Even if the spreads could be lower, they are aligned with the spreads found in ETFs.

The spread on emerging gov bond of the “Vanguard USD Emerging Markets Govt Bond UCITS ETF (USD) Dist” ETF is 0.2862% (info found under the market quality metrics).

If you multiply by 2 (buy and sell), it’s higher than the 0.5% (0.5% buy, 0% sell) of CS. Obviously, bonds are less liquid which imply higher spreads.

Concerning the FX fees, the line in bold from ther FAQ mentioned that the average fees are only 0.05%

Is there a fee for foreign currency exchange?

Yes, there is a fee. Due to VIAC’s intelligent calculation system, the fee for foreign currency exchange is ideally 0%. This happens when foreign currency purchases and sales are of equal size across all customers in our monthly rebalancing. If the purchase and sale volumes are not identical, the bank will charge a commercial fee of up to a maximum of 0.75% on the difference to be traded for foreign currency exchange. The resulting costs are then distributed to all customers and thus already massively reduced (see Academy for details). Historically, the average annual cost over all strategies is less than 0.05%. Usually these fees are hidden from other providers and are not disclosed to the customer.

The total TER of the real estate fund is not really transparent.

Disagree. IIUC spread is ask - bid, so in the CS case subscription + redemption. For the Vanguard ETF you mentioned the spread is 0.2862% - not multiplied by 2

The WIR Bank charges us 0.75% spread. This is the maxiumum which you pay on foreign currency. It used to be 1% at the beginning, which we were able to renegotiate to the new level.

This external spread is the optimized in two steps:

First with the personal netting; so if you buy and sell i.e. USD we first pool and net for each customer.

Then we optimize ist again over all customers with a general pooling and netting

On the final trade, either a buy or a sell trade, charges the WIR Bank the Spread.

Subsequently, a personal rate is calculated for each customer based on the individual trading volume. More on our pooling and netting can be found here: https://viac.ch/en/academy/pooling-and-netting/

Since a lot of money is flowing in at the moment, the optimization is rather deep at the moment. However, if, for example, in a very positive month, shares are sold via many customers, this can quickly move in the other direction.

At the moment, the general spread (so without personal netting) is moving around 0.50%.

And now to the mentioned 0.05%. This figure was calculated with historical data and some assumptions over all strategies. The basis is a customer, who adds the same amount of funds each year into the same strategy. He would end up paying spread on the initial invemtments and within the rebalancing for his allready invested funds. The idea behind it is a buy and hold approach, as we only offer a monthly rebalacing and are not a trading app. So if you shift your assets more often, you end up paying more of course as discribed above. I hope this explanation helps!

Regarding the discussion above, would you consider making the funds buy/sell spread more prominent for transparency? (currently it’s fairly hidden as one would have to check each KIID separately).

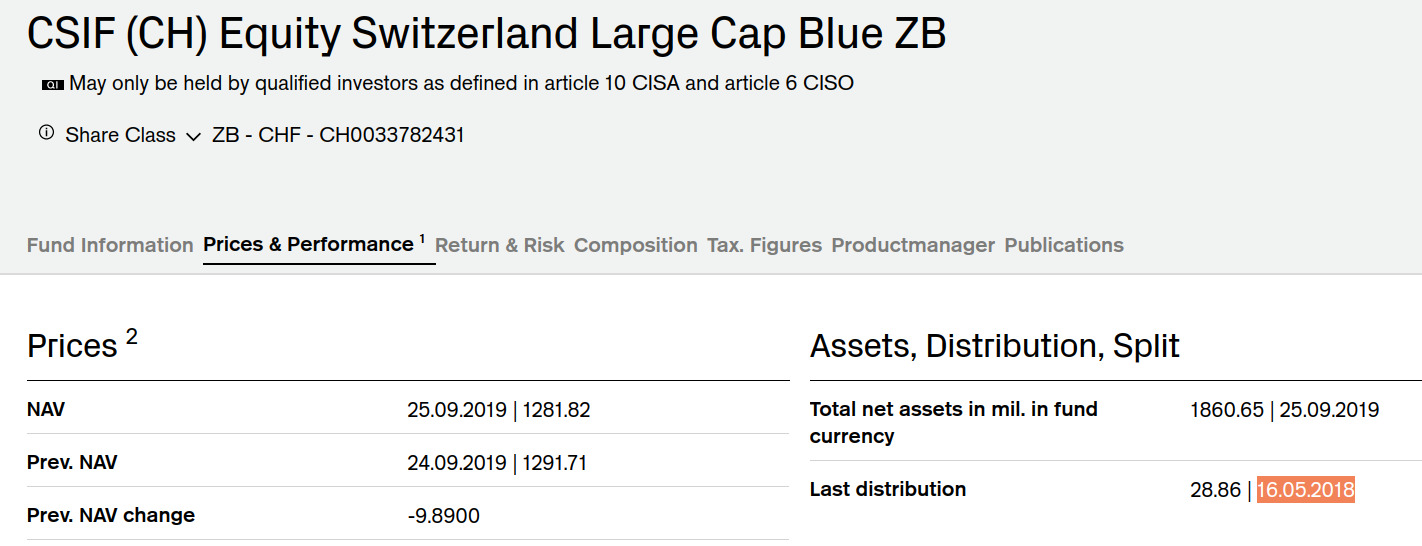

Does anyone have any idea when the next distribution will be for the CSIF funds?

Last year it was in the middle of May but this year I’ve only seen a distribution for CSIF World ex CH Small Cap (the very same day but different year).

The last distribution was on 16.05.2018 for most of them. This year very few got a distribution on 16.05.2019/ 17.05.2019.

The VIAC page contains links to all factsheets where you can see the latest distribution. I can put as example the fund for SMI (but it’s the same for most of other CSIF funds):

Thanks for a detailed reply. One clarification: even if I’m not adjusting the strategy, VIAC still does the rebalancing every month, which results in fees. Is there a way to make it less frequent, e.g., [half-]yearly unless the strategy is adjusted manually?

I’m not sure if I should use the Global 100 (don’t like the fact that 28% is SMI) or just do something on my own:

3% cash

12% SMI

25% SPI Extra

20% World ex CH

20% SP500

10% World ex CH Small Cap

10% EM

or

3% cash

12% SMI

25% SPI Extra

5% Pacific ex Japan

7% Japan

10% Europe ex CH

25% SP500

3% Canada

10% EM

My ideal scenario would be something that comes close to VT, but due to swiss regulations 40% needs to be in CHF and I don’t want the CHF hedged index funds.

By reading and partipating to this forum, you confirm you have read and agree with the disclaimer presented on http://www.mustachianpost.com/

En lisant et participant à ce forum, tu confirmes avoir lu et être d'accord avec l'avis de dégagement de responsabilité présenté sur http://www.mustachianpost.com/fr/

Durch das Lesen und die Teilnahme an diesem Forum bestätigst du, dass du den auf http://www.mustachianpost.com/de/ dargestellten Haftungsausschluss gelesen hast und damit einverstanden bist.