I might also been missing what the issue is, there’s been enough fast growth/low growth year that someone with a decent portfolio and some predefined allocation would have to rebalance, whether in accumulation or withdrawal phase.

What’s so hard about sticking to a predefined percentage? Is it that a lot of people are 100% VT? Personally I’ve always been X% equity, X-Y% fixed income (or similar) and you do have to sometimes rebalance (and at some portfolio size, contributions aren’t enough).

substantial stash in a world-stock ETF with an optimized mustachian strategy to the cent

There’s only one thing been done from the beginning: BUY. Market crashing ? Great, buy cheap!!

risk identification / new cycle in personal life / being curious / fashion / whatever (follow the links above): investing into new asset classes / stock regions / stock caps / factors / whatsoever with defined allocation

it works so well contribution does not help maintaining the allocation as pre-defined.

While you were used to buy X, or X and Y you now “have to” stick to your rule and sell X to buy Y.

Are we prepared not only to buy, but also to maintain the portfolio when diversifying?

Another popular example: “I started to buy exUS to lower US exposure and target a 50/50 US/exUS allocation”. So what do you do if it works so well a year later some POTUS has plunged the US and you’re at 20/80. Let’s sell exUS and buy US because that’s the strategy, to target 50/50. The US are bankrupt but will recover, never bet against the US (Warren buffet). I am pretty sure most people who started buying exUS are not ready to sell it to buy US to stick to their plan, if such things happen (not sure I would be capable). Are they expected to ?

I am exaggerating all the examples just to understand if all these themes and discussions about diversification go beyond buying stuff because it feels comfortable in the current context, and if we are ready to sell huge amount of one class to buy another to stick to our targets.

We don’t talk enough about that, imho, because when reaching that stage that’s a new action with some psychological steps to overcome, in my experience. It’s easy to buy 60X/40Y, or adjust contribution to maintain a predefined allocation, it’s harder to sell ramping Y to buy falling X when it reaches 55X/45Y due to market events, especially if your global portfolio has gone sharp in one direction (up or down).

At first sight rebalancing is not difficult. You sell some, you buy some, that is it. I think IB still has a one-click solution for this somewhere.

But then… how to re balance? You want to catch Shannon’s demon, how do you do that? You could use just the invested capital. Or you could use the risk what probably makes more sense, what is done in managed futures normally.

As I said, first you have to decide where you want to go. Then you choose the method of transport. A robo adviser would just be a form of transport. You don’t enter a plane and say “let’s see where it takes me…”.

There is the very moment when a minimalist lazy investor used to buying was lucky enough their stash has grown big enough that contribution does not help and they must be active in their portfolio to stick to their allocation. Part of this (size and situation) is thanks to their diversification in alternatives that worked too well. And then they’re thinking “oh well I might just pay for a robo advisor where I could replicate my initial strategy and save me a few clicks, errors, and thinking “am I doing the right thing” each time I have to place an order”

I would never ever think I would face this “problem” when I rtfm, thus my contribution on questioning how to deal with this “good” problem

Did I get that ? No I didn’t (see, you are at least smarter).

The plan has gone well until now, my usual transport implies new buttons to stick to the plan, due to the current situation the plan has lead to, thus I am thinking of ordering an uber to continue the ride.

OK, sorry. Most strategy books on Futures (including the famous Turtle System) recommend a position size based on risk. Meaning if you risk say $2 per contract you buy 5 times the contracts than if you risk $10 per contract. That is all, risk-based balancing/position sizing, you change size when the risk changes.

Shannons demon says that you can make money from two non-correlated investments by re-balancing even if both of those investments per se would lose money.

Ok, that. Isn’t there a bigger chance of catching waves if we have regular, even time based, and/or band-based rebalancing (I guess this is when the allocation has gone out-of-band and we’re “told” to rebalance?) , as a robo would do automatically ?

Thank you for confirming I am well-positioned when not investing in them, one of my rule being “ensure you understand the basic info of what you’re buying”.

Of course. The best strategy is the one executed when you don’t think about it (because you’ve designed a system that does it for you automagically).

You could do that with monthly CHF 1.00 contributions to a “filled up” VIAC account - I talked about this before - or slightly higher inflows to another robo advisor doing the work for you. To make this fully automatic, time-based (weekly, biweekly or monthly) standing transfers are best in that they’re the easiest tool to set up.

Managed futures should do just as well (especially for momentum/trend following) but are way down the learning curve and require more intervention.

Very interesting, who would have thought you can systematically win at coin flipping.

The single most important element is the investments not to correlate. How you exactly rebalance is not that important. Just for rebalancing I would not pay for a robo adviser, sorry.

BTW: found the button “rebalance” on the IB TWS. That one is free…

discusses Shannon’s Demon, Parrondo’s Paradox, the Rebalancing Risk Premium, and discusses special cases such as Samuelson’s critique, Warren Buffet, minimum variance portfolios and when to apply which weighting ex-ante.

Compares randomly-selected rebalancing windows to fixed (Nth date of the month), and derives that “it has been advantageous to use the window of 7-10 days before the end-of-month”

introduces rebalancing through Shannon’s demon. Shows Dempster/Evstigneev/Schenk-Hoppé’s result that even with negative-CAGR assets, at a portfolio level rebalancing can yield (highly) positive returns given zero or negative correlations. Finds that this is possible with Nikkei 225 stocks and JGBs, both known to be negative over the 1995-2010 period.

Just to repeat: not the action of rebalancing is the difficult part, but to decide what, when and how to diversify and rebalance. The robo-advisor can only help with the action itself and that is present in IB as a single click, so for me not really worth throwing money at.

Now how I do it: I am risk tolerant, did and will probably again lose 70% (without real estate, but the real estate maybe is next?) of my invested capital. That is normal at the stock market and the important thing is to survive and then get it back. Now, we have many years without such a situation and that is the real problem for younger investors.

Even if the performance probably is higher without it, I do some kind of rebalancing, depending on my strategy.

In my dividend strategy I start with 25 diversified stocks, maximum 20% per sector at equal capital, so 4% each. Once one reaches 6% I sell down to 5%. With this money and the dividends I buy more of the stocks that are still on buy and are worth less than 4% of the portfolio. This is somehow lowering the risk without a big premium because cyclical stocks bring home quite some cash that way… as long as the cycles are not too correlated. And that is where sector diversification comes into place.

Now in my momentum strategy I don’t do that. I even sometimes do double down, creating enormous positions when they run up. I partially sell after gains of 500%, 1000%, 1500% and so on and after every 12 months if the stock is not on buy any longer. That way I generate some income with this strategy too… and it is even fax-free.

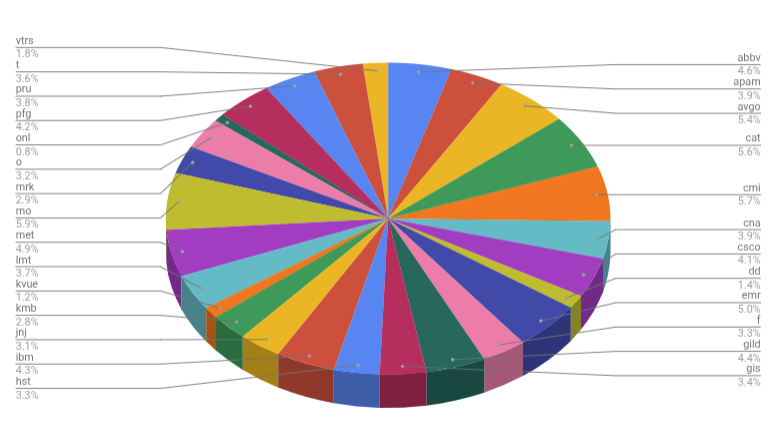

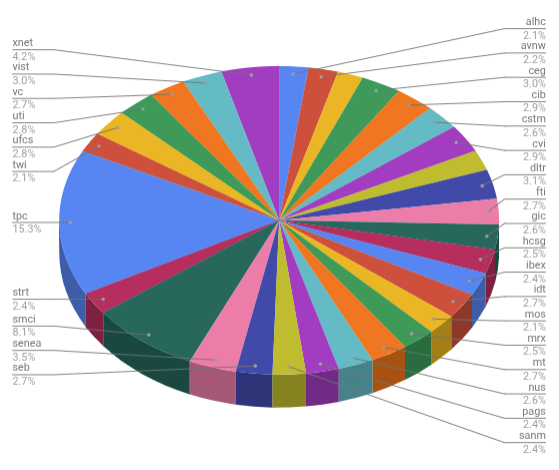

As an example here are my actual allocations for the dividend and the momentum strategies (Labels are the U.S. stock symbols)… and please, don’t do this at home :

Addendum: This is a stock-only portfolio and stocks always correlate a lot. To lower the risk you need to invest in other asset classes and fortunately you can do that today with ETF. For me the high risk of the stock market is not a problem, but for most people it is (and should be).

I think this is the key issue. Most people on this forum are likely experienced enough to invest directly without goofing up. But I would dare to say that a cheap robo advisor is the better solution for your average consumer. To give you an idea of what I mean, the most common issue I’ve run into with people I’ve introduced to investing is that they end up using limit orders, so their orders do not go through. It could be compared to servicing your own car vs. taking it to a garage. Doing a basic oil change or replacing spark plugs is a synch for those who “get it.” But people who don’t get it are likely to make costly cock-ups, in which case paying the garage is a bargain.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.