Maybe run a simulation what if the underlying asset drops by 20%, 50% or 80% and at what point margin call kicks in. I think margin call for mortgage is a bit later than brokerage

This should answer the question. leverage always makes sense when asset price goes up. And it makes no sense when asset price goes down. So the question is always about what will happen during investors‘s horizon

As a lender, I would rather have CHDVD with an ability to liquidate it whenever I want as a collateral (I wouldn’t go as high as to offer a loan worth 5x the collateral on stock assets, though).

As a borrower, I think nobody would care about the impact on the economy of over-leveraged stocks investors being margin called. I do think the impact of the price of houses dropping significantly such that many/most landlords have trouble maintaining their mortgage is more likely to elicit a help response from society.

First, both are very high risk. But then with the real estate you have less control.

In both cases you lose all after a loss of 20% and that is more than realistic after so many boom years. In both cases you will be asked to put in more money or sell. But here is an important difference: you can sell one share of stock, but you cannot sell one room of your house. There you are all-in.

In theory you can lose in both cases more than you did invest, but depending on the broker you cannot lose more than 100% of your investment in stocks. You can lose more, much more than your investment in real estate as happened in the 80s in Switzerland and in many countries since. You are asked to put down more money first, if you cannot the object is sold. But as stocks are more liquid you know the market price. You don’t know the market price of real estate and if it is a buyers market it can be much lower than expected.

I was just thinking about this buy-to-let alike investment after reading your first post. I see Saxo can provide 75% LTV (not sure if chdvd would allow this much leverage). Putting up 250k would allow 1’000k investment and you would pay 1.5% interest on it. Current dividend yield is ~3.5% (apparently not easy to find on Swiss real estate). So all in all very similar to cash flow of a highly leveraged RE investment just no hassle with tenants and maintenance?

Portfolio margin at IBKR is up to 800% multiplier, so you need 12.5% down payment. But it is risk based and I doubt an all-Switzerland ETF will allow for the max margin. Also if you start with the maximum multiplier the slightest volatility will throw you out.

I have both, a mortgage and a margin credit. The mortgage is at 0.75% and the margin credit at 1.05% interest rate, that can go down to 0.75% too when the credit is bigger. But the mortgage has a 13 month notice period while I can change the margin credit at any moment.

Despite both being debt, a mortgage compared to margin loan is different to me. A mortgage is based on the valuation of the house. The housing market is rather illiquid and a lender will not recalculate the house value regularly. With the limited housing supply and resulting data, it is probably also difficult for the lender to assess accurate housing prices, hence why they often just keep the initial valuation in their books. I also don’t think its in the lenders (in CH) interest to foreclose real estate (large scale) because in such a scenario every lender would be doing this and prices would plunge. Also you can fix your mortgage rate for x years.

With a margin loan, the lender (broker) sees the value of your positions in real time. The market is more liquid (until it isn’t in times of stress) and the broker can issue a margin call if they see to much risk in your positions.

Therefore I find mortgages less risky with more certainty compared to margin loans. But the amount you can borrow with a mortgage is limited by equity and house price so thats where margin loans have their spot.

How do you get up to such a high multiplier?

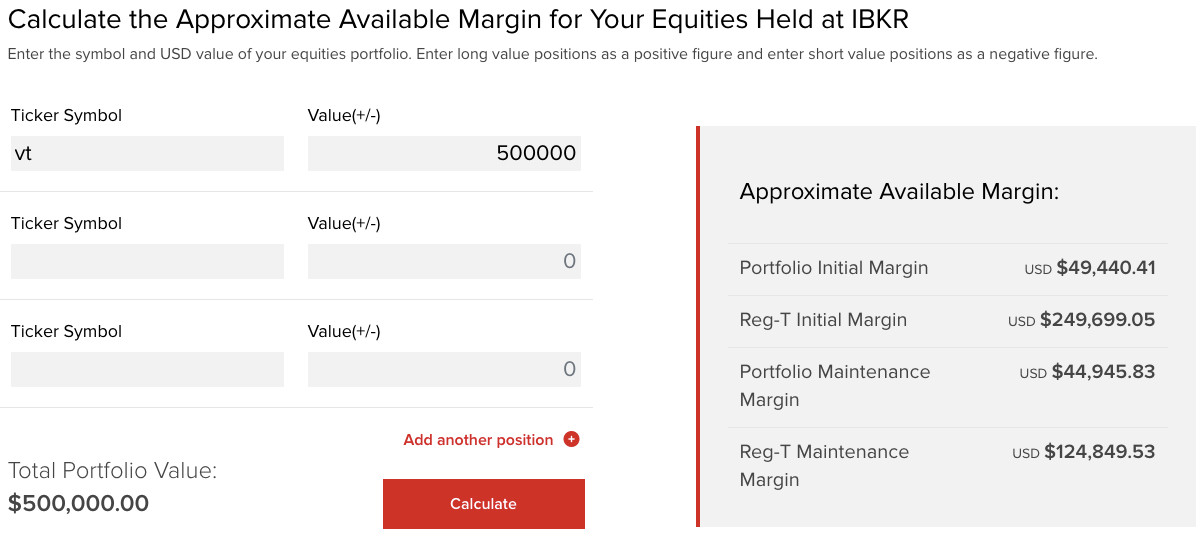

As an experiment, I entered this form’s favorite ETF and 500k CHF value. This only gives me a 50% multiplier (assuming reg-t initial margin is the available margin loan). 800% sounds to me therefore more like a theoretical value.

That reminded me that investing subs get the occasional smartass (not calling you one!) on reddit who think they’ve discovered the hidden money printer, asking the question “So, yeah, say I get a loan with <3% interest and buy XYZ stock/fund paying >3%, covering the interest payments, doesn’t this mean that I eventually get the stocks for free?”.

Don’t know the answer to the topic’s question, most of you here are more sophisticated than me!

The question I’m asking myself is would you do it today with the uncertainties of the future still ahead of us? Making good decisions in hindsight is easy but yields zero returns.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.