Just some quick math (assumptions):

If they can get 2% somehow of the 26M AUM, you would have 520k/year. Now compare this to 150k/year salary (average) with 100 employees* → 15M salary costs only.

*according to LinkedIn, seems like a lot to me in relation to the 26M AUM

I suspect a significant portion of Alpian’s losses comes from staff salaries, as previously mentioned. Another major cost likely stems from office space, surprising for a digital bank that offers no physical deposit options. Maintaining such premises doesn’t seem justifiable.

They’re also likely bearing costs for their banking license and third-party service integrations. Technical connections, like those with IBKR, may come with high fees that contribute to ongoing losses.

Although Alpian is backed by a major Italian bank, and these costs may seem minor at group level, if the parent company applies a strict profitability standard, similar to some French management approaches, they may decide to shut down operations if targets aren’t met.

Unless things improve, I wouldn’t be surprised to see Alpian exit the market within the next two years. Ideally, they’d be acquired by a local competitor interested in their tech. But with negative profitability, Alpian isn’t currently an attractive acquisition target.

Update

Upon reviewing their financials, it’s clear Alpian faces serious challenges. Salary expenses total CHF 11 million, and office rentals add another CHF 800’000.

More worrying is the projected cumulative loss of CHF 90 million, with CHF 30 million lost just last year. This suggests the bank is far more indebted than it appears. Smells fishy…

Exactly: And in early 2024 they were talking about approaching 100m AUM.

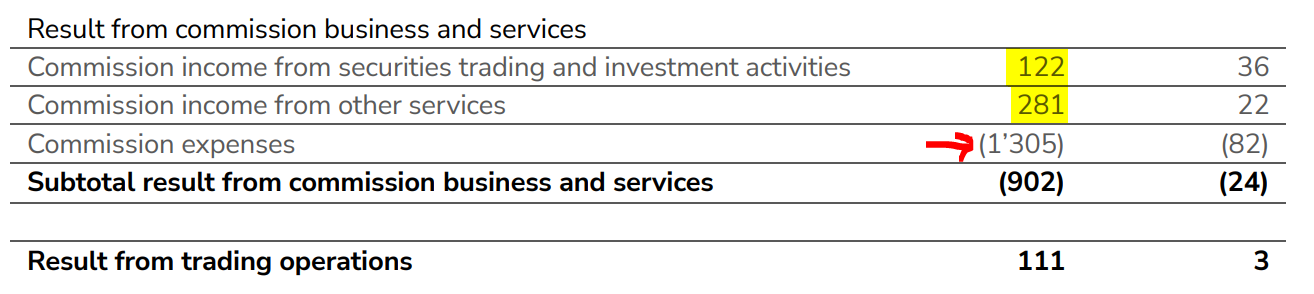

While in their 2024 annual report they state that they managed to triple the 2023 AUM of 9.05m to 26.26m. Where is the disconnect? Do a lot of people just keep cash in the bank?

They indeed earned 403k on the 26m AUM (1.55%) but had to pay 1.3m to get it.

I kind of agree. At least they are trying to fill the need for some kind of financial advice for the people with their offer. But maybe it’s not enough. Besides this, there is nothing really groundbreaking. In the investing part, it is yet another “we construct you a stocks portfolio by randomly weighing standard ETFs on regional stock indices for a 0.X% yearly fee” app.

I tried to pay myself from Alpian to Neon and PF. For both Banks I’ve generated a QR that apparently Alpian doesn’t support yet.

So I had to type in all the info by hand. If I’m not mistaken, I had to type the address as well, which is “powered by google”.

I just saw that too on the app but haven’t received any mail about it.

I hope the free account stays the same and they don’t treat us the Neon way and enshitificate the “Standard” plan.

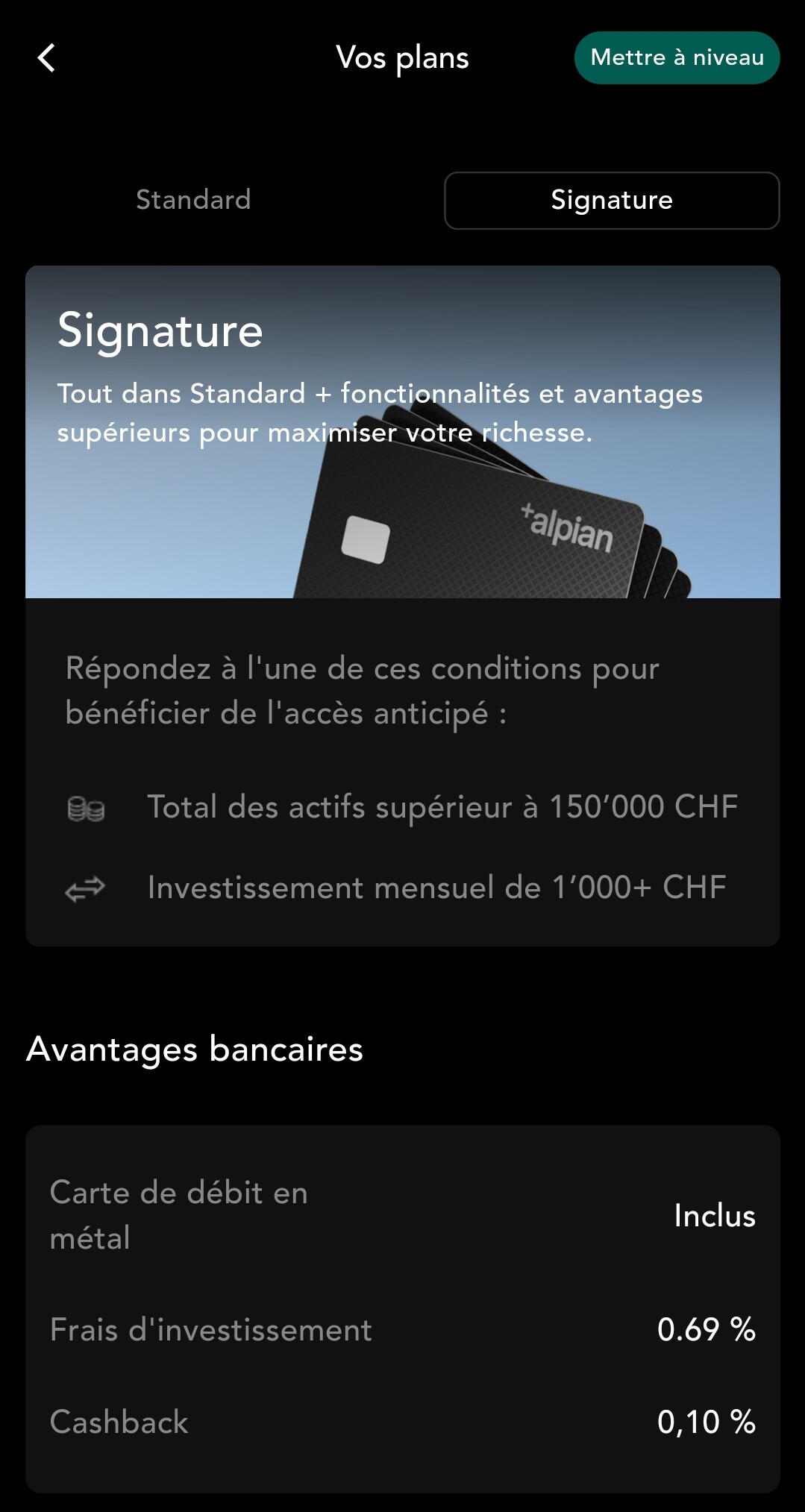

While I haven’t found any strategy details, it doesn’t seem to be very interesting (compared to VIAC and finpension) at 0.60% management fee¹ + an average TER of 0.15%. And as they are using ETFs, their solution presumably can’t benefit from the US/Japan withholding tax exemption for pension funds. They also only offer a single account per person.

¹ The first 1’000 clients won’t pay management fees until end of 2026 but that’s practically irrelevant for a long term investment.

Don’t know how much difference it makes, but it seems they are going to use traditional mutual funds (managed under BlackRock brand) and not ETFs (iShares).

Edit:

Managed by lemania-pension with BlackRock ETFs,

Your assets are invested in institutional-grade BlackRock index funds and ETFs

I wonder what the 0.60% management fee is for, since we also have to pay VAT, Swiss StampTax and TER. Maybe I am mistaken, but don’t other providers like VIAC, TrueWealth or YUH include these fees under their 0.40%-0.50% fee?

Doesn’t seem very competitive to me, especially because we don’t which funds it uses.

It’s simply the fee for lemania-pension and Alpian itself. The TER goes to BlackRock and taxes go to the Swiss government.

If you use the 0% TER index funds at VIAC or finpension, the 0.4/0.39% fee indeed includes everything¹ (there is no stamp duty charged for Swiss-domiciled mutual funds), except for currency exchange fees, if you choose funds that aren’t traded in CHF. They also optionally offer some non-0% index funds and ETFs, in which case the TER and stamp duty are not included in the 0.4/0.39% fee.

I think Yuh works similarly, just with a slightly higher fee of 0.5% p.a., but I’m not familiar with the details.

TrueWealth doesn’t use 0% TER funds (you might pay about 0.15% for fund management) and they use some ETFs where stamp duty applies. However, they (currently) don’t charge any management fee themselves, so the total costs are very low.

¹ The funds have subscription and/or redemption fees but that’s not a management fee and roughly the equivalent to the spread costs of ETFs.

I sent an email to finpension about this in Feb ‘24 and the answer was:

Wir haben keine Mitbeteiligung bei den Währungsumrechnungen. Ihr Fonds ist explizit nur in USD handelbar, weshalb die Swisscanto eine gewisse Umrechnung verrechnet. Es ist aber deutlich weniger als die genannten 2%. Durch das netting werden die jeweiligen Käufe und Verkäufe so gut wie möglich kostenneutral verbucht.

Just wanted to share that whenever I move USD from Alpian to IBKR, it’s free of charge and very fast.

But for some reason IB puts this transaction on hold because they call Alpian a non financial institution. Of course it’s incorrect.

Eventually they release it but they demand proof of transfer and then add 4 days holding period. It’s annoying. I have told them twice that Alpian is Finma regulated bank.

Unfortunately, I have never transferred USD from my Alpian account to IBKR.

But I would be very curious about the free of charge. Do you receive the full amount on IBKR? My experience with USD transfers to the US is that there is mostly one or several intermediaries that take their cut.

Weird that I don’t see much movement about Alpian. Anyway..

After they redesigned their UI, they are now offering some new bonuses if you deposit more on your account and also the usual bring-a-friend thing. I wonder what’s the feeling on this forum about them. I am still unsure if they have ebill (haven’t fund online but I didn’t search much).

Personally I am still unhappy that I lost the opportunity to get their card for free, but that’s my fault

I wonder if now the FX is getting near neon (or better: neon is getting near Alpian..)

I tried Alpian — both for payments, transfers, and their investment offering.

In general: the website and the app were full of bugs (lorem ipsum placeholders, translation errors, non-functioning buttons). I usually don’t mind small glitches, but it’s absolutely unacceptable for a so-called FINMA-regulated bank. If such issues still exist when they go live, it’s really, really embarrassing. I assume most of these bugs have been fixed by now. Personally, I expect a certain level of professionalism and I’m also willing to pay for it. I had my account deleted after just two short weeks — which, by the way, was only confirmed by customer service about three months later.

Fee structure: completely off. I’m supposed to pay a USD 7 fee just to send USD to a non-USD region? Sorry, no thanks. Then there are Alpian’s investment products: I’m supposed to pay a 0.75% fee for an S&P 500 product purchased through Alpian? A few months ago, there were barely seven ETFs available. The offering was rather weak and didn’t make much sense as an investment platform. I was initially committed, but after completing the investment questionnaire, I was already quite disappointed with the limited selection.

On one transfer, I had the issue that a different IBAN number was shown as the sending account. Why is a shadow IBAN being used for outgoing transfers? If you send money back to that shadow IBAN, it doesn’t go back to your own account (you’d have to use your personal IBAN for that). Sure, customer service can help locate the funds internally, but that’s just old-fashioned and cumbersome.

The only positive aspect: monthly interest payouts — though in today’s rate environment, that’s hardly a unique selling point.

The metal card is well made. From my Amex Platinum experience, I know metal cards sometimes get stuck in ATMs, so it’s probably best not to use it for cash withdrawals. Otherwise, it’s quite a nice card.

Alpian is backed by Intesa Sanpaolo — so, like Radicant with BLKB, it’ll probably run fine for a while, but eventually they’ll need to show results. The marketing is pretty slick, but so far, Alpian’s numbers remain unimpressive (number of clients, contribution margin, etc.). I think in five years Alpian will be in the same position as Radicant; their customer base isn’t attractive for an acquisition — mostly frugal users like us with low bank loyalty who don’t want to pay fees. For FX rates, Alpian is okay, but honestly, I’d rather go with WIR Bank — a solid Swiss bank that doesn’t have that intense “start-up” feel Alpian gives off.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.