It makes a difference that is negligible. Funds will invariably hold some cash - so do VIAC and finpension.

The performance of 100% equity vs. 99% equity and 1% will be …the same, essentially. Less than 0.1% p.a., so way less than daily variation. Or comparable to the fund’s current premium over NAV.

(And before anyone chimes in, that’d still within the differences of expense ratios between different funds: true - but then you’d better start comparing tracking error! Does that mean I’m advocating to ignore expense ratios? Certainly not. But it’s nothing you should track down to the exact amount, I believe).

Principle, precision, pride - but not necessarily prudent.

(…in terms of your personal effort and resources).

Do they, actually?

In the prospectus I’ve found exactly one mention of the word, and, honestly, not much in their other figures on the web site.

…in the “portfolio”.

As Vanguard themselves are stating:

“Portfolio holdings may exclude any temporary cash investments”

It would line up with OP’s original post and link provided above above:

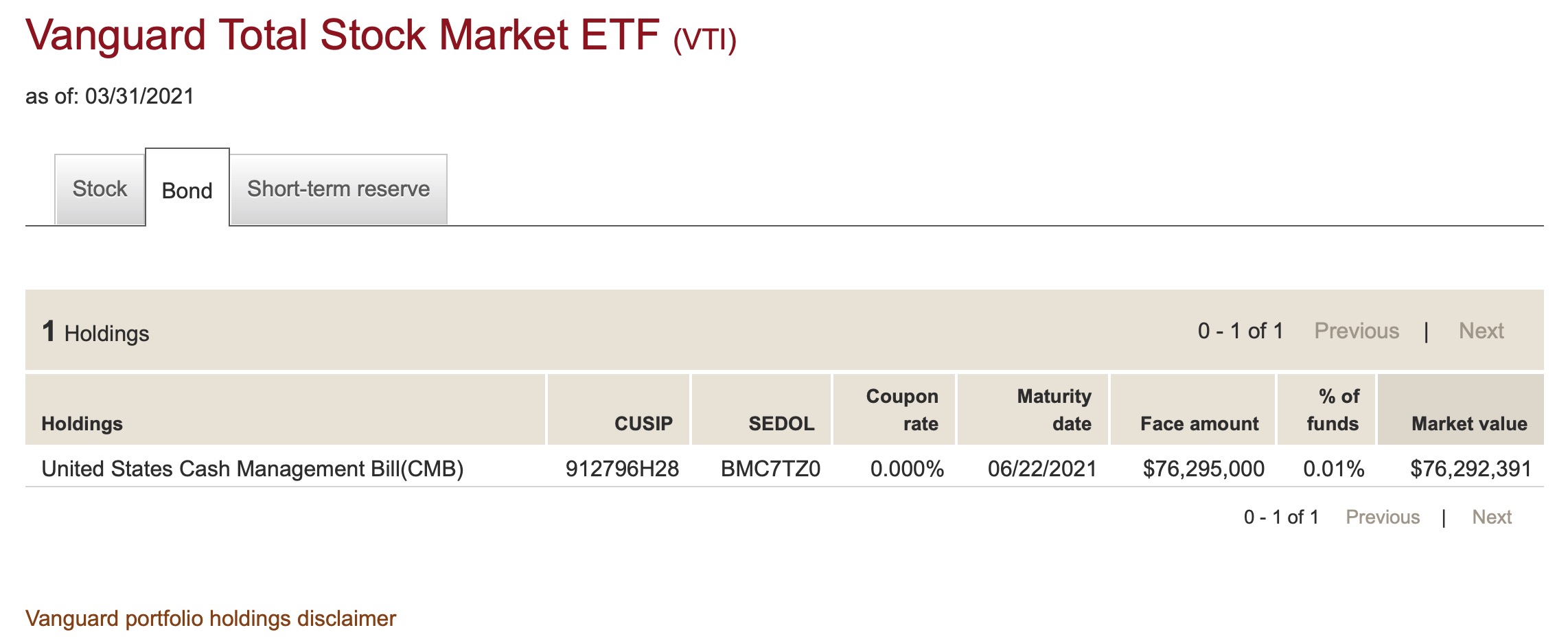

3722 stock holdings.

1 bond holding (with a maturity date in june), at a total 0.01% of holdings

2 short-term reserve holdings (liquidity funds), for a total of 0.89% of holdings

https://investor.vanguard.com/etf/profile/overview/VTI/portfolio-holdings