan = yes, aspirin = no) is reimbursed with LAMAL. Do you have any experience with “Assurance de Base” and different providers? I assumed they are all the same (aside from paying for stuff from your own money and being reimbursed vs. having it covered), so I still went for Assura in my “doctor year” but I am not sure if by chance there is no some hidden profits with other providers of LAMAL.

There is also a tax discount benefit to consider, right?

Can you deduct from your income all expenses (franchise, 10% and non-reimbursable medication, also abroad)?

Do you have any experience with deducting foreign medical costs?

I don’t know wether I’m missing something but I think this advice is not sound.

I think they only calculate the tipping point of where you pay less and don`t take into account how much you pay less.

In turn this advice is only true if you either know that your expenses will certainly be above (e.g. if you have some chronic ilness) or below 2000CHF/year (e.g. if you never see a doctor out of principle). Most people are probably in a situation where they put some probability of their expenses being below AND some probability of their expenses being above 2000CHF/year.

So, I would pay 1530CHF more with the minimum franchise compared to the maximum.

For the expected expenses of:

(approx.)

500CHF, I`d pay 1340CHF more

1000CHF, I`d pay 1000CHF more

1500CHF, I`d pay 450CHF more

2500CHF, I`d pay 450CHF less

3500CHF, I`d pay 450CHF less

4500CHF, I`d pay 450CHF less

7000CHF, I`d pay 450CHF less

So, they are right about the tipping point, but the spread is very different if you`re below 2000CHF than above.

So if I’m right and you’re expected expense value is 2200CHF and you had a nice bell curve around that number, you should probably still go with the maximum premium.

I’m not sure where the actual tipping point of total expected expenses is but it depends a lot on the probability distribution of your expenses and not simply on the expected value.

I hope it won’t keep continuing going up like this.

I’m somewhat lucky right now, I switched to the cheapest insurance I could find for 2019 and pay only 140.- (because I am below 25, after that I gets ~100.- expensiver).

The biggest health insurer Helsana said that their costs actually went down for 2018, my hope is that this trend continues / stabilises.

But maybe we do have to busget for 700.- / month in 20 years time, what do you guys think?

I don’t think this is true. The amount a doctor or a hospital charges is decided in the TARMED in the frame of the LAMAL. Hospitals have an additional layer : the “forfaits” which specify how much is reimbursed for an act, e.g. appendicitis, regardless of the number of nights and extra care someone will spend.

Yeah there is the TARMED, which means there is no market economy. Good doctor, bad doctor? Zurich or some village? The price is always the same. So good doctors have full schedules and bad doctors just go out of business, I guess.

Also, the doctors will try to put everything possible from the TARMED in your bill. Did the doctor mention that you can go to his friend to make that next procedure and give you his visit card? That’s gonna be 30 CHF.

And you only find out what they put after a month or two, when you no longer remember how the visit went down.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.