Hi

Has anyone taken a closer look at be Yapeal?

Any USPs?

At first glance: I don’t see any advantages over Zak or Neon.

Maybe the app will be a bit nicer.

Hi

Has anyone taken a closer look at be Yapeal?

Any USPs?

At first glance: I don’t see any advantages over Zak or Neon.

Maybe the app will be a bit nicer.

Is it me or the site is cringe worthy? It’s like some banker is trying hard to get young people onboard.

I don’t like its name though.

Well, interesting.

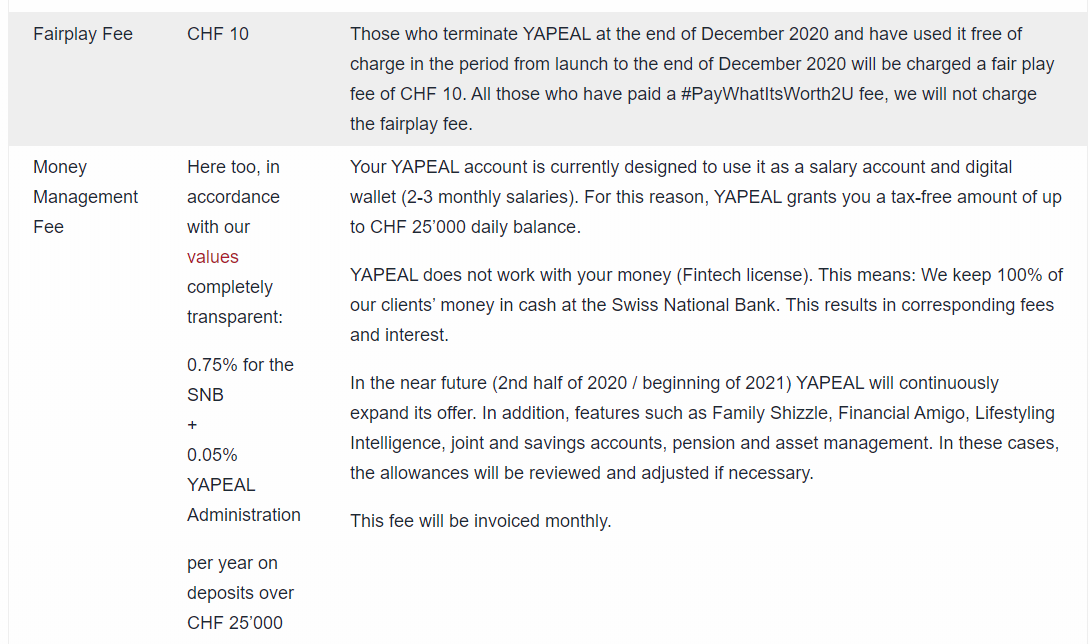

The fees don’t seem outrageous (though this might be a controversial statement on a Mustachian forum), I am just surprised that they are not looking for a freemium model like Zak. Maybe fees are back in fashion?

I am just not sure who the target group is that is not already served by Zak, Neon and Revolut.

If you want people to pay for something that they can get for free elsewhere you better offer something unique, other than flashy names. Their USPs seam to be negative interest rate from 25k+, no free cash withdrawal and no maestro card. Jokes aside: the fast onboarding, customizable ibans and their use of hashtags and hip-names for features like family-shizzles are probably the only things.

During the growth phase the base version has to be free, otherwise you will never attract enough customers. They even have the impudence to charge you for trying their product during the “free” phase if you decide to leave. Most of the people behind this project are ex-bankers of big banks pretending to build a fin-tech but obviously still keep the old swiss banker mindset - this will be one big failure.

This was literally my impression when I found it couple of days ago and was surprised that never heard about it here. When I looked at pricing I understood why.

Gizmos aside, the only real advantage I see in Yapeal is that your money is held in real Swiss francs at the SNB. So it’s more secure than book money from commercial banks. You don’t pay negative interest or the admin fee on balances up to 25k. If you keep up to 25k in a private account, then Yapeal should technically be more secure than other private accounts. I can’t imagine why anyone would keep 25k in a private account which doesn’t pay interest, but the fact that you hold base money is an advantage over Neon and ZAK. That’s the only advantage I can find. Judging by their marketing they are targeting the kind of customers who would fall for the Alternative Bank.

As far as I can remember “Family shizzle” would have been cringy 13 years ago. How did they think that was a good idea?

The security gain going from a normal bank to yapeal seems minimal because of Einlagensicherung, right?

Agree that they seem to target “I don’t want my money being invested in a bad company”-people.

But I seem to remember that the Nationalbank invests in similar companies as banks. So I don’t quite get ut.

I’m an Alpha tester since some months with the yapeal…but at the moment there’s no big benefit in comparison to other players on the market (revolut,neon,zak).

It’s funny to generate your own IBAN and have one of the newest visa card (debit and also v-pay) and the onboarding is really fast…but naah…

Yes, the wordpress webpage is a bit cringy

A lot of things which would have been cringy 13 years ago are suddenly all the rage…ever heard of K-Pop? Grant it, both K-Pop and family shizzle still make me cringe.

I agree that the security benefit is minimal. I was straining to find a benefit. The SNB is “private” but in reality benefits from virtually unlimited backing from the state, just like the SBB. So real Swiss francs have much broader backing than the book money of a single commercial bank. As far as a single fiat currency goes, Swiss francs at the SNB is probably in the top 5 most secure bets. Similar to holding CHF in cash, but with the advantage of financial services. But I’d have to take a closer look at what the exact legal arrangement is.

Cantonal Banks have a unlimited state guarantee, if you want security I would rather open an account there. In case Yapeal defaults (which is very likely with their current strategy) you will probably have to wait for ages until you get any money back from the SNB.

Not all cantonal banks without error so verify before

Not the BCV, BCGE etc.

BCV, BEKB and BCGE are the 3 with no cantonal guarantees. But it is important to understand that a guarantee, whether cantonal or from Esisuisse, can still mean a long wait for your money. I don’t think you could compare a guaranteed bank balance to actual legal tender. But that said, I do not (yet) know what the process of claiming your money from the SNB would be like. Obviously the account at SNB is Yapeal’s (or a third party’s). In any case, I would agree that this is a fringe benefit. Still I find it interesting, as I don’t know of any other bank-like financial service provider which holds all balances in base money.

Two of them from French-speaking Switzerland. Taxes, fees while buying house etc. are also one of the biggest here. So, my question is: what’s wrong with this region (I also live in)? ![]()