Thanks Kane,

I never found these for UBS, while Credit Suisse had a full public page about it, if someone is interested, these where the contribution at Credit Suisse (it’s still online today) not sure for how long.

@kane Are the rates listed in the table total contribution (Employee + UBS) or are they what UBS chips in? What are the rates UBS is paying for and how much can the employee pay?

I am asking this because the numbers you gave for BVG (Minimums) are the total rates (Employee + Employer) and this is usually paid 50/50 by the employee and employer.

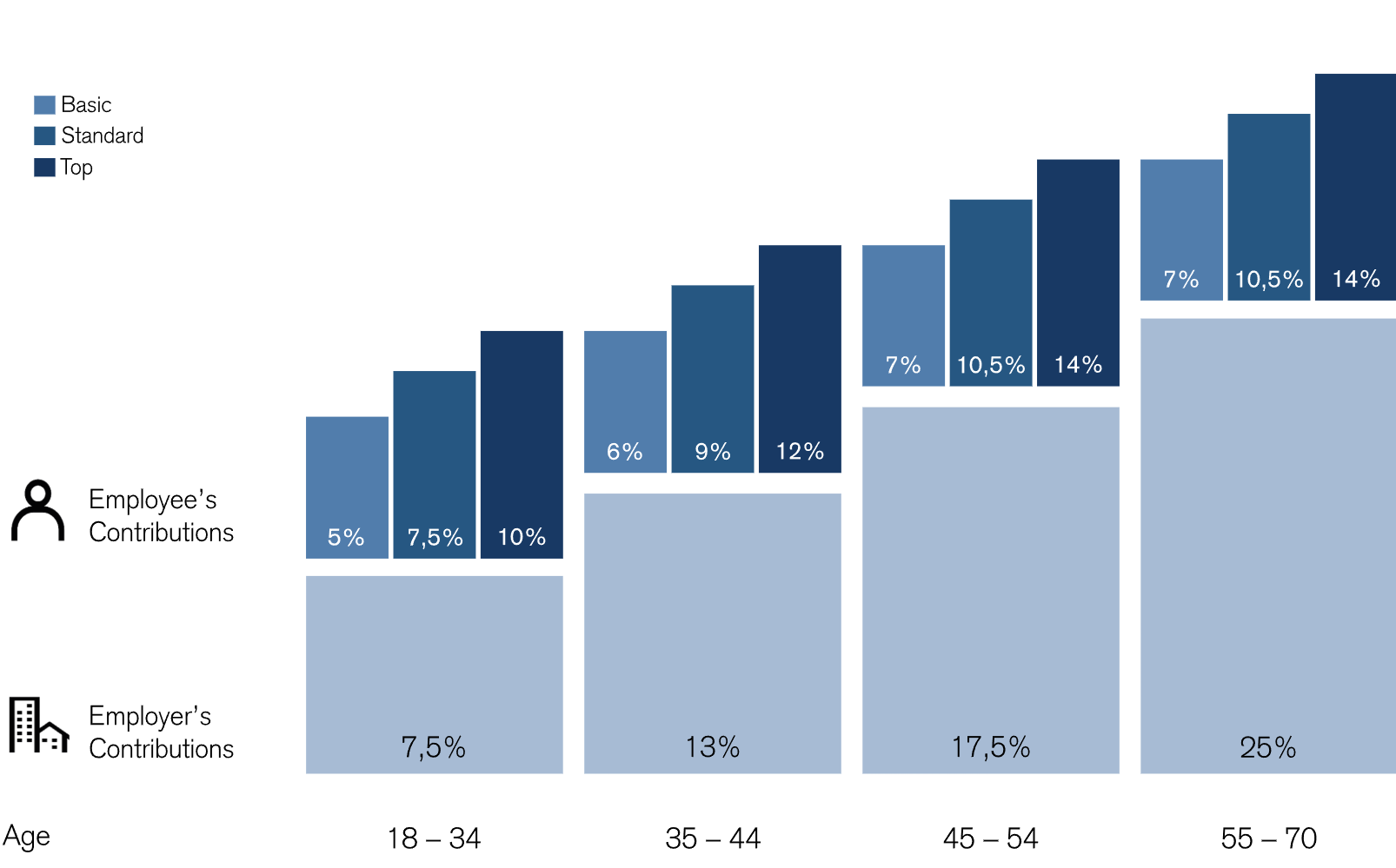

these are just what UBS pays, on top is employee contribution. That varies again by age group and employees can choose between three different contribution options (on a quarterly basis).

E.g. for age group 35-44 it’s between 3.5%, 9.0% and 10.0%/11.5% (salary depending). If you opt for the highest contribution, its 13.5% UBS + 11.5% employee = 25% yearly income. The most extreme case is 55-65 years old, and opting for max contribution, that’s 41% of yearly income (27.5% UBS + 13.5% employee).

My information might be outdated, I left a while ago.

Honestly those are underrated (and buyin potential is huge with more unlocked every 10y so it’s very flexible how much you can shove into the pillar, esp given the more than decent performance)

I am simply amazed how UBS is managing to return such higher interest on pension funds (where the risk profile is complex and restrictive) but struggle on their active funds to beat indexes.

Which numbers are you referring to?

The discussion above is about contribution %, not annual return % (unless I missed something? I didn’t see the return history, at least in this topic)

Sorry I think I might have mixed the threads. But on this forum is was mentioned that UBS has best pension fund in Switzerland and also there was a documentary on one of the Swiss channels sometime back

@kane Do you remember anything about “coordination deduction”? ZKB was deducting ~23K from your salary while defining your insured salary, which is basically used to calculate your savings.

As far as I know, the law limits PFs to a 50% equity allocation. Coincidentally, the PFs with the highest returns have between 40% and 50% in equities. A prime example is Profond, which has had a high equity allocation for decades.

For (1) iirc they have lower conversion rate and can’t convert the full sum to annuity(?), which reduces risks and redistribution. But my guess is that (3) accounts for most of the extra performance (as mentioned, profond has high-ish conversion rate and high interest rates).

(2) isn’t relevant for the fund performance (but it’s a nice perk )

for 2, what I mean is, if they invest aggressively and then have a shortfall due to bad stock market performance, they might have contributed to plug the hole.

I have not worked in that area, but andectotally it‘s a combination of things: excellent real estate portfolio and other investments, low or no fees, good managers, and most importantly very little „umverteilung“ from active contributers to retirees. They aggressively reduced the „Umwandlungssatz“ already a couple years back.

That’s not really supposed to happen and is extremely rare (it’s one of the most extreme measures), I think you’d need to be below 100% of reserve first before even considering something like that.

(Before contributing, they’d first have 0% interest, profond did that at some point)

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.