I think we don’t really need to look very far, there are already countries with a declining population.

What happens, as the article describes, is that rural regions get deserted at an increasingly faster rate, while the pressure on the major population centers and desirable areas is the same if not higher than countries with increasing populations due to higher internal migration.

Just take Italy, 1€ houses in the countryside, still rising prices in major cities. This with a 40k population decline last year.

Same in Japan, which is further down the process with a 900k population decline last year.

I would say the trend is clear: anything near major population centers is “safe” from population decline for the next few decades at least. Rural not so much.

I think as people get older they want functionality more than aesthetics. So depends on what rural is in terms of infrastructure, logistics , mobility etc

Old people move from cities to rural areas? I plan to do that. But yes, not too far that it’s out of the way of ‘everything’.

But you will have more time, so taking a bit longer to get into the city, maybe with an e-bike, isn’t as much of an issue as a long commute to work would be.

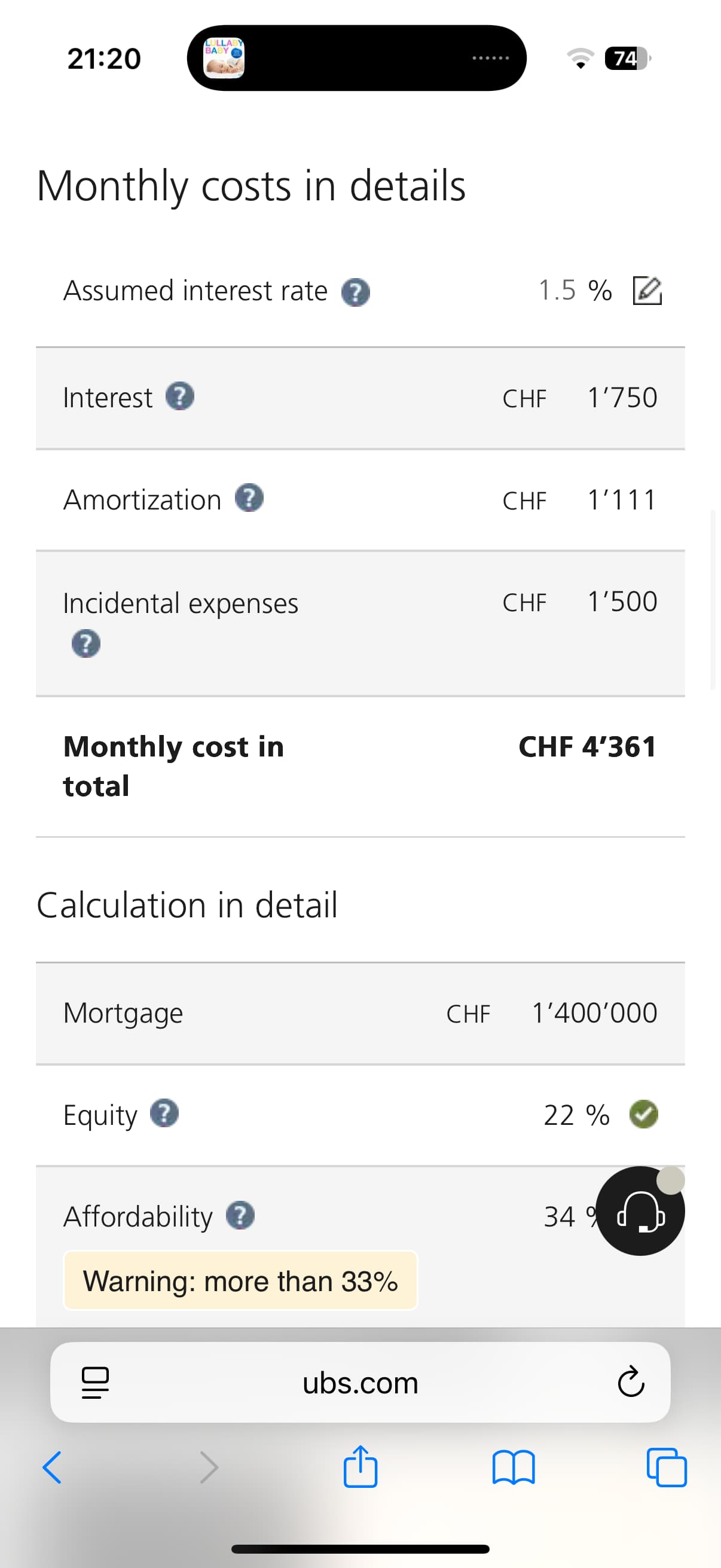

These 4.4k on the screenshot include also “Incidental expenses” which is not part of the mortgage cost - it’s what UBS estimates owning the house will cost you in repair and maintenance

UBS is using this to estimate your risk profile.

This is not only mortgage interest, it includes amortisation & maintenance cost estimates that you will incur during the period.

I wouldn’t use these numbers to compare rent vs own. Reason is that amortisation is amortisation your ownership of property. It’s not a cost , it’s an investment

But these numbers are good estimate of your monthly expenses which you would incur if you buy this property

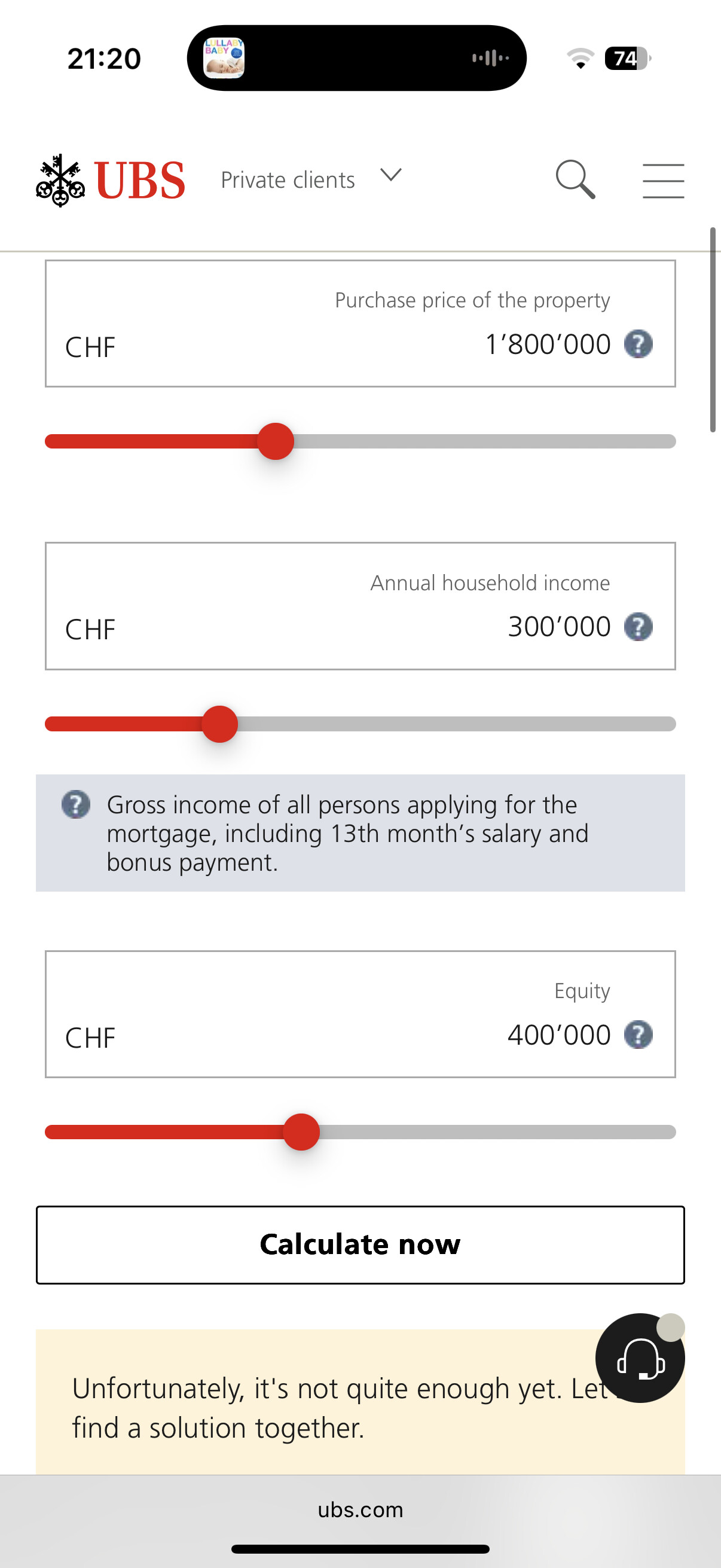

Any other consideration? Apart from the fact that the tax office will use a virtual possible rent value of 4.5k and then add 4.5k*12 =54k as additional income to estimate tax rates?

I needed to know if monthly expected cost of owning makes sense or not.

My current rent of 4.4k includes monthly provisioned charges.

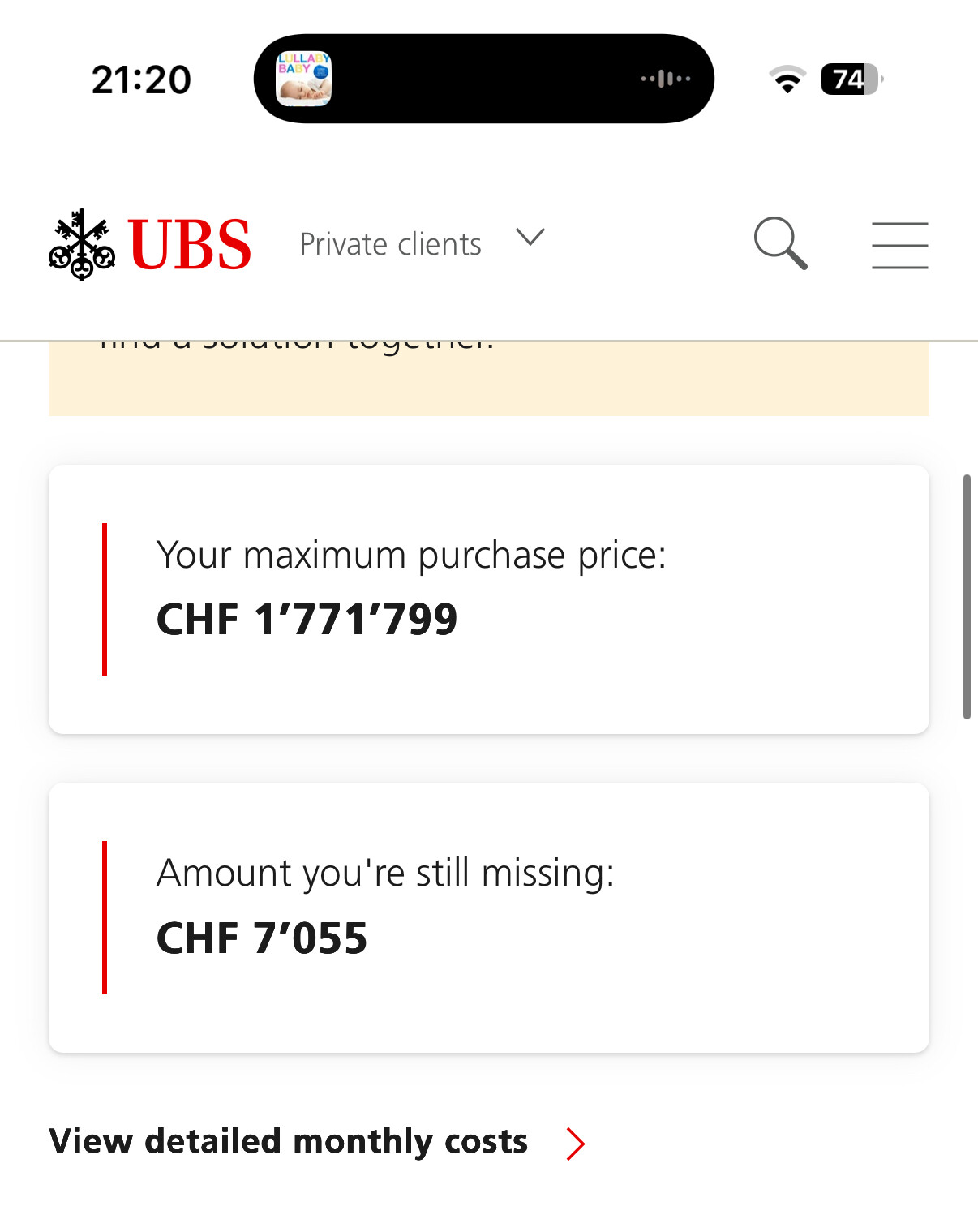

Based on the estimator and excluding incident cost this brings the value to 2900 and then with 400 charges this is 3300 so around 1100 less per month compared to what I pay now as tenant.

I would approach it from a different perspective—comparing rental costs directly with “interest + incidental expenses,” since these are pure outflows, whereas amortisation reduces the debt and increases your equity share. So: 3’250 vs. 4’400

Indeed but as I don’t provision these in my rent in a way (for example I rent an unfinished apartment so if bridge breaks down it’s on me to repair) I was doing this kind of comparison.

That’s not right comparison.

Owning home has much higher costs than renting home.

We are talking about repairs of the home itself. Not these small things like tap repair or broken glass.

This is what most banks use as average costs -: 1% per annum.

Another way to think about it would be that everything in the real estate will needs to be replaced/depreciate over time except the land on which it is built. So banks have made estimates on what that cost is as percentage of full asset price to keep things simple.

I would really recommend you to talk to some actual real owners and understand costs of owning & maintaining a home. People who have owned homes for 10-20 years might give right advise.

don’t forget you have to pay ~5% on top of the purchase price for the notary, “registre foncier”, “cedules hypothecaires”, you cannot borrow to finance these

your imputed rental value looks a bit too high to me, but my experience is in Vaud, maybe Geneva is more greedy

put in your calculations the extra taxes you’ll have to pay because of the rental value

but you can deduct from taxes the interests, the maintenance charges of the PPE and your own repairs (not improvements), in Vaud you can deduct maintenance on a forfait basis which is quite larger than what I was actually paying

Overall it looks like you should be able to fit easily in your current rental budget, but 1.8M for 100 sq.m. in Geneva countryside seems expensive to me

I have used some online estimators in the past, but they were really simple.

Going manually with a simple spreadsheet is probably the best you can do, at least you can tailor to your own situation, income, taxes, risk appetite, …

I am a homeowner (three-storey house) for over 15 years now, so here’s my perspective:

Regarding expected costs, there’s quite a big difference between owning an apartment (which, if I’m not mistaken, is the target for our friend) and owning a house

1% of CHF 1.8 million is CHF 18,000 per year. This amount should, on average, be sufficient to cover both small and major repairs. For apartments, major repairs are typically shared among all owners in the condominium, which reduces the individual burden

Some minor repairs can be done yourself (depending on your skills and willingness), which can help reduce costs (not really my case, though)

After a few years, appliances such as kitchen equipment (fridge, oven, washing machine, etc.) may start having issues. However, we’re talking about costs ranging from a few hundred to a couple of thousand francs, which should be manageable within the 1% budget

also correct; mortgage interest deduction should usually allow to fully compensate inputed rent (to be checked based on individual situation)

another point is that when deducting mortgage interests you may be limited in recovering US withholding taxes through DA-1 (check the relevant threads on this topic)

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.