Although I never bought such a certificate, my work environment is such that i am quite familiar with them. Which kind of BRC do you have in mind? on a single stock? on an index? on multiple underlyings?

if it is on an index, i would not expect more than 2-3% of coupon

if it is on a basket of stocks, your final performance is often tied to the worst performer of the basket, not the average, so beware

The bid-ask spread is often high on these products, and the issuers and distributors of such product often have a commission that is included in the price.

For instance, you have a product that is worth 98CHF:

the issuer will take a 1CHF commission

the distributor will take as well 1 or 2 CHF commission

Now the mid price is 101 CHF. Add the bid-ask spread and you get an idea of all the fees middle men are getting.

On the other hand, the coupon received is not considered as taxable income in Switzerland…

What do you want to gain from it? This is mostly a bet against volatility, right? (if the stock goes higher than the coupon or lower than the barrier, you wouldn’t gain much from what I understand).

Why not simply hold the stock (or better an index to be diversified)? Also when comparing with the underlying, afaik they don’t take into account dividends, which can make the comparison biased.

Edit: and it seems a somewhat opposite to a FIRE approach, since it caps your upside, but you still carry unlimited downside risk.

You reached FIRE in terms of cash but how do you fund your actual day-to-day expenses. 2% ETF dividends is one way – but the BRC path seems to be another interesting one (3-5% p.a.; no tax; fairly limited downside – those bluechip stocks would need to drop more than 40% before you would get booked to your trading account vs. getting the 100% cash payback).

And they will during the next bear market, make no mistake about it.

So your upside is capped to 3-4% during good times, you lose 1-2% each time you need to roll your products, and lose 40-50% once every 10 years…

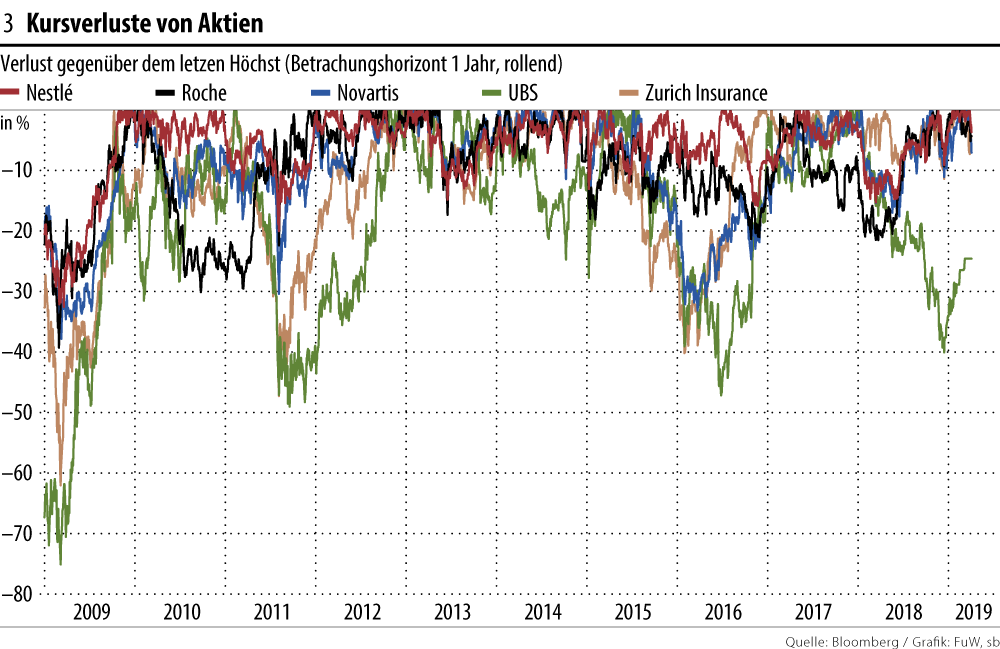

This chart says that none of those 3 stocks lost more than 40 percent but yes there is a risk. On the hand, investing in the current market feels even more risky. So brc make probably sense if you see limited addl upside for the market.

Do you think it’s risky and it might crash? If so BRC makes even less sense since in case of a crash you’ll be impacted as well. (How did those stock behave in 2008?)

Well the certificate would surely tank in a crash — but that wouldn’t matter if you hold it till maturity. Instead you will still get the quarterly bonus payouts.

…within the given horizon looking back 10 years and 1-year rolling periods.

It also says that Roche came awfully close to do.

Taking a quick glance at historic prices shows, how a close a call it was.

Just extend your rolling 1 periods by a couple days, let’s say 370 days (for Roche Holding):

229.50 CHF on 27 feb 2008

131.00 CHF on 2 mar 2009

for a drawdown of approximately 43%.

Granted, with a tenor of just one year for the BRC whose barriers gets fixed just once, initially, you wouldn’t practically be so unlucky to just hit that. But then, such products often do seem to have longer maturities. And on a longer time horizon, market drops of 30+ percent don’t seem uncommon, every 10 years or so.

In the end, for me it (again) boils down to predicting and timing the market.

Which, in this case, to me seems taking a (relatively) high impact but low probability risk.

Bit like Russian roulette.

…unless you actually do hit a barrier event.

Because then you might be hit with a loss, even at maturity.

What are you going to do in that case? Roll over your investment to a similar BRC, with limited upside, thus prolonging the (minimum) amount of time to recoup your initial investment?

Also, while we’re at it: Don’t forget about issuer risk. Sure, “ZKB” might sound very, very good and secure - and by way of state guarantee is.

But… is it, really, for the BRC you linked to above?

What about “ZKB Finance (Guernsey) Ltd.”?

Would that still sound so good and secure… in, imagine, a major market crash?

(I honestly don’t know, have nothing more than a gut feeling, on this)

I assume that some kind of index would be safer (40% drawdown are much rarer) but I can’t find attractive certificates with >40% buffers. A complicated beast

The 2% withdrawal rate sounds extremely conservative to me even considering market conditions. I think most people would consider 3-4%. The non-dividend component of that income from portfolio would also be tax free (mixture of return of capital and tax-free capital gains.)

If you are buying funds domiciled in Ireland like VWRL then there will be no withholding tax, no?

Expenses sound low if you are a family like Mr RIP. It is possible that they will be spending 30’000 yearly for a while on childcare alone if their family grows and they both continue to work.

How do you get 5765 CHF in taxes on a dividend income of 40’000? That sounds very high to me.

It looks conservative - however not so much considering he does not want to eat into principal. As the discussion above seems to indicate, a 4% return is hardly risk-free.

I did not check the numbers but assumed they not only include income tax (on dividend income) but you would also need to account for wealth tax on the 2m.

Technically, dividends also come from principal. Economically and contrary to intuition, it does not make a difference whether your spending money comes from selling shares or dividends. As most shares trade at a multiple to book value, your stock should also lose more value than you are getting with dividends. Seen in this light, dividends destroy more value in the share price than you are getting paid out in your trading account.

Regarding barriers: Risk is roughly defined as the volatility your investments expose you too. For a long term investor, this is not decisive. Barriers with their fixed terms however are structured to let you take this risk for the banks.

With barriers, while fees and the imbalance between upside and downside have been mentionned, there is also the related point of expertise. Having expectations about how the market will develop is one thing. Making a bet on it with a derivative is another thing. With a barrier, you are going against pros doing it full time. I don’t think that this is conducive to good pricing of the risk you are taking. Meaning that the interest is probably too low for the risk you are taking.

Addendum:

What I also dislike is Barriers on high dividend titles where the dividends go to the bank. With a share yield of 3%+, you get just 1.5%- for the specific risk of the barrier.

Addendum2

NZZ-Article that goes deep on the tax situation

It does, in light of the tax situation. Dividend income is taxed differently from just sale of assets. And as we know, Switzerland has no capital gains tax for individuals’ personal wealth management.

I just ran a similar calculation through Schwyz’s tax calculator. A CHF 45k dividend income will approximately incur a 6-7% tax charge. Whereas selling stock from principal is tax-free. The income tax percentage is, of course, small, if you’re not having any other income, but could make a bigger difference if you (or your spouse) had.

I am not sure it’s that simple an equation.

Why shouldn’t the trading multiple (over book value) change?

I see you describing rather a sequence of return risk than a yield problem. Many guys smarter than me regarded a 3% withdrawal rate as sustainable. (Even over 2 world wars and the big recession, stocks yielded ~5%. Your mileage may vary.) There are calculators that tell you how long your stocks will last, crash included etc. The biggest risk, as I understood, is a crash early in your retirement. There are solutions proposed like holding more bonds/cash 5y before to 5 years after retirement.

The “safest” way to get 40k (but giving up all upside) is by means of a Swiss PK rent. Still, the whole system could collapse.

Monte Carlo simulation works like this, for our case: You decide on a portfolio allocation and annual withdrawal amount. Then you simulate the market using either historical data or some statistical distributions. Then you check your end result after 30 years. Then you run this simulation 10’000x times, each time getting a different amount at the end.

For example, for a $1’000’000 portfolio with 100% VTI allocation and annual withdrawals of $45’000, this are the results:

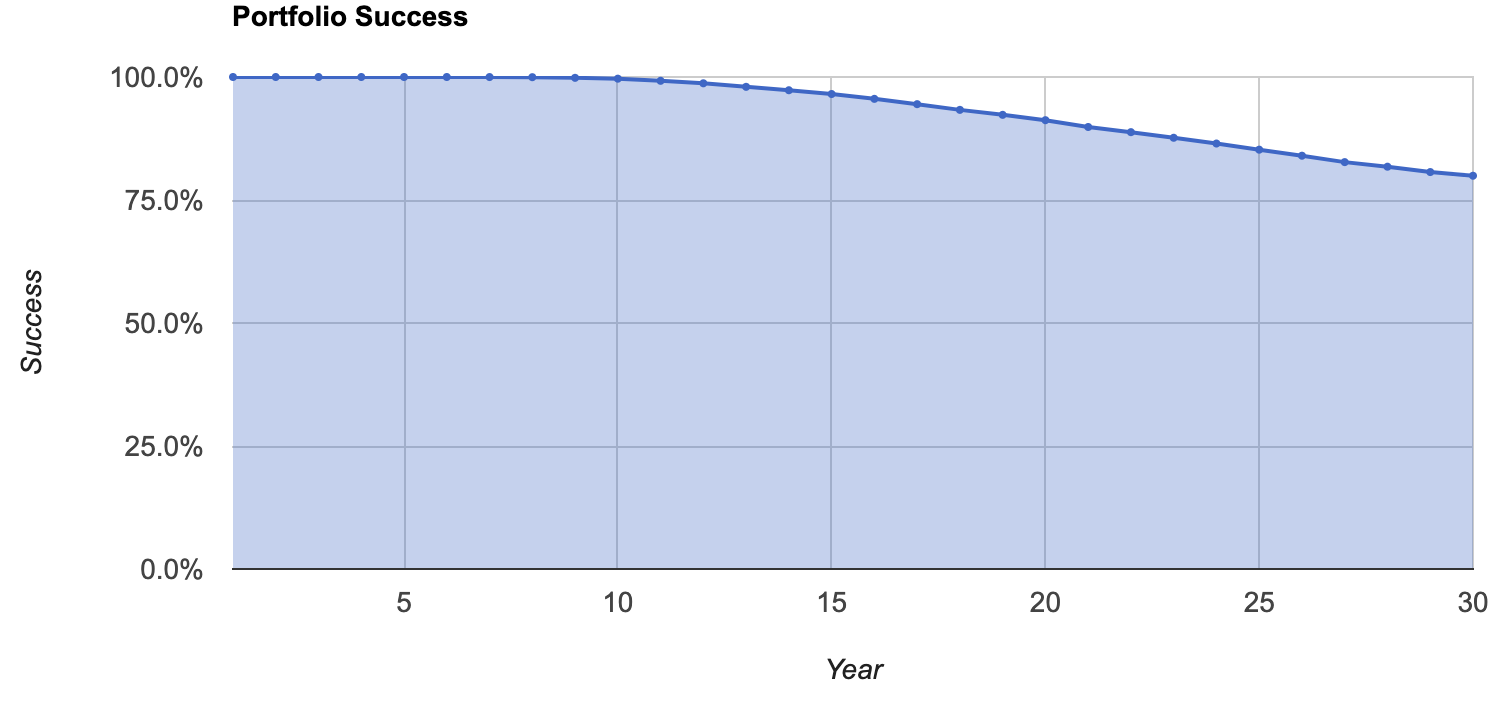

This second chart should be of special interest to you. It shows the portfolio survivability rate. That means: how many portfolios of the simulated 10’000 still had some money left after X years.

I think your idea of always satisfying your 40’000 expenses with 2% form dividends is kind of flawed. You would normally get the 2% from dividends and then top it off by selling as much stock as needed to get to 40’000.

By reading and partipating to this forum, you confirm you have read and agree with the disclaimer presented on http://www.mustachianpost.com/

En lisant et participant à ce forum, tu confirmes avoir lu et être d'accord avec l'avis de dégagement de responsabilité présenté sur http://www.mustachianpost.com/fr/

Durch das Lesen und die Teilnahme an diesem Forum bestätigst du, dass du den auf http://www.mustachianpost.com/de/ dargestellten Haftungsausschluss gelesen hast und damit einverstanden bist.