I found another analysis “ETFs or futures?” by Invesco with data as at 31 December 2020 (there where also older versions). What knowing the right search term (“ETF vs Futures”) does for finding stuff…

They have analyzed following indices from 2012 to 2020:

S&P 500

FTSE 100

MSCI World

MSCI Europe

STOXX Europe 600

Euro STOXX 50

MSCI Emerging Markets

In comparison to the paper provided by CME Group (which operates financial derivatives exchanges), the futures cost in the analysis by Invesco (which manages ETfs) is higher, but much more in line with my own calculations.

Their actual comparison to ETFs is of course apples to oranges, too. In their dedicated section about how they compare ETFs and futures (page 12) they discuss their method. They calculate on the basis of a fully funded investor (so leverage = 1x). Under this conditions Futures still pay the risk mark up on the risk free rate, but ETFs don’t, since no money is actually borrowed (= your borrow money to buy ETFs, but your lender is yourself).

Going short on a futures contract and hedging it by going long on the underlying is apparently risky. So you want something in addition to the risk free rate and dividends.

This results in the observed risk markup required by the marked for buying long futures.

But curiously the spread around the price of S&P 500 futures is nearly zero.

Why does the market not consider it risky to do the opposite: Going long and hedging it by shorting the underlying? If anything this siphons additional security borrowing fees that should be compensated.

So where is this spread? Is it that the market is so liquid from the long side that this second strategy can not appear? In other words, everyone and their mom wants to be long S&P500 and the arbitrageurs oblige for a risk markup?

I just wanted to revisit this, as I have heard rumors about ways around this for a while.

Apparently, you can have US government bonds (which do pay interest) as collateral for futures instead of cash. Although, the interface still shows a debit and credit in cash. That means instead of:

Type

Product

Allocation

Rates

Interest

Stocks

VWRL

90%

US Gov Bond

SHY

10%

4%

0.40%

US Cash

USD

-5%

5%

-0.25%

US Cash

USD

5%

0%

0.00%

Index Futures

ES (notional)

100%

TOTAL

0.15%

You will get:

Type

Product

Allocation

Rates

Interest

Stocks

VWRL

90%

US Gov Bond

T-Bills

10%

4%

0.40%

US Cash

USD

-5%

0%

0.00%

US Cash

USD

5%

0%

0.00%

Index Futures

ES (notional)

100%

TOTAL

0.40%

This information is rather hard to come by. IBKR doesn’t mention it anywhere. Their customer support doesn’t know about it. The internet search engines didn’t find me any such information until recently.

Still, I have seen multiple people claim it works for them. I have now found a public claim through Reddit, which first links to yet another Reddit post, finally arriving on ET. Also, another such claim for those with an account on RR.

Futures vs ETF: there are rollover costs, I suppose they are included in the comparison.

I think today’s markets allow arbitrage trades for both and even for the underlying stocks. So the difference may get lower and lower.

A few words about withholding tax on “in lieu of” dividends: the tax is deducted on U.S. shares. It is not deducted on shares of many other countries. If you ask those back in your tax declaration in theory you commit a “cum-ex” fraud.

Unfortunately the internet tax form in Kanton Zurich has no way of declaring partial “in lieu of” dividends. That happens often, the broker does not lend out all of your shares. I usually state it in the comments of the tax declaration in such cases.

I think that is not a small problem for our taxmen. Interactive Brokers does declare everything correctly but I don’t think that all banks and broker do. In Germany alone they discovered billions in cum-ex damage.

If a broker does not declare the partial stock borrowing and charges withholding tax which you ask back, the cum-ex is committed by the broker and you as client cannot do anything about it.

Yes, every day the futures price inches closer to spot/index of the underlying, reaching it on maturity. The difference (plus movment of the underlying) is paid each day between holders of short and long futures.

Do you have some more sources? We have a personal account for IE funds. No WHT (especially no US WHT), but IE also doesn’t have their own L2WT.

In the statement I see WHT on “in lieu of” dividends for U.S. stocks, but not for other countries. I think last time I had partial in lieu dividends was in 2022, let me check…

…found it, was 2022. I had a stock from Argentina, Italy, Luxembourg, Greece, Israel, Netherlands (No WHT), Uruguay (No WHT), Bermuda (No WHT), GB (No WHT) and the Caymans, what a year.

No WHT for the lent out part and WHT for the part that was not lent out in the countries that charge WHT. All the U.S. Stocks that were lent out had WHT deducted, in lieu of or not. In the Zurich internet tax declaration there is no way to declare this situation correctly, had to mention it in the comments.

I looked in “Account management”, “statements”, “Tax”, “2022” “dividend report” to find the relevant information at IBKR.

I think Switzerland has a little problem here. IB does not cheat, but the taxman cannot control the Swiss banks or broker because of the banking secret, therefore it is very easy for them to cheat. I have never seen “in lieu of” dividends in any Swiss broker statement. The fact that in Germany they discovered billions in cum-ex fraud makes me think that in Switzerland there may be some too.

I want to share a success story. Today, I rolled my FMWO futures (MSCI World, Net, USD, on Eurex) with IBKR’s TWS.

I needed some time to become confident that I would not mess it up, but in the end it was very simple. I just bought a calendar spread, which nullified my old futures position and gave me the next 3 month one.

The really cool thing is the price for this calendar spread nearly doesn’t move. It is can be understood as depending on three rather static factors: The risk free rate, the expected dividends lost between Gross and Net, and the markup for leverage.

The index was around 13400 USD. Bid and ask were 137 and 144 respectively. In the end I just bought the ask with a limit order. My calculated fair price was 122, taking in account the risk free rate, and an approximation of the lost dividends (Gross - Net) based on historical annual monthly patterns and dividend levels at the moment. This leaves me with around 16.5 bp markup for the next quarter. If that will be similar in the future, it would be around 60 bp annually.

But since the theoretical price is quite stable, I might just put in the calendar spread early next time and let it sit. Because if I got the bid price, it would be only 11 bp. Maybe even less, since the actual price of trades made vary quite a bit over the months it is active.

But I see prices near 0, which would be a cost of about -90bp (so nearly 1% in my favor per quarter). Which is strange (very strange). If someone knows more, I’d be happy to hear it.

Yeah, you could, or you could earlier. I now hold a futures contract that matures in 3.5 months instead of holding the old one a bit longer and then getting the same new one with only 3 months till maturity.

Rolls can trade all over the place. It’s like a separate market. Especially in times of market dislocation where banks funding requirements change, e.g. their index arb book might prefer being long futures, shorts stocks to have more $$. This is most likely not modeled. A roll is NOT a nice steady risk free trade.

One more thing, TLDR, how are dividend expectations vs actual dividends modeled. A future trades based on expected dividends. If you’re long a future, you’re basically short dividend increases. Same goes for interest rate curves, if they suddenly change, futures prices will change.

So you claim that I can realistically get those -1% markups per quarter? That would be a goldmine. As such, it can’t be true.

Can you expand? Even if the prices would be wild in reality, after my trade I only held Dec19 contracts. I’m not leveraging the roll to the moon. I add about 0.3x leverage through the notional of a contract.

The fair price of that roll is rather static. I want to place a limit order for a price as low as possible.

Interest rates (increase price): 3-month interest rates don’t move that quickly. I’m exposed to about 1/4 of the change to the annualized rate.

Dividends (decrease price): The difference between Gross and Net is smaller still. In the dividend rich summer contract it is about 20bp on average. If they then unexpectedly double their dividends, the futures price goes down by that (since new expected Gross - Net dividends are 40bp).

Then there is some higher order difference in the overlapping interval of the contract I sell and the one I buy. I assume (but haven’t checked with data) it should be small, since we are still having the only difference is that one contract runs 3 months longer, and those 3 months are accounted for in the 2 items above.

Lastly, the changes in markup don’t bother me, less is always good.

How much can the fair price really move down in one day (resulting in a fill that is much above fair price plus acceptable markup)? Blips from market panic don’t really count. I would like to have my order filled at a lower price if it moves right up again afterwards.

It is not modeled. I would need much more data and time to produce historical distributions of the reaction to changes in expectation. I would probably need historical yield curves of the futures. Then I could make something from the yield curve estimate of intervals and how they actually did till maturity. This would be somewhat polluted by risk markup for further out intervals. I could additionally try to factor this into its components (interest, dividends, markups). Whereof interest would be easy (I just take the treasury yield curves) and the rest (dividends vs markups) probably pretty hard.

But maybe the points above might be an estimation?

Huh? I did not claim a markup is available. The difference between spot and futures price is determined by interest rate curves, time to expiry, dividend expectations and borrow rates.

That would give you the estimate of the fair value. And then futures (as well as rolls) can and do trade around this fair price. Everyone has a different fair value though as Bank A funding cost, dividend estimates etc differs from Bank B’s.And it times of crisis,deviations from fair value can be large.

As you rightly pointed out, this cannot be modeled with data available to retail investors.

Fyi I traded futures, rolls etc in a professional setting for more than a decade

I mean, I can calculate an approximate fair price from the expectations for a point in time. No advanced predictions of future price distributions needed. That fair price doesn’t vary as much as the screenshot above.

If those were real trades that I could be any side of, I would get approximately that negative markup (~0.9%) for rolling at a price of 0 some days ago. So the question is, what am I looking at?

It’s wolves of Wall Street over here. Fascinating.

Long gone “I’ll teach you how to create an IBKR account, what a stock is, what an ETF is, what dca is, and why it makes sense and how to invest low-cost world stock ETF forever”

I’ll add: “but remember that you’re at level 0 of understanding markets at this point”

Now that we’re expert with futures, teach us STA spread trading in another thread

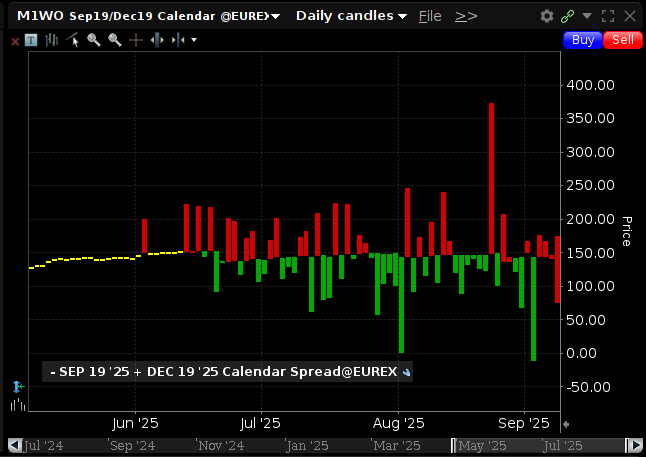

Ok, if anyone finds this in the future. I put in a limit order and the candles moved below it. I also got EUREX L2 data and found that my limit order actually was on that a calendar spread book (according to IBKR’s TWS).

From this and some more comparing of numbers I conclude:

The chart shows synthetic “price” as the difference between the prices of both outright contracts. In a time interval all trades have their price computed with the last available price of the other contract. If there is more than one synthetic price, there is a candle (highest - lowest).

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.