Is there any way to automate a transfer from a Swiss bank into IB, convert CHF to USD and then buy VT ETF say on a monthly basis? I started last month to buy VT as explained in one of the guides but it was all very manual…

So it would be possible to write a simple program that does that for you.

However you still need to keep the gateway updated and authenticate the gateway each month.

No really answering the question, but if it’s a hassle why not do it once of twice a year instead of monthly? The time in market difference is probably negligible in the long run.

Now you can do it through the web interface directly on the web account manager.

It really take 3 min and maybe 10 clicks. Not automated, but a little easier than through the Workstation

Maybe another interesting point that has not been discussed so far: you can enable fractional trading now which allows you to buy VT for USD 500 which would buy you 6.0469 VT instead of having to calculate how much VT you can buy with a certain amount.

Especially interesting for people who want to buy a security with a high price e.g. SPI Extra (CHF 1900 per share)

good point. my objective was to remove market risk by monthly purchases but the ETF is so broad and in the long term horizon it’s probably not worth it and 2 or 4 times per year would likely suffice. thanks for the perspective

Is it still the case ? If I google “passive funds stock market share” I get:

19.03.2019 - Market share for passively managed funds has risen to 45 percent, up a full point from June 2018, according to data this week from Bank of America Merrill Lynch.

11.09.2019 - End of Era: Passive Equity Funds Surpass Active in Epic Shift. It’s official: inexpensive index funds and ETFs have finally eclipsed old-fashioned stock pickers.

There is the risk part of the statement. 5.2% is the expected return above the risk free rate, but there is the risk that the return is lower (or higher).

Here are some resources about the “index fund bubble”:

That leads to another question: how does the volatility matter in the context of “RE” ?

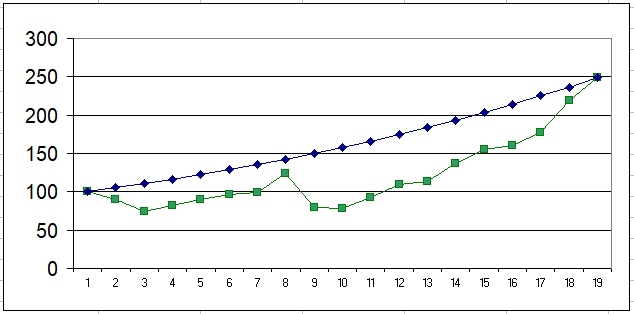

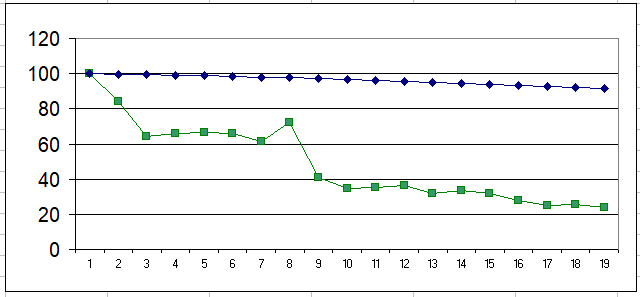

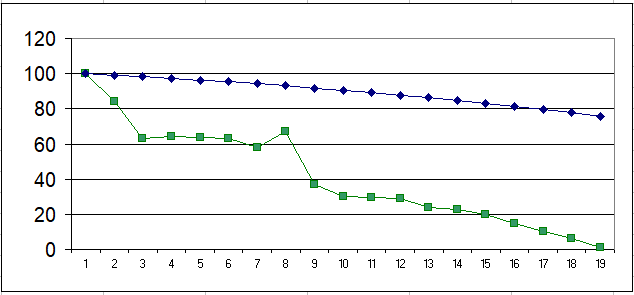

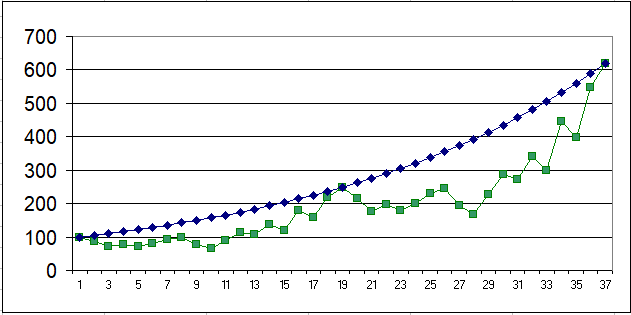

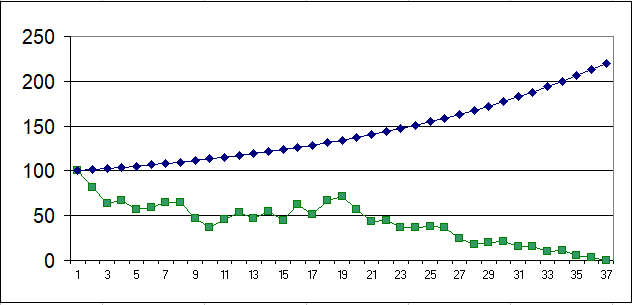

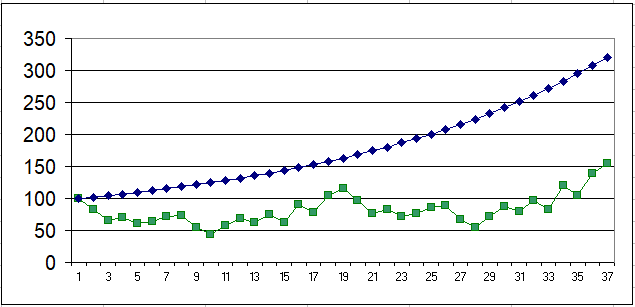

Here are two curves, one following an index, with an average 5.2% return on 18 years, one with a fixed yield of 5.2% each year (I assume the risk-free rate compensating for inflation, so 0% real). Everything is reinvested. As expected, the curves meet after 18 years.

Now, say I want to retire, and spend 6 units each year. Most is covered by the 5.2% return, right?

Mmmh, actually, not quite…

If I withdraw 6.05 each year

I’m broke after 18 years!

Why not using the App on your phone? Super easy and fast. I always sell my CHF.USD and then buy VT. I never timed it but I am pretty confident it takes not much longer than one minute.

By reading and partipating to this forum, you confirm you have read and agree with the disclaimer presented on http://www.mustachianpost.com/

En lisant et participant à ce forum, tu confirmes avoir lu et être d'accord avec l'avis de dégagement de responsabilité présenté sur http://www.mustachianpost.com/fr/

Durch das Lesen und die Teilnahme an diesem Forum bestätigst du, dass du den auf http://www.mustachianpost.com/de/ dargestellten Haftungsausschluss gelesen hast und damit einverstanden bist.