Crazy find that VALE, how did you come up with it ?

I’m going to start following it.

Also, on the Japense side, I was following the trading companies but couldn’t invest on them and now too expensive. So I reframed my approach and decided to only take Sumitomo and another trading company called Sojitz. Currently holding those two plus Honda.

End of January, I want to add into MUFG and that’ll be it for the Japenese portfolio.

If you like VALE, I encourage you to check TSE for value plays, lots of companies with tons of cash and below book value.

VALE is one of the biggest iron producers in the world. I have owned a fair bit of it, but sold as I’m concerned about the potential about the monopsony impact of China’s CMRG.

Very interesting thanks for this input. I was not aware of this (bless full ignorance) but it does directly impact me as I own RIO and BHP.

As mentioned above I own RIO and BHP since several years and specially RIO with the DRIP is one of my most successful investments even with the plumbing £. I bought them after my major subject in the university of resource management (in the Life Science curricula) around 2014. I’m aware of the impact on nature but still think that it’s better to have these “controllable” companies perform resource extraction rather than smaller local companies. That sad VALE is less diversified than RIO and BHP, therefore I had it on the radar for long time but never actually bought it (also never got assigned my puts).

Yes, they have increased their price quite a lot. However, I still think they are in a reasonable price range and will buy the next dip (I tried also puts but volume is almost inexistent).

TSE, seems to be a very small company with a market cap of about $20M, that is to small for me.

MUFG actually seems to be very interesting as well. What I actually find striking is the correlation of these companies I wonder if I should have bought simply a JP ETF rather than the individual companies. This remembers me of the Indian market some (maybe 2???) years ago where I could not decide on a company but should have simply bought a Nifty50 ETH (which I did not). Well in the end this is all just for fun beside my core VT and VWRL but it’s way more interesting to look out for companies

Thanks for sharing, amazing knowledge there regarding resource management.

I think there’s still upside, but, they carry that Berkshire premium now. I’ll concentrate on others.

I should have specified, with TSE I was referring to Tokyo Stock Exchange.

Regarding the market, Nikkei did really well last year and this month, but I’m not a fan of that index. I think Japan has a lot of bargains outside of Nikkei.

That makes more sense than Trinseo PLC (TSE) . Let me know if there are other interesting companies on the TSE. I’m still scanning and waiting for my Japanese friend to invite me again to his house

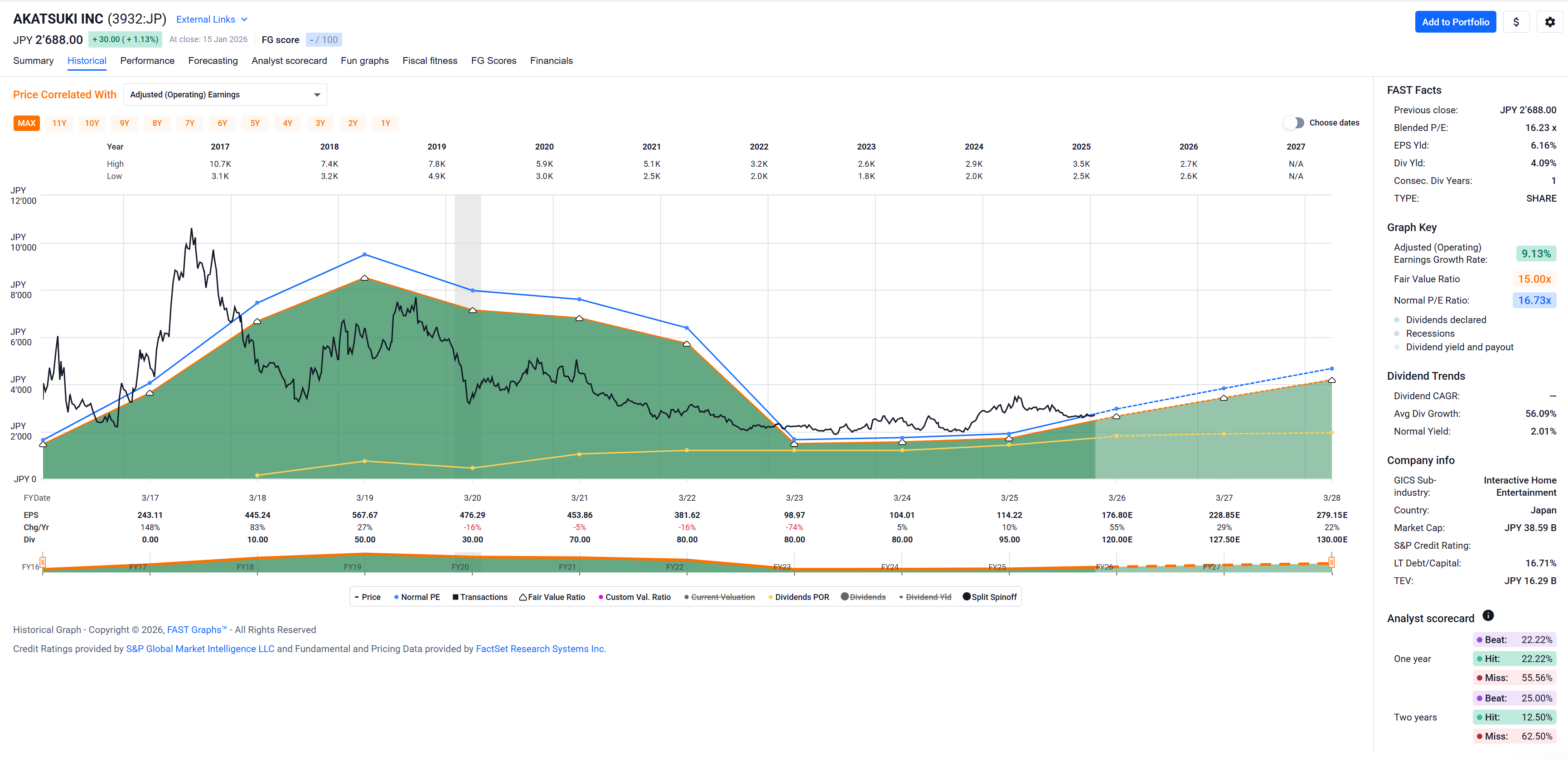

You have some Japanese dirt cheap shitcos, telecom and electronics/automotive manufacturers (these I’m watching just to see how high they’ll go xD), retailers, banking, transport and logistics, game companies.

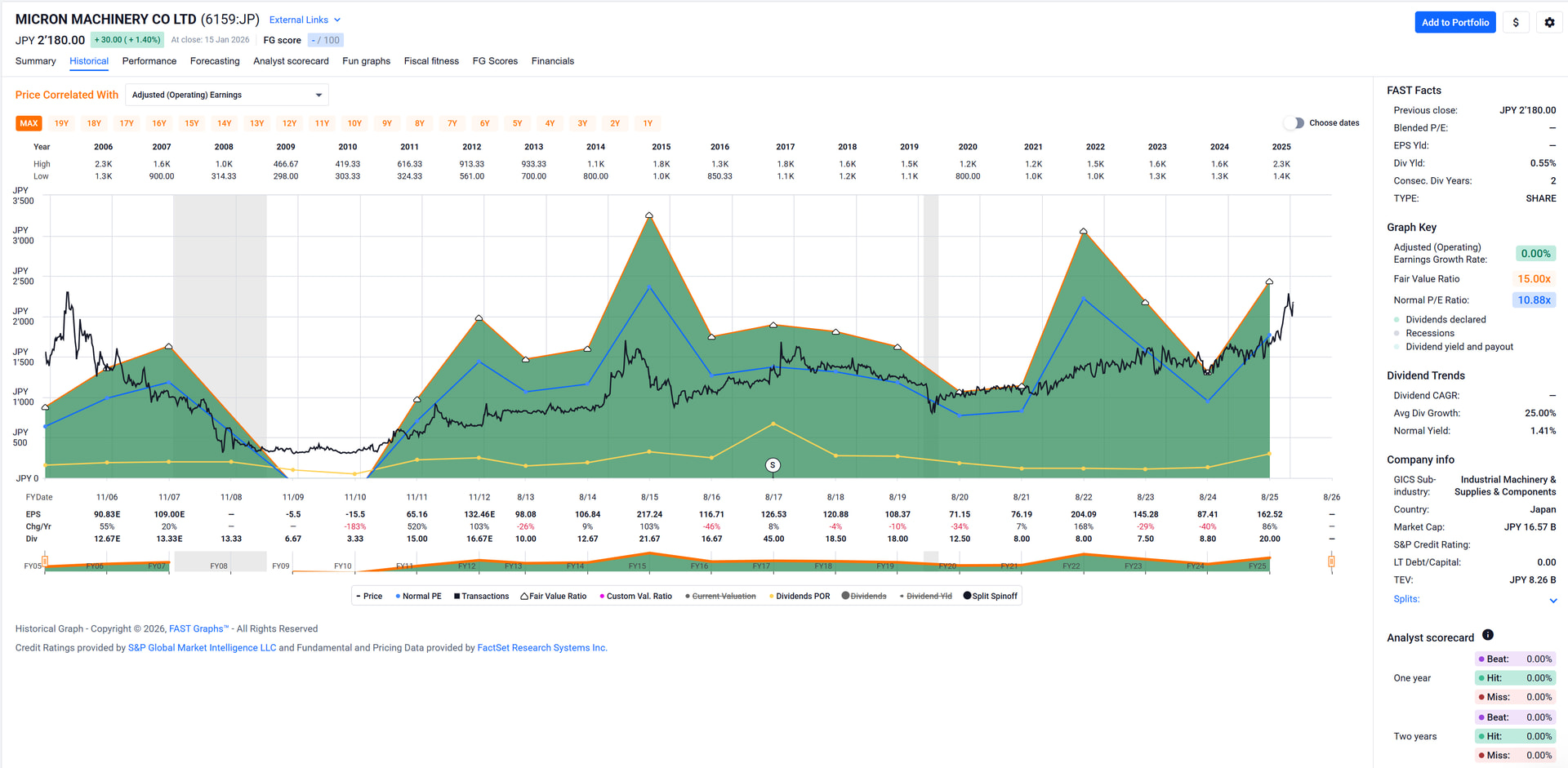

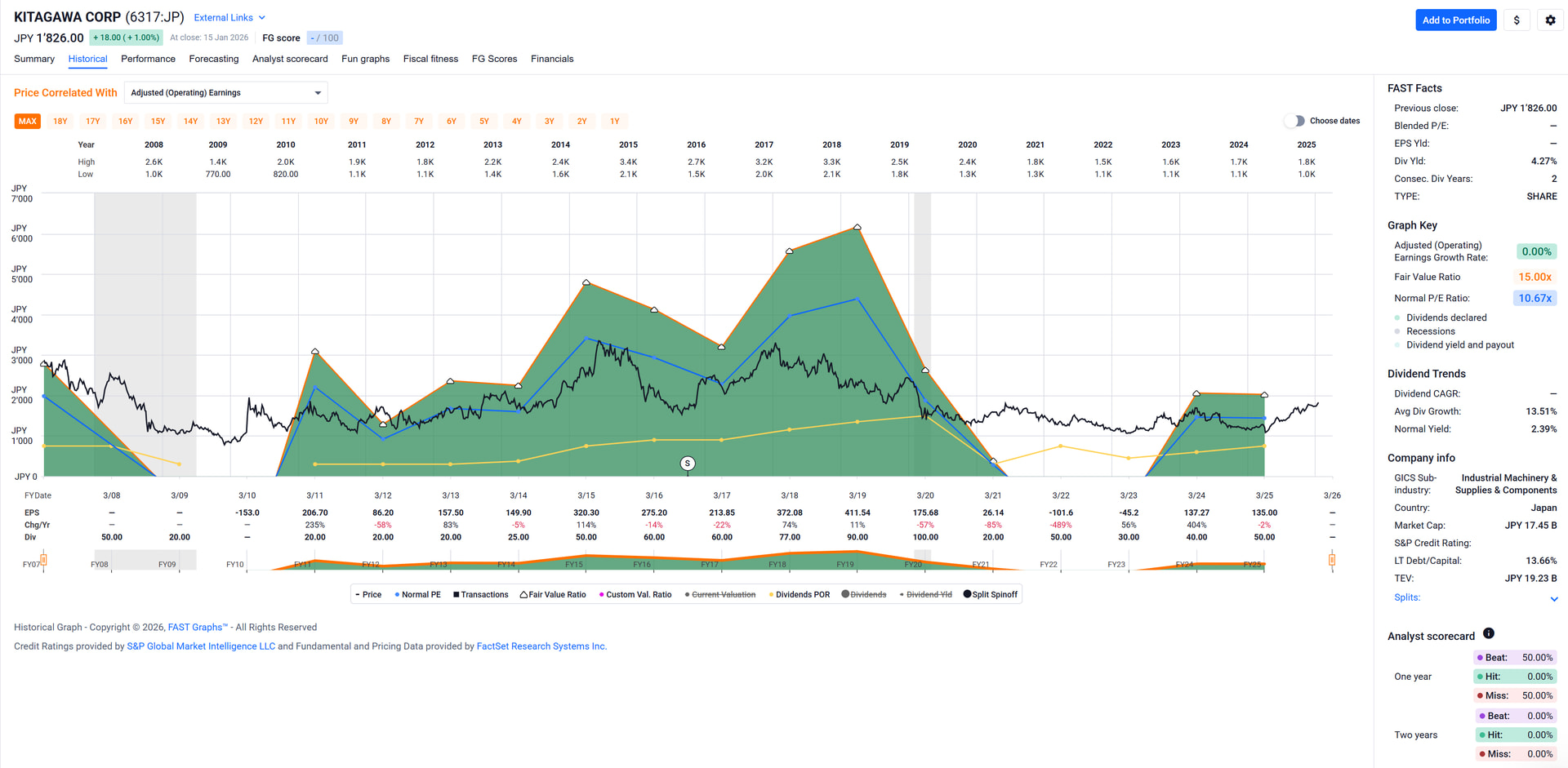

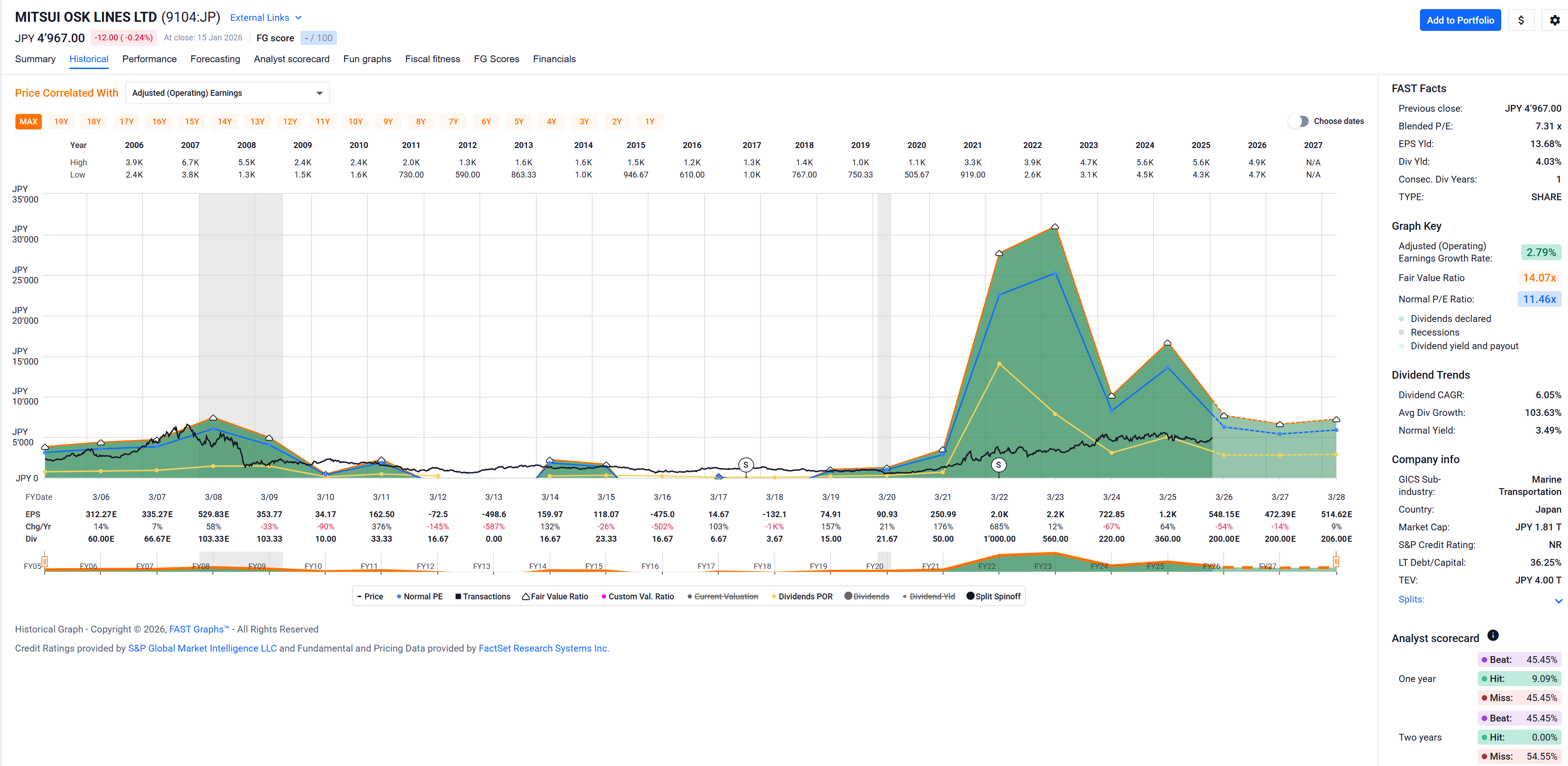

I am the most interested into Seiko Epson, since I know the company is solid, and they make great printers/scanners. Inpex, is the biggest Japanese oil company with a great dividend policy. Kitagawa is cheap af, the problem is the return on capital and those margins . Mitsui is cheap and profitable with great dividend.

I’m looking at dividends since I hold a loan in JPY, and on the TSE you’re forced to buy in units of 100. So, I want to buy the stocks for the long term and just pay the loan with the dividends.

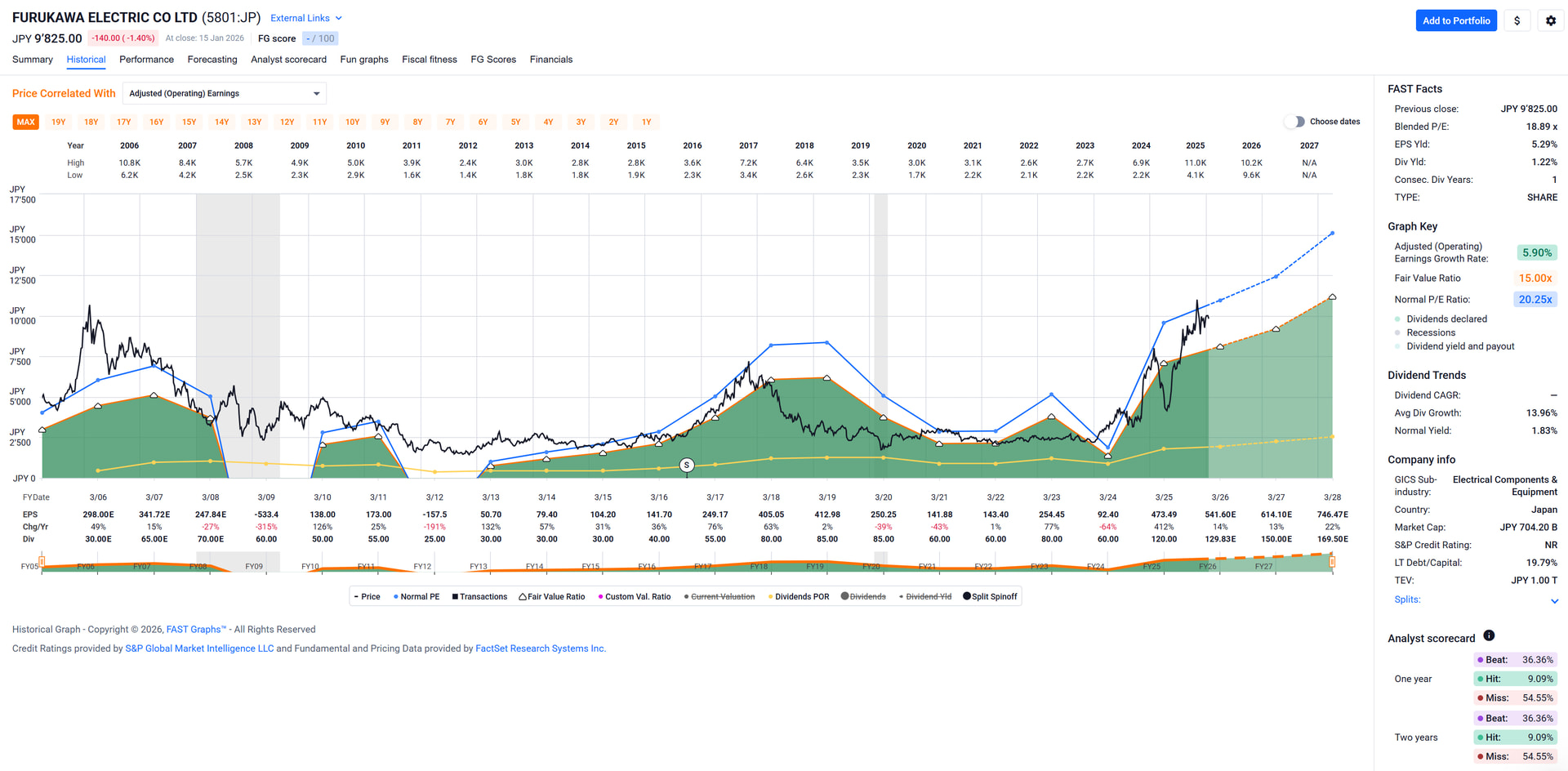

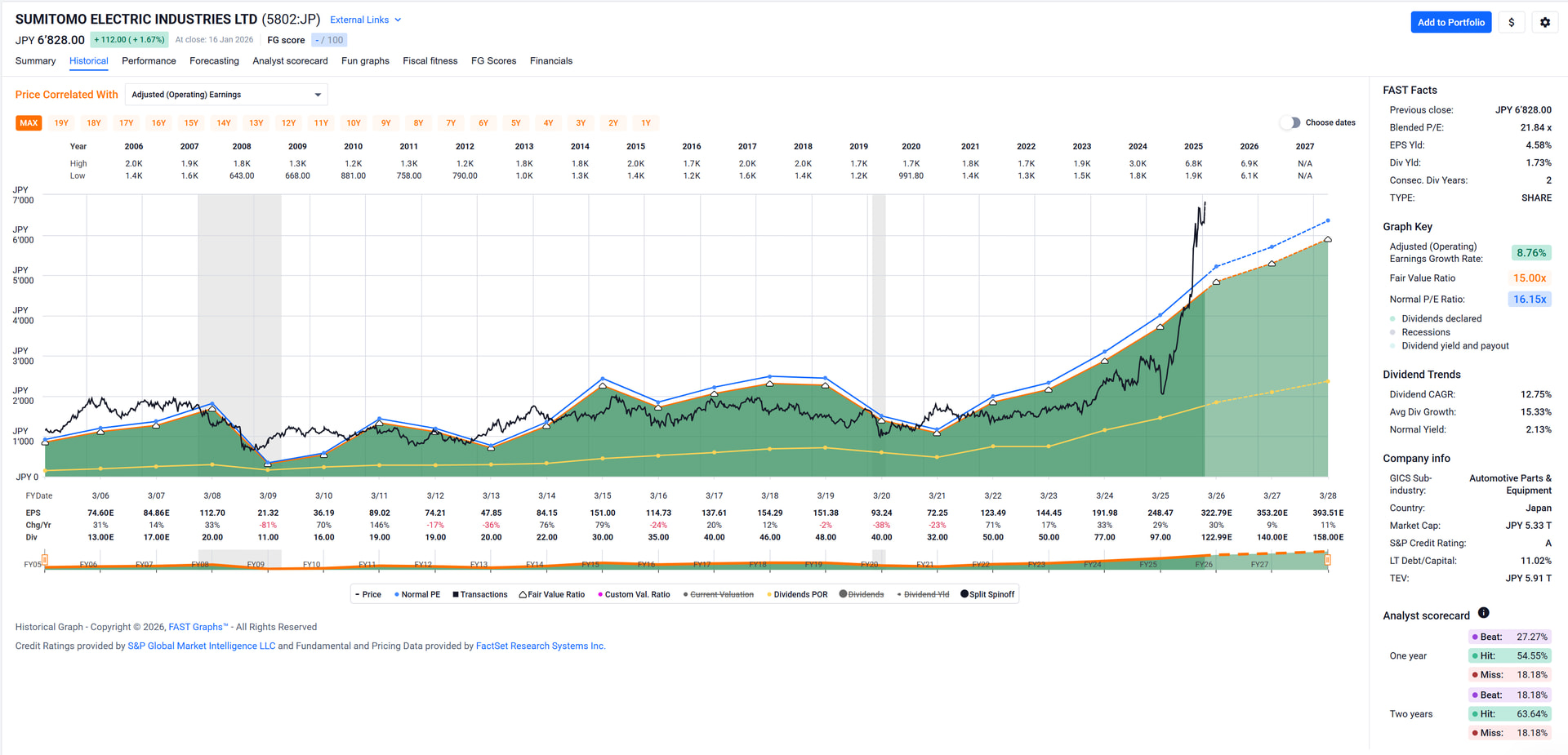

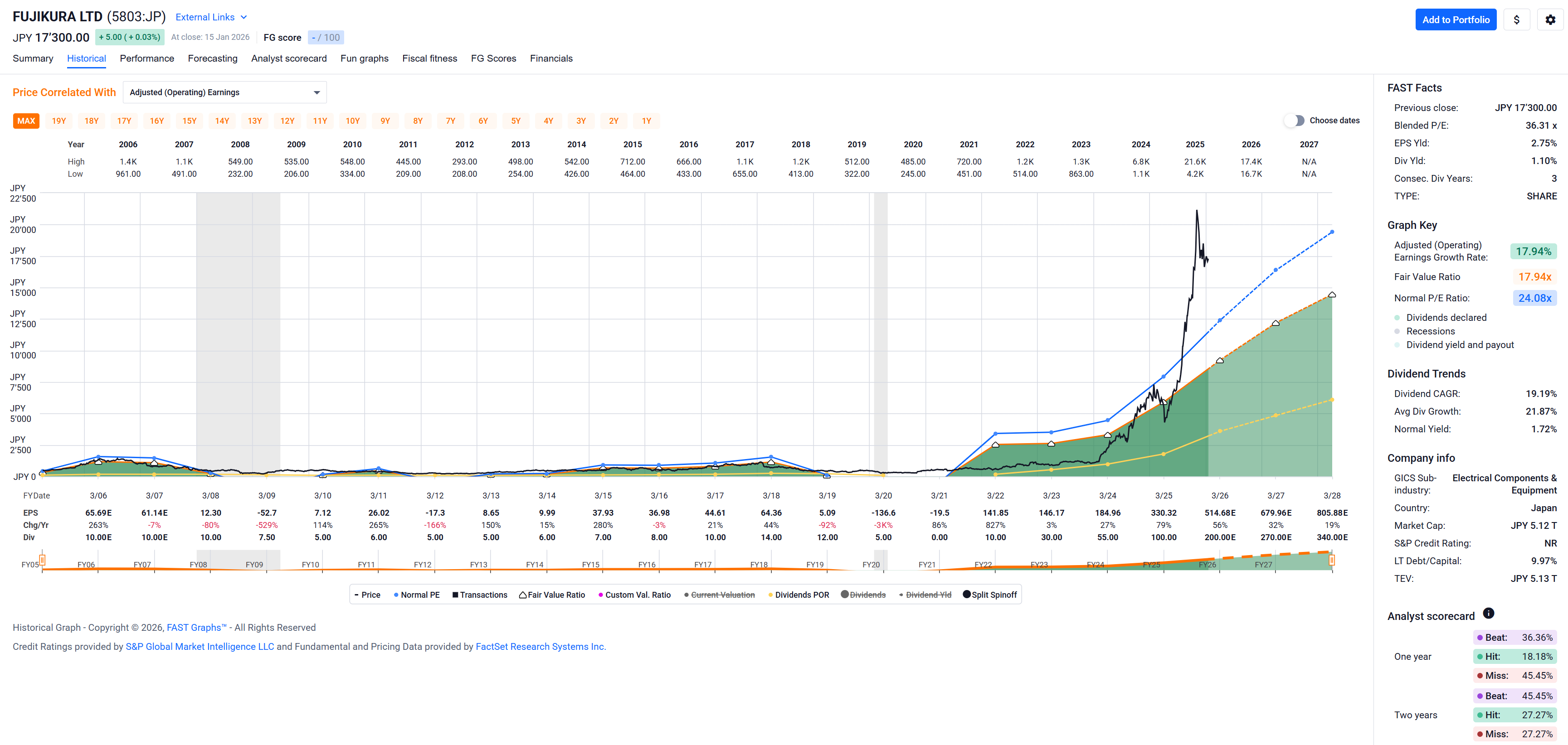

If you like the trading companies, they often have the different segments in separate companies, look at Mitsubishi that does everything from AC units, to pencils to houses. Most of the time, the other companies are also worth looking at.

One of my biggest regrets, along the trading companies, was not investing in tobacco stocks, particularly 2914 (Japan Tobacco). It’s like oil, people say it’s bad, the environment, health, etc; these companies have bad PR. But they just print cash. People keep consuming.

I sold all my JP stocks as I didn’t want to deal with the timezone etc. but couldn’t bring myself to sell 2914 so still hold some shares there. I hadn’t noticed there was a decent buying opportunity at the start of 2025.

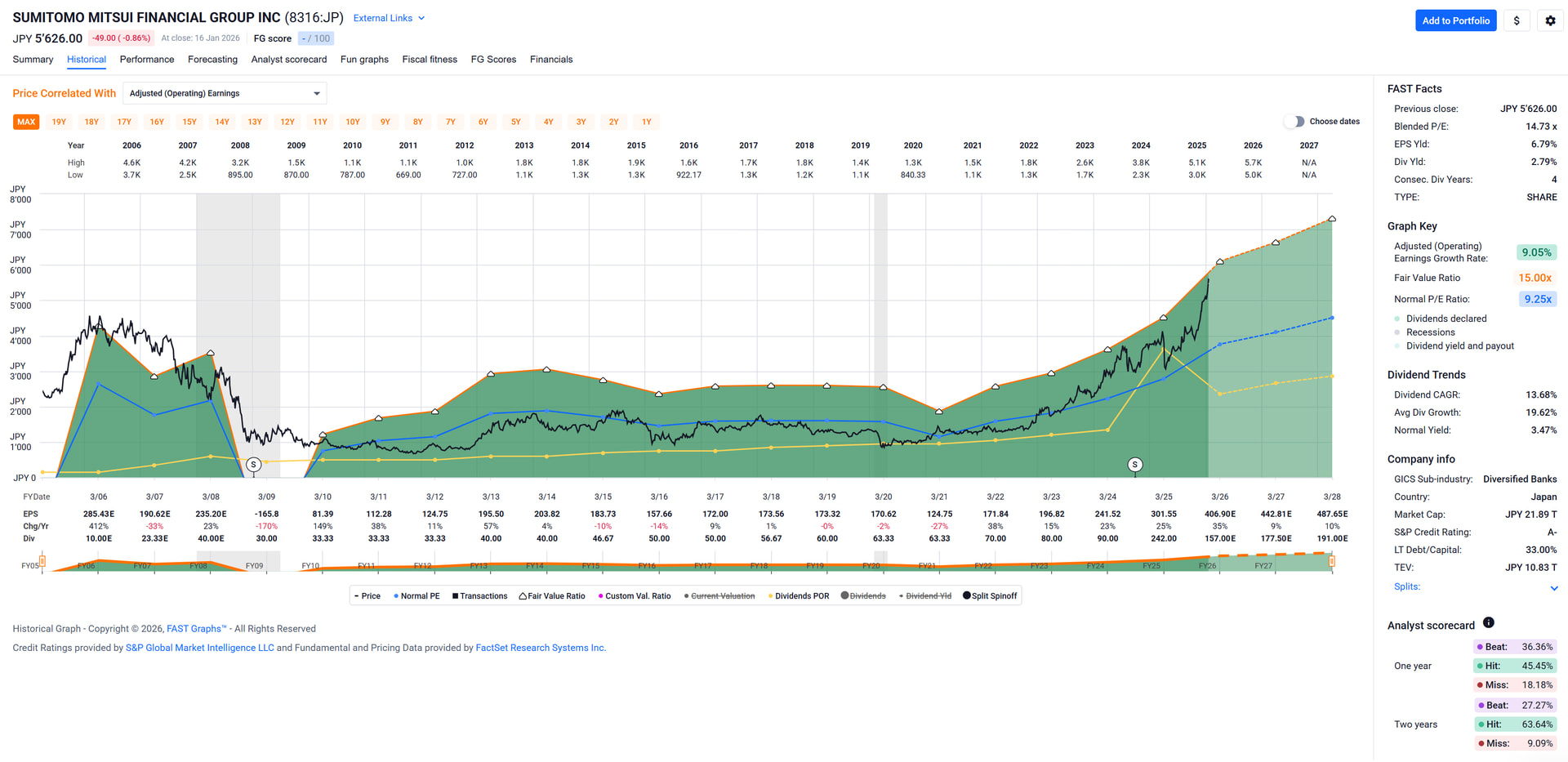

From a quick glance valuation POV (to me) only 8316 (Sumito Mitsui Financial Group) looks about fairly valued with a still nice earnings growth perspective, a cyclical but overall nice earnings growth history, a nice and steadily growing dividend, fairly low debt and a great credit rating.

It’s the only one on the list I would consider buying, I’m afraid.

I’ll throw in a bonus Japanese company from my watchlist that I just today upgraded to be eligible for buying, even though the dividend yield is (for me) on the low end: 6902 – Denso Corp. FASTgraph:

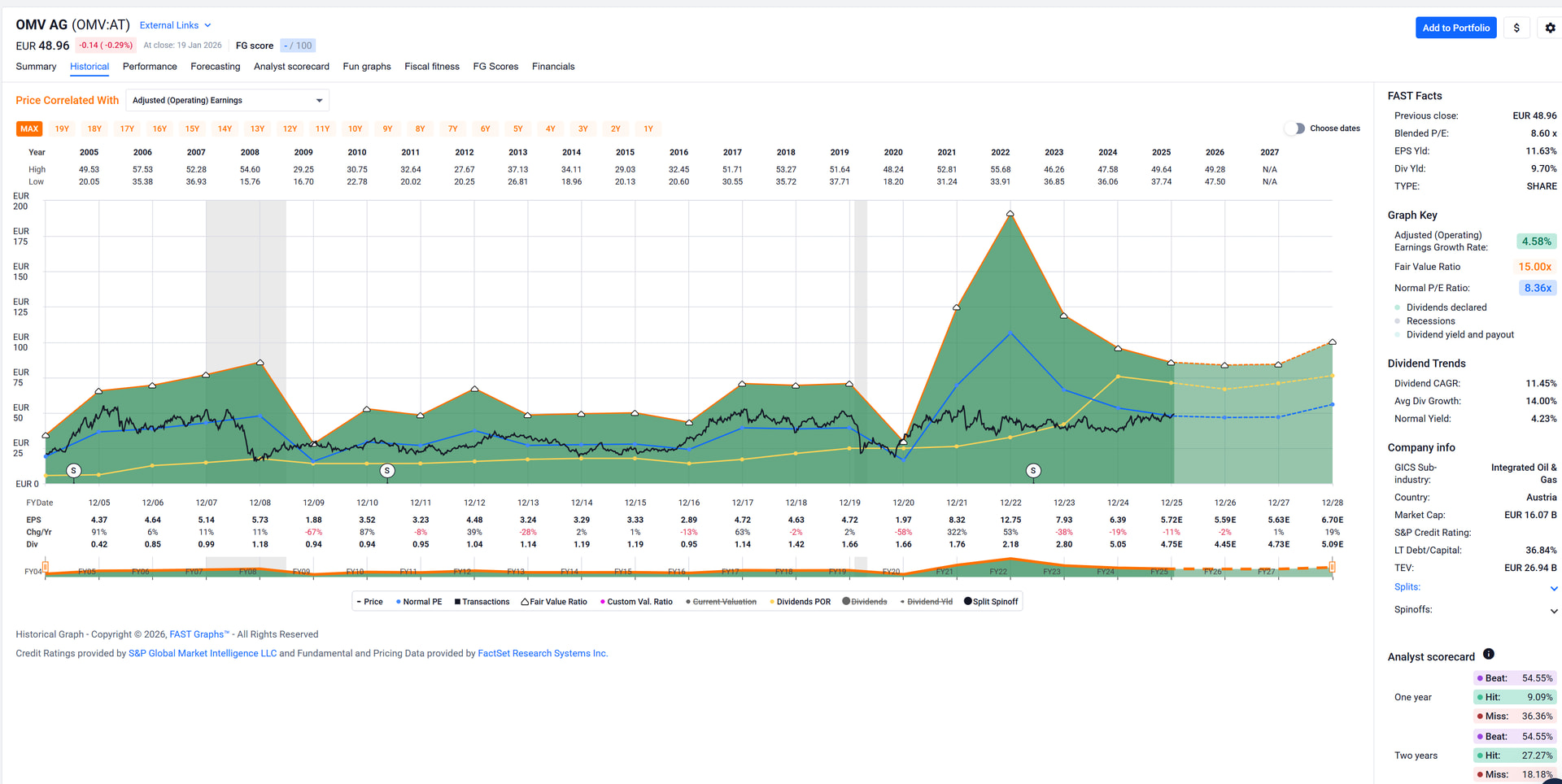

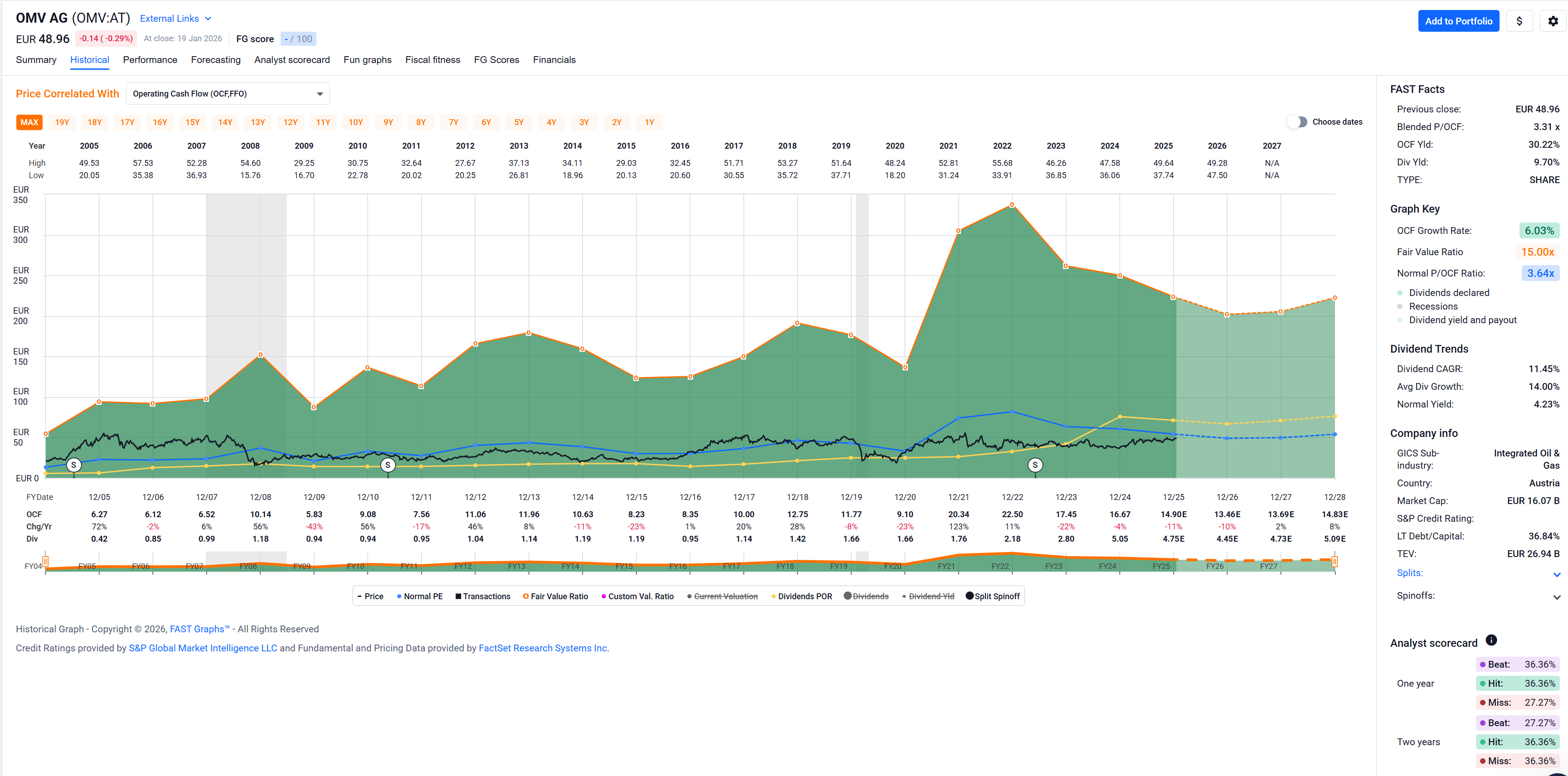

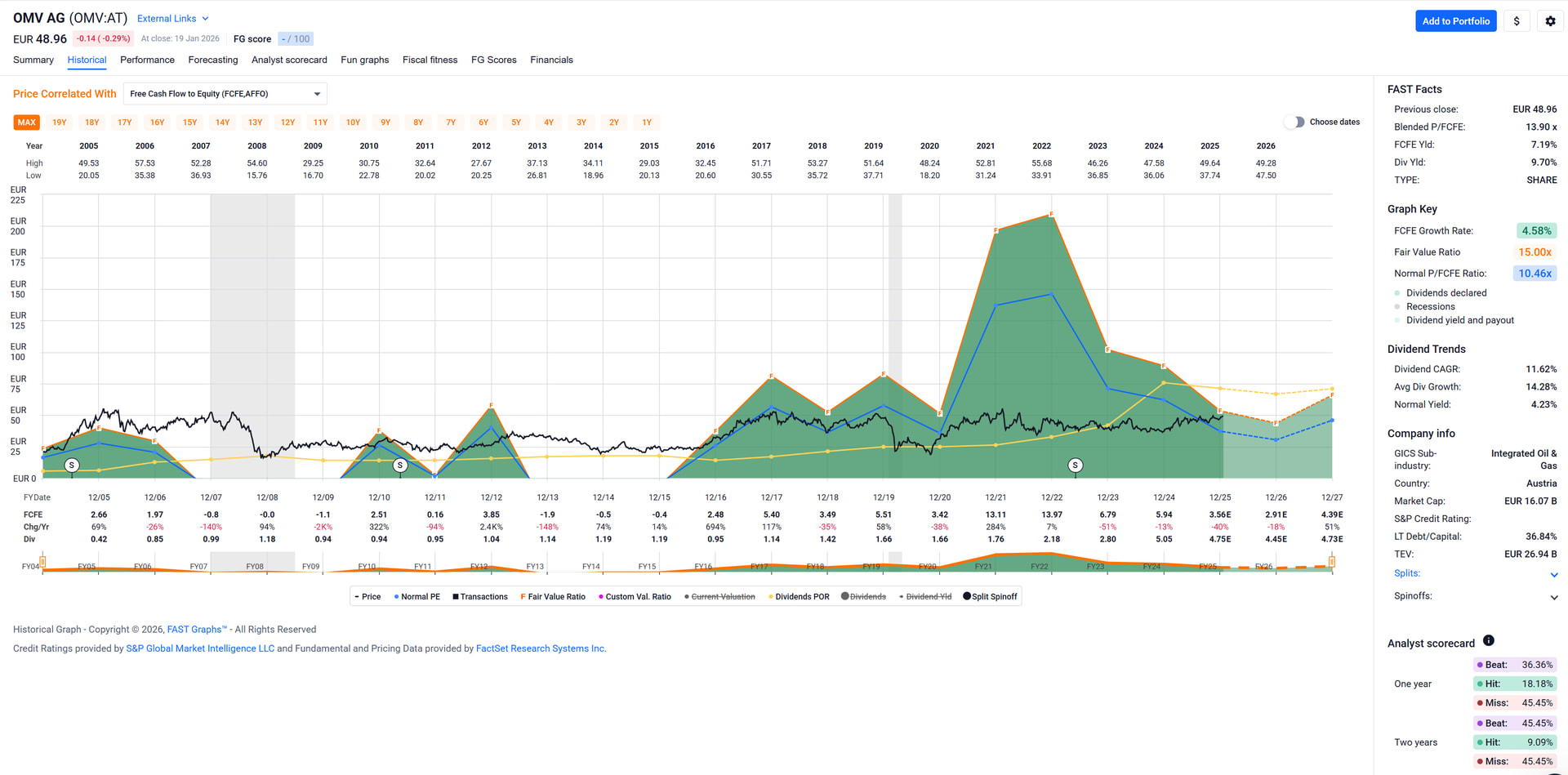

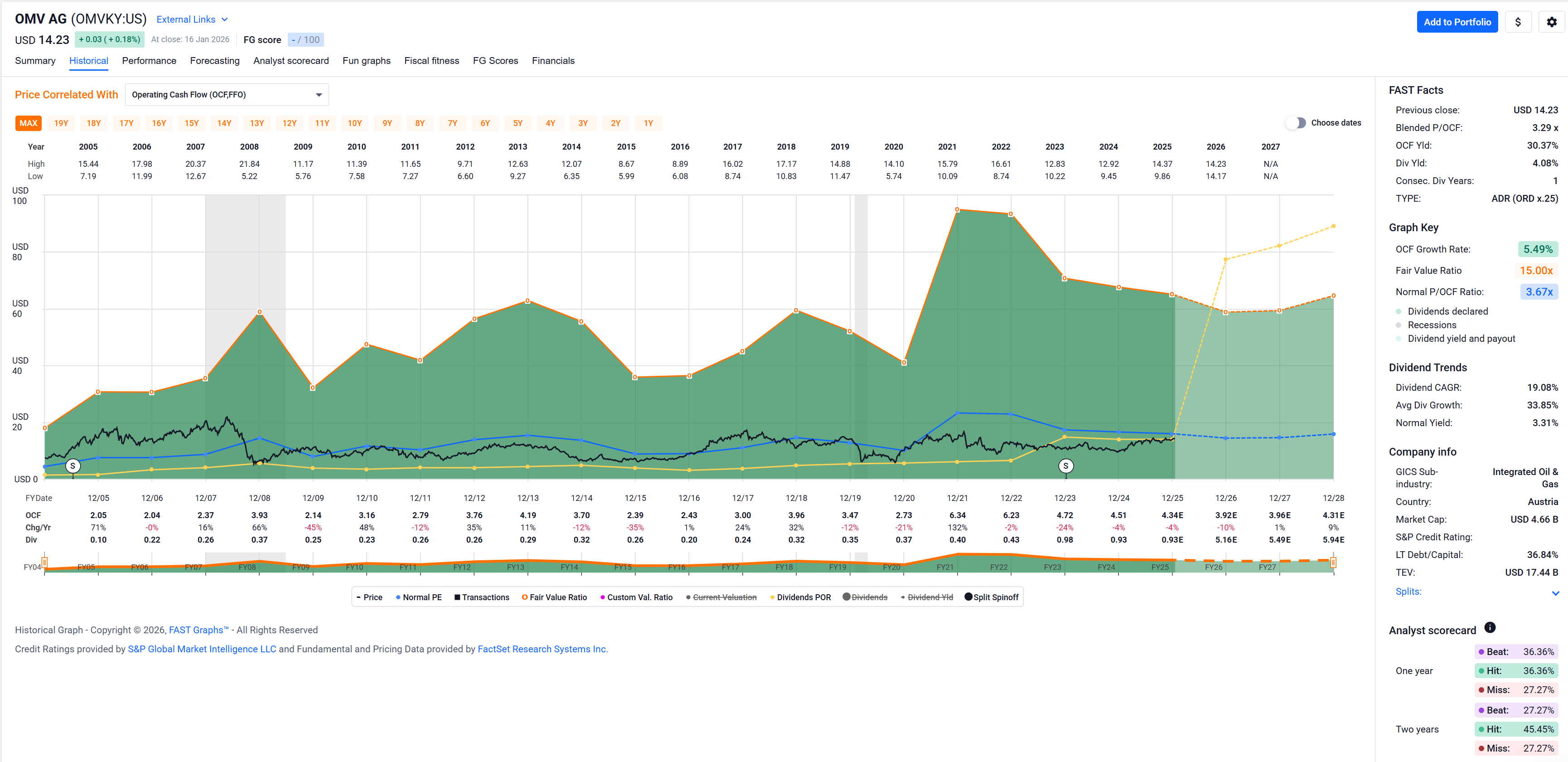

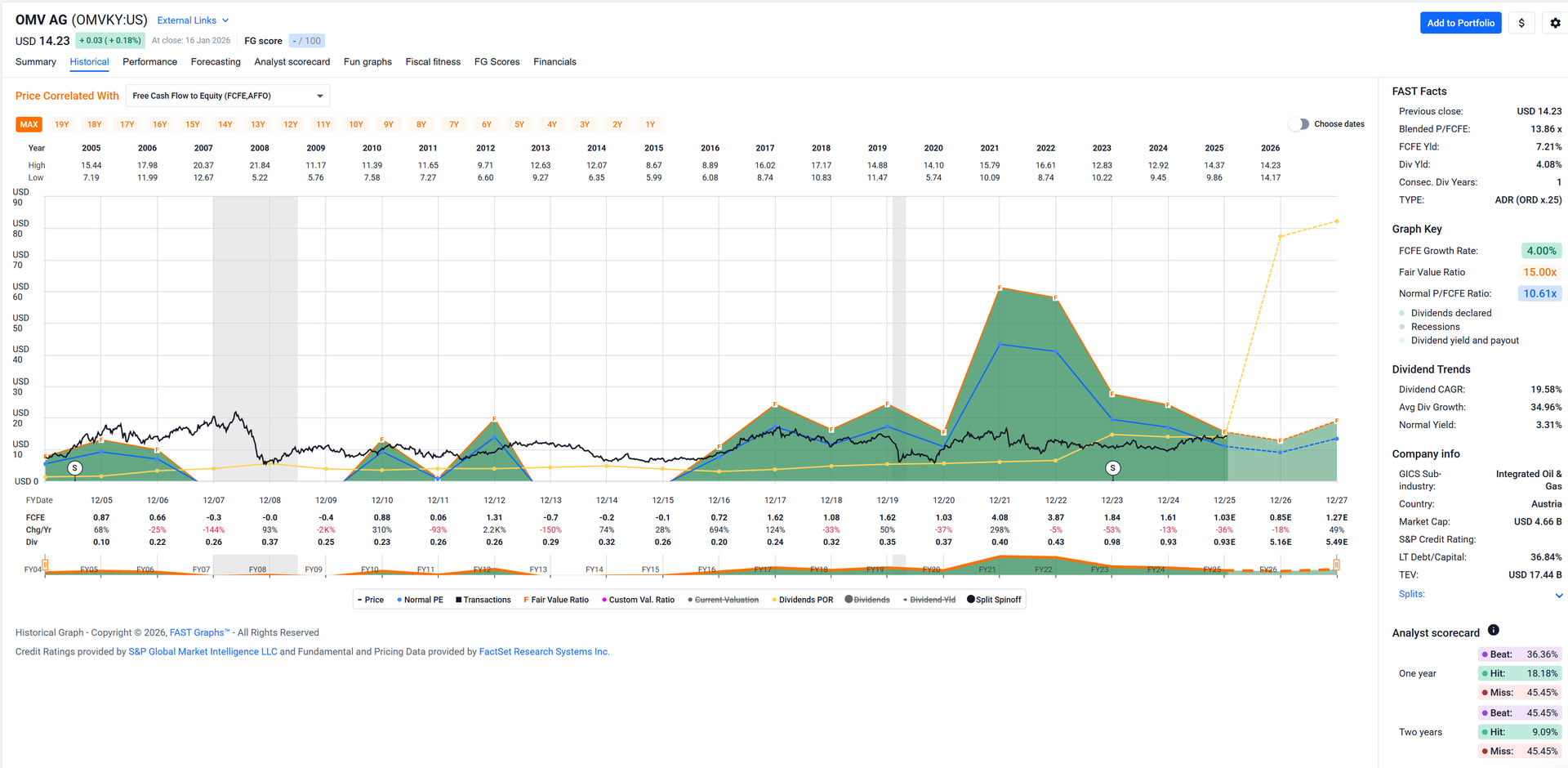

Came across OMV today.[$] Austrian Oil & Gas company, paying a huge dividend. Wouldn’t expect any price action or multiple expansion, but might be interesting if you’re interested in cash flow in EUR.

Haven’t looked into it in much detail, couple of yellow to orange lights for Goofy are a seemingly rather high payout ratio for their dividend and fluctuating dividends year over year. Green lights would be an almost 10% yield and an 11% dividend CAGR over the past 20 years.

Since @cubanpete_the_swiss will scoff at the FCF not covering the dividend: true, but look at past periods of FCF not covering the dividend – they still paid. Probably not unexpected for this kind of company with investment booms every now and then to gain access to new energy fields.

According to the interview with the CEO[$] they’re currently building up a large nat gas project in the Black Sea which might explain the drought in free cash flow for the next couple of years.

Anyway, as said initially, needs a deeper look before I would buy, but it is a stone turned over with some with some perhaps interesing bugs under it. Determining what kind of bugs these are is your own homework for now.

$ Since I want to get something … anything, really … out of the CHF 335 p.a. Swiss TV tax SERAFE fee, I click into about three shows – EcoTalk (weekly), Sonntagszeitung Standpunke (monthly), Bilanz Standpunkte (monthly) – and occasionally watch one them. This week’s EcoTalk had the economically seemingly clueless anchor interview a few folks attending this year’s WEF. One interview (the only interesting one IMO) was with the CEO of OMV.

The FCF payout ratio rule is just a way to minimize risk and avoid the stupid system that a company needs to take on debt to pay a dividend… because that is exactly what the company needs to do if the dividend is not covered by the free cash flow.

I mean, I can live with share buybacks. Reducing the capital may be a good thing and at least you do not have to pay tax. But debt for paying dividends?

BTW: most utilities have a FCF payout ratio of over 100%… that is why I don’t touch them.

I might dig a little deeper, but it’s hard to do so especially when current political tantrums make the US potential brides prettier cheaper (except for those Energy ones …).

I’ve been writing Put options on OMV for some time now. Nice extra tax free income, but also wouldn’t mind having to take delivery at a ‘discount’ either.

What do you guys think about General Mills? First time in a long long period I may buy some for my divi portfolio. Historically that was a nice cyclical from a non-cyclical sector. Juicy market dividends…

GIS and KHC bagholder here. I don’t use their brands and so have no real attachment/feel for GIS as a consumer. Valuation still could be considered high considering expected growth.

Still with both GIS and KHC you have a decent dividend.

I like Flowers too. But this is just to reinvest some of my dividends. Flowers is interesting for a new position.

I hold GIS since 2014, had a nice run, exactly the type of volatility I need for my “buy low sell high” part of my dividend strategy. Which is: “Invest dividend to a position still on buy and less than 4% of portfolio value in sequence of last buy. Sell down to 5% of portfolio value when over 6%”.

I’ll buy some today. It is not my choice, the dividend reinvestment is mechanical.

Maybe I’m missing something about FLO, maybe it’s just because the mentor who (also) seeds my watchlist recommended FLO as a buy but keeps pronouncing the company name (in very German way) as Flowers Foots.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.