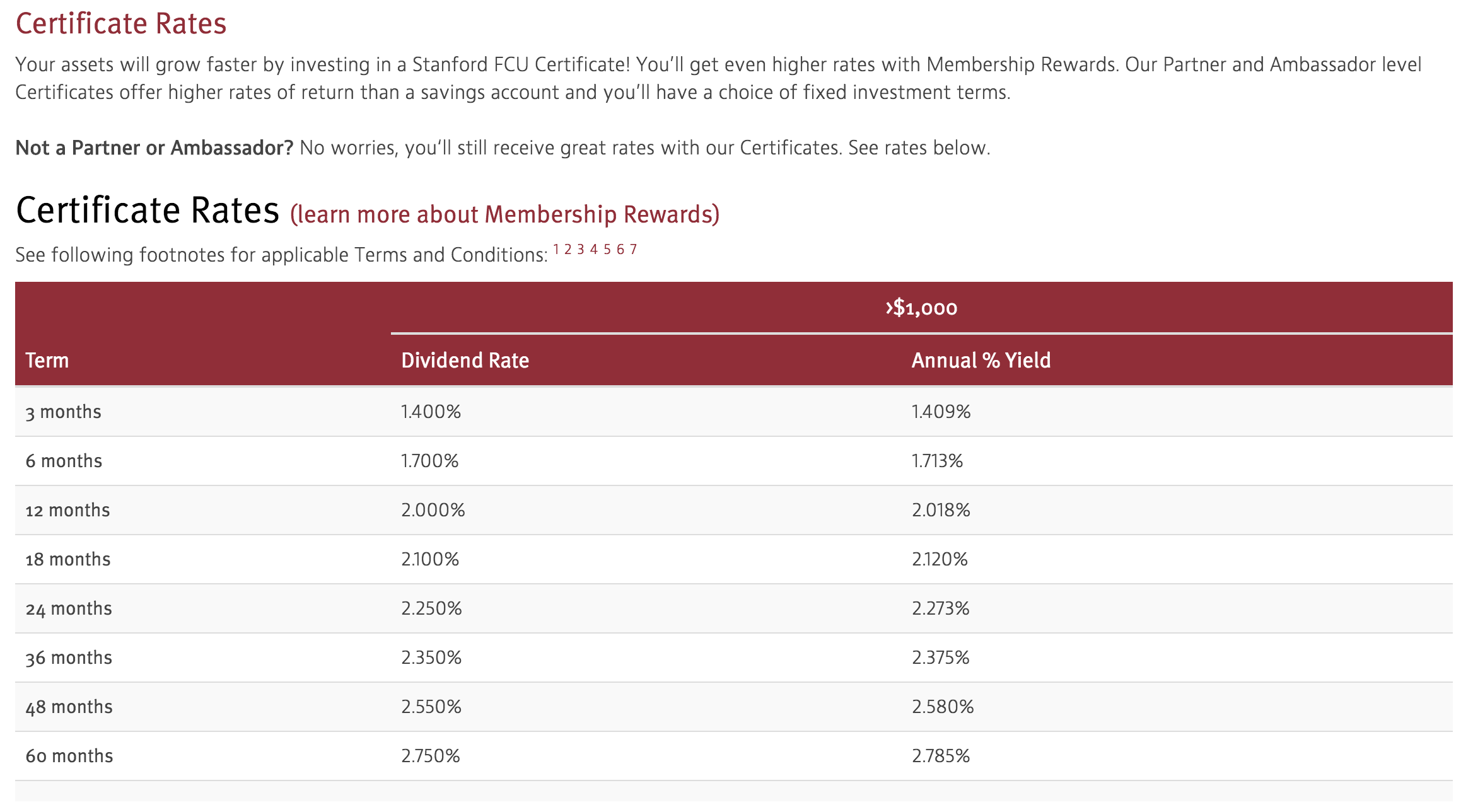

I’ve read about CDs (Certificates of Deposit), which seem to be common in the US: you deposit a given amount at your bank, and block it for a certain duration (e.g. 12 months). In return, the bank pays dividends to you.

Please take into account that 2% might sound nice at first glance, but consider the inflation you have in the US. You are not even beating inflation in the US, which currently sits at 2.8%

In Switzerland inflation is 0.6-0.8%, So you have the same situation, where CD’s / Kassenobligationen are just not worth it.

Thanks for your answer @Joey! I need to learn to focus on real (inflation-adjusted) returns instead of nominal returns.

As far as I understand, inflation affects you when you live in that country (goods are getting “more expensive” in nominal value). If we live in a low inflation country and get a fixed-income product like a CD in a high-inflation country, could there still be some real return?

Or will the difference in inflation be reflected in the relative prices of the two currencies?

It’s not about country, but about currency. So if you’re not spending the money in the currency of the product, then you bear the exchange rate risk, which in the long run tends to reflect inflation difference between the currencies, but in the short term there are other factors, which make the xrate change much more rapidly than inflation.

As far as I am aware yes. Inflation is basically measured by taking an average shopping basket of a countries products used by the people living there. So for instance you look at the price of milk, toilet paper and lots of other things basically.

However its only an average for the products consumed. Lets say milk spikes in price. You buy alot of milk I buy none. You have a much higher inflation than me, I am unaffected by this milk price increase

Its close to impossible to determine your personal inflation rate though, so that’s why averages are used.

I just checked the inflation rates of Germany and Greece and indeed they are different. So although they use the same currency, they have different inflation.

As @Joey said, measuring inflation is hard, and some people don’t trust the official measurements. The government has an incentive to lower the official inflation rate, because then they can sell bonds at a lower return.

If prices of beef go up and people switch to baloney, the statistics bureau can say: the preferences of people changed, so we adjusted the basket of goods.

monetary inflation (it’s depreciation of the currency by an increase in the money supply by central banks and thus loss of relative value vis-a-vis other currencies)

price inflation (it’s the CPI inflation - for instance, OPEC makes a deal and decrease the production of oil, then its price goes up, then price of everything goes up because everything is dependent on oil-based transport, and thus even if there were no monetary inflation and money supply was fixed, there could be still price inflation)

The second inflation might be affected by the first one (like in cases of famous hiper-inflations, like in Weimar Republic), but it doesn’t have to (like in the case of post-2008 crash central banks policies result). The two are related, but there are so many other factors, that it’s hard to guess how one will affect the other.

PS. CD and bonds in Switzerland basically in current conditions are not worth a dime and it’s better to just keep cash on a bank account.

In addition as long as the European Central Bank (ECB) keeps their 0% policy on money lent to member states, swiss bonds largely wont have a noteworthy positive yield.

When the ECB changes its course bonds might get interesting again.

1 Like

By reading and partipating to this forum, you confirm you have read and agree with the disclaimer presented on http://www.mustachianpost.com/

En lisant et participant à ce forum, tu confirmes avoir lu et être d'accord avec l'avis de dégagement de responsabilité présenté sur http://www.mustachianpost.com/fr/

Durch das Lesen und die Teilnahme an diesem Forum bestätigst du, dass du den auf http://www.mustachianpost.com/de/ dargestellten Haftungsausschluss gelesen hast und damit einverstanden bist.