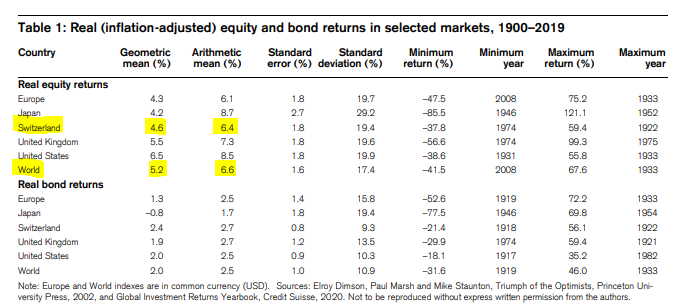

Thanks for providing the sources. Switzerland is really a great place to invest, similar to the US. Independent, high living standard, high inflow of skilled workers, tax-friendly, great law system etc.

I think that’s part of the reason why the stock market performed so well. Of course that says nothing about the future…but I’m waaay more confident in Switzerland than the rest of Europe.

I’m just replacing the rest of the developed exUS world with it. Market neutral would be 58% US, 32% developed exUS and 10% EM. I’m just doing 16% CH 16% developed exUS/CH and keep the rest the same.

There is the “age in bonds” rule of thumb. If you consider your 2nd pillar as bonds, it should cover that part for a good time if you’re at the start of your journey. When it doesn’t fill the whole allocation anymore, then it’s time to think again if that’s really the allocation you want and what you want to invest in.

I personally want to be more agressive than that so I’m using (Age/100)² in safe assets. I’m splitting the other part of my investments between stocks and real estate with a similar shift (Age/100)² in real estate, the rest in stocks.

That way, I’m agressively turned toward stocks when I’m young and gradually switch toward real estate and bonds as I grow old.

At age 30, that would give me:

83% Stocks

8% Real Estate (RE Funds or REITS)

9% Safe assets (probably my emergency fund and 2nd pillar)

At age 65:

33% Stocks

24% Real Estate

43% Safe assets (I would have to reevaluate this if I take a big part of my 2nd pillar as a pension, that’d probably allow me to take more risk, so I may go for a bigger allocation toward stocks and real estate)

And at age 80:

13% Stocks

23% Real Estate

64% Safe assets (same as above, I may fix a lower boundary on stocks, maybe 20-25%).

I don’t think there’s something inherently wrong with swiss stocks, although there is with big allocations in a single stock. If you don’t want an extra layer of complexity, a broad world ETF is probably the way to go (though it’s worth delving deeper in the risks tax and political instabilities may weight on some of the assets in these funds. The more knowledgeable you are, the more power to you).

With your 2nd pillar, it’s likely you already have a healthy allocation to safe assets. I’d check that my emergency fund is funded enough for my needs, that I don’t have short term projects that I want to fund and am not willing to delay in case of poor stocks performance and that I have the resilience to stick with my investments if stocks go down deeply (otherwise, I’d invest in a balanced fund in order not to see the value of the stocks part of my investments as a discrete number). I’d still make sure that my stocks investments are broadly diversified (VT fills that bill).

All the funds can be traded on the secondary market, because if they are not on Zurich market, they can be traded over the counter.

The primary market, as you call it, is only a contractual right to redeem your shares at the NAV minus a fee. The price is not low because it is illiquid, but because it is a contractual price. That primary market is not a market, it is like a put option. Of course, no correlation can be calculated because the NAV is only calculated twice a year.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.