This is my first post I ramble a bit, so I hope everything is clear.

My girlfriend works at a large swiss company, that offers 20% discount on various insurance products. We got an offer for 3a with a monthly payment of CHF 500. The fees are quite high (CHF 19.90) and there is an insurance (“Prämienbefreiung bei Erwerbsunfähigkeit”, CHF 26.60) included. I am not sure how the fees are related to the total payment amount if that were to be increased. It is also possible to buy 3b (our adviser said the fees are the same and it can be withdrawn at any time). As far as I understood it is possible to buy up to 20k (3a+3b including payments to other 3a providers).

summary:

The company pays 20% of the monthly cost (not sure how fees are handled)

Maximum of 20k per year is possible (3a + 3b)

I did not consider investing the cash there. Mainly to keep the calculation simple.

The money would otherwise be invested at Viac or Degiro.

3a transfer within 5 years costs CHF 300 (not sure about 3b)

The fees would be payed by the 20% discount, so about 11% are left over

There are so many unknown variables and my math is rusty, that I am unsure of my calculations.

I am not sure how the discount is taxed. Worst case the whole 20% is taxed as income.

How would you handle this situation? Under what conditions does it make sense to take advantage of the company discount?

Maybe it could make sense to invest the money at the company (probably active funds with higher TER). On the other hand the position could also be used to reduce risk, instead of leaving the money at the bank.

Thanks for all your inputs and please tell me if you need more information or have any questions.

Here is my view: is it a 3a life/disability insurance ? Yes ? Don’t sign and open a VIAC, Frankly, Finpension (even PF 100) 3a account and invest the rest with whatever broker you want, you will earn more than de 20% discount on a product which offer between 1.75% and 3.25% return with a TER of at least 2%

It is quite the same, the insurance will take a portion of your investment to ensure you against a risk of disability.

Imagine that you invest each year for 30 years 7’000 CHF, where the 3 first years are invested against you to ensure your risk disability, we are talking about a loss of 21’000 CHF. Then from the 4th years, they invest for you 6’000 CHF, and they take 1’000 CHF to continue to ensure you against your risk disability, and this for 30 years.

At the end you will lose 51’000 CHF (21’000 + 30’000) and only invest 162’000 CHF (27 x 6’000). Now imagine that these kind of insurance give you 5% return, but you pay 2-3% of fees… Do you really want to lose all of this money ?

In comparison with Finpension or VIAC you will invest your 7’000 CHF for 30 years for 0.45% TER and a 7% return…

Just subscribe to a real life-disability insurance, and not with a 3a…

EDIT: This is my view about your question, you can ignore what I’ve said and go for it, at the end, it is your money, your investment and your choice Personaly, I will never take again this kind of product (I’ve lost 4’400 CHF, it was a bad choice and I’ve learned from it).

Just my personal opinion: As soon as I hear “3a” and “insurance” in the same sentence, I head for the nearest exit. I (as many others) have been burned before and I don’t intend to repeat my mistakes.

This is exactly why many people fall for the 3a-insurance trap: It is a huge blackbox and its fees are almost impossible to figure out. It might even be worth it with the 20% discount, but I doubt it. My advice: separate saving and insurance by opening a normal 3a account and getting the insurance you want/need (do you really need an insurance that pays 500 per month into your 3a in case of disability? In that case I’d rather have that money available to be able to alleviate my disability).

Another thing to consider: Be aware that you are signing a contract with a LONG duration. Usually, the contract ends when you turn 65, and until then, you are obliged to pay the premiums or face the consequences.

If you want to understand how this product works ask them to provide you with the table showing the surrender value of the 3A account (i.e. how much you can withdraw at any given time) and compare this to a standard compounding account with the same return as the one used from their simulation. At this point you will understand the difference between the two and how much money they make on your back.

I also got such an offer from swisslife and did not do that comparison until I discussed it with my wife as she was also considering getting one. When we did the calculation we understood that they took around 3% per year of fees on your money and that over the whole duration of the contract. That story actually lead me to that forum as I was googling about 3A insurance account and that’s when I found the horror stories people posted here. After the first payment I canceled the product, total loss for me 500 CHF but it could have been a lot bigger had I continued to send them my hard earned CHF (NB: I would actually say that 500 CHF to find that forum was actually not a loss given the information you can find here). Also one important thing, you ll see from the surrender value table that you only start making money after a few years (I would say at least 5 if not more) and that if you need to withdraw early e.g. to buy a property you will actually lose money.

I would also recommend to stay out of this and go for VIAC ^^.

3B is the same story, same kind of construct. What alternative do you have ? Just browse this forum there are plenty of ideas, for instance open an account with Interactive Brokers and invest regularly into Index ETFs.

… the point here is the 20% discount on every payment! You pay 500 CHF p.M. and the employer adds another 100 CHF - each month.

Subtracting costs and the insurance part, you still get a performance > 10% in every “first year”.

On the other hand, there are the opportunity costs of not having your (full 3a) capital invested at “best” performance during the following years (e.g. VIAC). The difference / discount, you can invest there, though (~1200 CHF p.a.)…

Without knowing the projected annual performance and TER (compared to e.g. VIAC) and the projected time span there is no way to calculate it through (even If you value the “insurance part” with 0 CHF)

In your place I’d: Sign up, take the 20% (> 10% resp.) in every “first year” and cancel the contract every few year… and move the capital to VIAC (given the cancellation fee is only 300 CHF)

500 CHF per month with 4% for 30 years is 345k.

400 CHF per month with 6% for 30 years is 392k.

We don’t know the exact cost structure, but insurance products are always pretty expensive, so 2% difference isn’t even that farfetched. What happens when she stops working there? Will she lose this bonus?

I would never mix up insurance with capital saving.

the fact that the money is not locked does not change the issue. If you were to withdraw that money in a few year after opening you will lose money. Again what I wrote in my post is still valid, ask them for the table showing how the surrender value of the life insurance evoluves over time and compare it with a normal investment account offering the same return as the one from their simulation. You will then see how much fees they charge you per year and I can tell you this is massive. The advisor will surely get a juicy commission if you sign I can tell you that ^^. Do you live in a canton that offers tax deduction for 3B premiums ? I would say that’s the only situation that could justify having one (would however need to understand whether the tax deductions make it up for the fees the insurance company charges in the 3B)

Ask for the table then you’ll see how the surrender value evolves. I would really be surprised if this really is your payments - insurance cost ^^. They usually stay at 0 for the first 2 years and start to slowly increase after that until they finally get in line with you payments after 5 to 10 years (i.e. 0 return for that period of time). Reason for this is that the insurance company needs to build up the reserves required to cover the risk associated with the contract. Ask for the surrender value table that’s the only way to judge whether this product makes any sense.

In Geneva, you can have a deduction on your tax if you invest 2’200 CHF per year. You can invest more, but the tax authority will take only the amount of 2’200 CHF. In Fribourg, it’s 1’000 CHF. And that’s it.

However, I think that it is still not a good investment.

I am in the same doubt, but didn’t go for the math yet.

In my case I work for one of them, so I get the 3rd pillar without fees, only paid the insurance part

now I want to extend it open the 3 pillar 3 more to be more tax efficient and I am not sure where to do it.

Oh, we do have a downloadable “factsheet” as well.

Sadly, they juicy details seem to be missing.

Like… in what are they going to invest, actually?

But let’s go back to the fancy simulation, shall we?

Suppose I’m 25 years old, can save 1000 CHF/month for the next 40 years.

And my investment strategy is going to be dynamic, cause boy, am I a risk-taker!

So what you are saying is that if you pay in 500 chf into the product you actually only pay 400 while your company pays 100 ? I did not understand that sorry I though the 20% discounts only applied to fees (my wife has such a deal with her company on the fees of 3A / 3B with some insurance company thus the confusion) you anyway need to get the surrender value table to understand the exact yield on your own 400 CHF and take into account the impact on taxes. As mentioned by others answering the question what happens in case of job change is also a key factor to take into account.

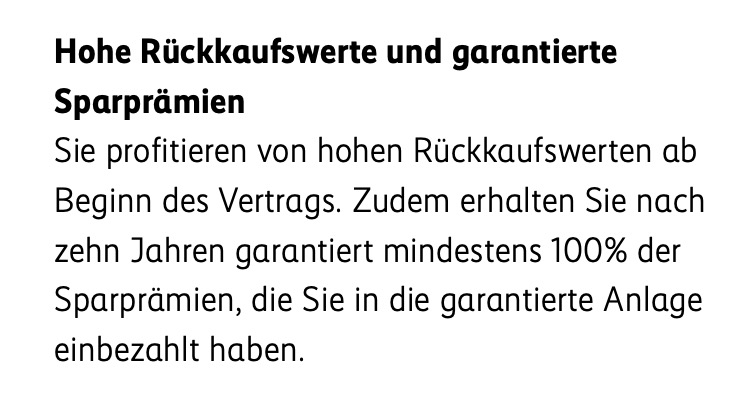

Not according to the product web site you linked above. See the PDF I already linked above, page 7 (emphasis mine):

"Hohe Rückkaufswerte und garantierte Sparprämien Sie profitieren von hohen Rückkaufswerten ab Beginn des Vertrags. Zudem erhalten Sie nach zehn Jahren garantiert mindestens 100% der Sparprämien, die Sie in die garantierte Anlage einbezahlt haben."

By reading and partipating to this forum, you confirm you have read and agree with the disclaimer presented on http://www.mustachianpost.com/

En lisant et participant à ce forum, tu confirmes avoir lu et être d'accord avec l'avis de dégagement de responsabilité présenté sur http://www.mustachianpost.com/fr/

Durch das Lesen und die Teilnahme an diesem Forum bestätigst du, dass du den auf http://www.mustachianpost.com/de/ dargestellten Haftungsausschluss gelesen hast und damit einverstanden bist.

I ramble a bit, so I hope everything is clear.

I ramble a bit, so I hope everything is clear.